Introduction

Cyber liability insurance is one of the hardest line items to budget accurately — because the exposure it covers keeps changing, and the premium rarely reflects what executives expect. According to IBM's 2025 Cost of a Data Breach Report, the global average cost of a data breach reached $4.88 million — a figure that excludes the secondary costs of regulatory scrutiny, litigation, and reputational damage that often follow.

What makes cyber liability insurance particularly difficult to budget is that there's no standard rate. A small professional services firm and a regional healthcare group can face dramatically different premiums — sometimes by a factor of ten — even when they carry similar revenue. Understanding what drives those differences is a governance decision that belongs at the executive and board level — not something to delegate to finance without security context.

What follows covers current premium ranges, the factors that move costs up or down, and the governance mistakes that create coverage gaps.

Key Takeaways

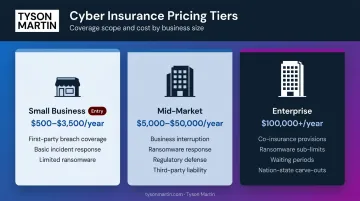

- Small businesses typically pay $500–$3,500/year; mid-market organizations pay $5,000–$50,000+; enterprise policies can exceed six figures

- The biggest cost drivers: industry, volume of sensitive data, security controls, coverage limits, and prior claims

- Strong controls — MFA, tested backups, and a documented incident response plan — reliably reduce what underwriters charge

- Cyber insurance is risk transfer — it works best alongside strong security governance, not as a substitute for it

How Much Does Cyber Liability Insurance Cost?

No flat rate exists for cyber liability insurance. Underwriters price each policy based on an individual risk assessment, and two businesses in the same industry with similar revenue can receive quotes that differ by thousands of dollars annually. That makes cost comparisons meaningful only when you understand the context behind them.

Entry-Level Coverage: Small Businesses and Lower-Risk Organizations

According to Insureon, small businesses typically pay between $500 and $3,500 per year, with many policies in the $1,000–$2,000 range depending on industry and data volume.

This tier generally includes:

- First-party data breach coverage (notification costs, forensics, crisis communications)

- Basic incident response support

- Limited ransomware coverage

Typically excluded: regulatory fines, extended business interruption, third-party liability, and nation-state attack losses.

Best fit for small professional services firms, consultants, and businesses handling limited personally identifiable information with basic but documented security controls.

As data volume, regulatory exposure, and operational complexity increase, so does the premium range. Mid-market organizations — regional healthcare groups, financial services firms, retailers with e-commerce operations — generally see annual premiums of $5,000 to $50,000, depending on those same underwriting factors.

Mid-Range Coverage: Mid-Size and Moderately Regulated Organizations

This tier expands coverage to include:

- Business interruption losses

- Cyber extortion and ransomware response

- Regulatory defense costs (partial)

- Third-party liability for client data breaches

Enterprise and High-Risk Coverage

Large enterprises, critical infrastructure operators, and technology companies managing client data at scale can pay $100,000 or more annually, with complex multi-tower programs reaching seven figures.

At this level, coverage comes with meaningful structural constraints:

- Co-insurance provisions that require the insured to share in losses

- Sub-limits on ransomware payouts, often well below the total policy limit

- Waiting periods before business interruption coverage activates

- Carve-outs for nation-state attacks and unpatched known vulnerabilities

Key Factors That Affect Cyber Liability Insurance Cost

Underwriters evaluate cyber risk the same way they evaluate any other insured exposure: through a structured assessment of likelihood and severity. Each factor below shifts where a business lands on the pricing spectrum — sometimes by a wide margin.

Industry and Regulatory Environment

Healthcare, financial services, and retail face higher premiums because the cost of a breach in those sectors — mandatory patient/customer notifications, regulatory penalties, and class-action exposure — is meaningfully higher than in lower-regulated industries.

Data from Security Magazine illustrates the gap clearly: healthcare and financial services organizations routinely pay multiples of what similarly sized professional services firms pay for equivalent coverage limits.

