What makes CIO advisory services different from hiring a full-time CIO for a mortgage bank?

CIO advisory services provide strategic technology leadership on a fractional or interim basis, delivering executive-level expertise without the commitment and cost of a full-time hire. For mortgage banks, this means access to a seasoned technology leader who understands regulatory compliance, loan origination systems, and cybersecurity requirements, but with flexible engagement models. You receive clear priorities, decision support, and governance frameworks tailored to your institution's size and risk profile, with 30-60-90 day deliverables and measurable outcomes that prove value immediately.

How do you address GLBA compliance and data privacy requirements specific to mortgage lending?

GLBA compliance and data privacy are foundational to mortgage banking operations. Advisory services include assessing your information security program against GLBA safeguards requirements, evaluating customer data protection controls across loan origination and servicing systems, and establishing clear governance for third-party vendor oversight. You receive board-ready reporting that demonstrates compliance posture, identifies gaps in consumer data protection, and provides actionable remediation plans. The approach prioritizes business continuity while meeting regulatory expectations for administrative, technical, and physical safeguards.

Can you help mortgage banks prepare for regulatory examinations and audits?

Absolutely. Regulatory examination readiness is a core component of CIO advisory services for mortgage institutions. This includes cybersecurity program assessments that align with FFIEC guidelines, third-party risk management frameworks that satisfy examiner expectations, and incident response plans that demonstrate operational resilience. You receive documentation that's exam-ready, including risk assessments, control matrices, vendor risk registers, and board-level cyber risk briefings. The goal is to enter examinations with confidence, clear evidence of oversight, and defensible decision-making processes that withstand regulatory scrutiny.

How quickly can you stabilize technology risk after a CISO departure or security incident?

Interim CISO services are designed to stabilize technology and cybersecurity risk within 30 to 90 days. The approach begins with immediate risk triage to identify critical exposures affecting loan operations, customer data, or regulatory compliance. Within the first 30 days, you receive prioritized action items with owners and due dates, incident response plan validation, and board-ready status reporting. By 90 days, critical control gaps are addressed, vendor sprawl is reduced, identity and access controls are tightened, and you have stable metrics that track meaningful risk reduction rather than activity volume.

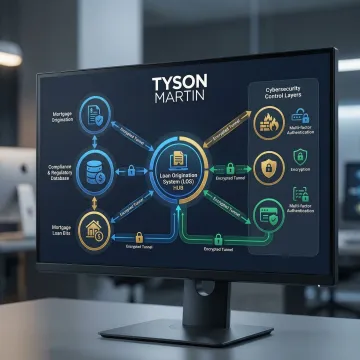

What technology risks are unique to mortgage banks that require specialized advisory expertise?

Mortgage banks face distinct technology risks including loan origination system availability during rate-sensitive periods, customer non-public information protection across multiple systems and vendors, compliance with evolving regulations like TRID and QM rules, third-party dependencies on title companies and appraisal services, and business continuity requirements that directly impact closing timelines. Specialized advisory expertise addresses these operational realities by focusing on risks that could disrupt lending operations, trigger regulatory violations, or compromise customer trust. You receive guidance that understands mortgage banking workflows, not generic cybersecurity recommendations.

How do you help mortgage bank boards understand and govern technology risk effectively?

Board cyber risk briefings translate technical risks into business impacts boards can act on—downtime effects on loan closings, vendor concentration risks, data breach disclosure obligations, and revenue impacts from system outages. Services include establishing technology risk appetite thresholds, creating decision rights for security investments, and implementing oversight dashboards that show trends rather than technical trivia. Boards receive one-page templates for quarterly updates, clear escalation criteria for incidents, and accountability frameworks that separate strategic governance from operational management. The result is confident oversight without micromanagement.

What deliverables can we expect in the first 90 days of engagement?

The first 90 days deliver tangible risk reduction and governance improvements. Expect a comprehensive risk assessment identifying top exposures specific to mortgage operations, incident response readiness validation including tabletop exercises, critical control coverage mapping for loan and servicing systems, board-ready dashboards with stable metrics and trend analysis, third-party risk register with vendor rankings by business impact, application portfolio assessment scoring technology investments, and a 90-day execution plan with assigned owners and measurable outcomes. Every deliverable focuses on decisions you can make and risks you can reduce, not reports that gather dust.

Do you provide ongoing support after the initial advisory engagement?

Yes. Engagement models are flexible based on your institution's needs. Options include transitioning to fractional CISO services for ongoing strategic leadership, quarterly board advisory sessions to maintain governance momentum, project-based support for specific initiatives like system migrations or M&A due diligence, or on-call advisory for incident response and regulatory matters. The goal is to build institutional capability while providing access to senior expertise when you need it most. You maintain decision rights and operational ownership while benefiting from strategic guidance that keeps technology risk aligned with business objectives.