Volume and Sensitivity of Data Handled

More records mean greater potential breach costs. Underwriters look specifically at:

- Social Security numbers and government IDs

- Credit card and payment data (PCI scope)

- Protected health information (PHI)

- Employee PII at scale

A business processing 50,000 customer records faces a fundamentally different risk profile than one with 500.

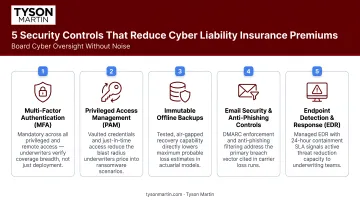

Security Controls and Cyber Hygiene

This is where the largest premium differences originate. Insurers now conduct detailed security questionnaires and, in some cases, automated scanning of a company's external attack surface before issuing a quote.

Controls that consistently lower premiums:

- Multi-factor authentication across email, remote access, and admin accounts

- Endpoint detection and response (EDR) tools

- Privileged access management with documented admin account reviews

- Tested, encrypted, offline backups with validated restore times

- Documented incident response plan with tabletop exercises in the past 12 months

Across underwriting reviews, the most common gaps driving premium increases are admin account sprawl, inconsistent MFA coverage, and backups that exist but have never been restore-tested. Insurers expect documentation — questionnaire responses backed by configuration exports, policy screenshots, or test results.

Coverage Limits, Deductibles, and Policy Structure

Higher coverage limits increase the premium; higher deductibles reduce it. But selecting a deductible your organization can't actually pay in a crisis defeats the policy's purpose.

Two structural details warrant close attention before signing:

- Sub-limits on ransomware: A $5 million policy limit with a $1 million ransomware sub-limit is common — and the gap rarely surfaces until a claim is filed.

- Deductible feasibility: A high deductible lowers premium but creates liquidity risk if the organization can't fund it mid-incident.

Claims History and Prior Incidents

A business with prior cyber claims is viewed as a higher-risk insured. Even incidents never formally claimed — discovered breaches, near-misses — can surface during underwriting through disclosure requirements or external scanning.

Breaking Down the Full Cost of Cyber Liability Insurance

The annual premium is only one component of the true financial exposure. Before purchasing a policy, understand all four cost categories:

| Cost Component | When It Applies | Notes |

|---|---|---|

| Annual premium | Recurring, paid regardless of claims | Base cost of maintaining coverage |

| Deductible | Per incident, before coverage activates | Typically $1,000–$2,500 for small business; higher for enterprise |

| Co-insurance / sub-limits | Applied at claim time | Requires insured to absorb a percentage; caps specific risks like ransomware |

| Coverage gaps / exclusions | Ongoing residual risk | Nation-state attacks, intentional employee acts, losses from unpatched known vulnerabilities |

The exclusion category deserves particular attention. Two scenarios consistently result in denied or reduced claims:

- Nation-state exclusions — now standard across most Lloyd's syndicates, meaning state-sponsored ransomware campaigns may not trigger coverage at all

- Unpatched known vulnerabilities — carriers frequently deny or reduce claims when a breach exploits a published vulnerability the organization had not yet remediated

How to Lower Your Cyber Liability Insurance Premium

Cyber premiums stabilized following steep hikes between 2020 and 2023, but underwriters have also raised their baseline security requirements. Shopping for a better quote helps less than improving the risk profile you present.

Implement the Controls Underwriters Require

Most insurers now mandate or specifically reward:

- MFA on all remote access, email, and administrative accounts

- Endpoint detection and response tools across the environment

- Privileged access management with documented account reviews

- Tested, encrypted offline backups with documented restore times

- A written incident response plan with tabletop exercise evidence from the past year

Organizations that cannot demonstrate these controls face restricted coverage, higher rates, or outright declinations.

Train Employees and Document the Program

Human error remains the leading cause of cyber incidents, and insurers price that risk. Organizations running documented security awareness training programs can qualify for meaningful premium reductions — but only if they can demonstrate it to an underwriter.

Carriers look for evidence, not intent. That means:

- Participation records and completion rates from training programs

- Phishing simulation results showing measurable improvement over time

- Verified managed detection and response (MDR) services, which some carriers credit directly

Adjust Policy Structure Strategically

Three structural levers reduce premium cost without reducing coverage quality:

- Raise the deductible — if the organization can sustain that out-of-pocket during an incident

- Bundle with other commercial lines — combining cyber with other policies from the same carrier often yields a discount

- Pay annually — upfront payment typically produces a 3–5% reduction versus monthly billing

Conduct a Pre-Application Security Assessment

Working with a cybersecurity advisor or conducting a third-party assessment before applying — or before renewal — lets an organization identify and remediate control gaps before underwriters see them. Addressing those gaps first prevents coverage restrictions and premium surcharges.

A fractional CISO or interim security leader can build and document the governance posture insurers reward: decision rights, escalation thresholds, tested incident response plans, and board-level metrics that show trend data rather than point-in-time snapshots. Carriers that see this level of documented oversight consistently offer more favorable terms.

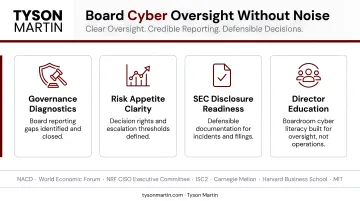

What Most Executives Miss When Budgeting for Cyber Insurance

Cyber insurance decisions are too often delegated entirely to procurement or legal, without the security context needed to make them well. Policies that look adequate on paper frequently leave significant gaps when an actual incident occurs.

Underwriters are paying closer attention to governance than most executives realize. Insurers now routinely ask about board-level visibility — who owns cyber risk, what the escalation thresholds are, and whether a named security leader is accountable for the program.

Organizations with clear decision rights, documented risk appetite statements, and a named security leader present a materially stronger profile than those without.

The three most common budgeting mistakes at the executive level:

- Focusing only on the annual premium while ignoring deductible and sub-limit exposure — the real out-of-pocket in a significant incident can far exceed the premium

- Treating a policy as a protection strategy rather than pairing coverage with active controls — insurers have sub-limits and exclusions for a reason

- Failing to revisit coverage limits after business growth, acquisitions, or significant changes in data volume or regulatory scope — a policy purchased three years ago may cover a fraction of actual exposure today

Frequently Asked Questions

What is the average cost of cyber liability insurance?

Small businesses typically pay $500–$3,500 per year. Mid-size organizations in moderately regulated sectors pay $5,000–$50,000+, and enterprise-level policies can exceed $100,000 annually. Industry, data volume, and security controls determine where any given organization falls within those ranges.

How much cyber insurance should a company have?

Coverage limits should reflect the realistic cost of a breach — including notification, forensics, legal defense, regulatory fines, and business interruption. The right amount depends on data volume, industry, and contractual obligations with clients or partners.

Should I get cyber liability insurance?

Any organization that stores, processes, or transmits sensitive data faces meaningful financial exposure from a cyber incident. Insurance is a critical component of a complete risk management strategy, but it works only when paired with security controls — not as a replacement for them.

What is cyber liability insurance for small businesses?

Small business cyber liability insurance typically covers first-party breach costs — notification, forensics, and crisis management. Policies can be customized to include ransomware response, business interruption, and third-party liability, though exclusions vary significantly by carrier.

What factors have the biggest impact on cyber liability insurance premiums?

The five factors underwriters weight most heavily:

- Industry and regulatory exposure

- Volume and sensitivity of data handled

- Strength of security controls (especially MFA and backup integrity)

- Coverage limits selected

- Prior claims history

Security controls are increasingly the primary differentiator between competitive and elevated premiums.

How can a company reduce its cyber liability insurance costs?

Practical steps that directly reduce premiums:

- Implement required controls: MFA, EDR, tested backups, and a documented IR plan

- Maintain records of employee security training

- Choose a deductible your organization can actually sustain

- Bundle policies where carrier options allow

- Work with a security advisor to strengthen your risk profile before underwriting begins