The evidence is hard to ignore. When Verizon discovered undisclosed cyberattacks during its Yahoo acquisition, the deal price dropped by $350 million, settling at $4.48 billion. Altaba (formerly Yahoo) later paid a $35 million SEC penalty for failing to disclose the breach to investors. Marriott acquired Starwood's breach history along with its hotel portfolio — and inherited both a £18.4 million ICO fine and a 2024 FTC order requiring a complete security program overhaul.

These aren't edge cases. A Forescout survey of 2,779 IT and business decision-makers found 53% had encountered a critical cybersecurity issue that put a deal in jeopardy, and 65% reported buyers' remorse due to cyber concerns after closing.

The core problem: M&A timelines move fast, legal and financial teams dominate the process, and cybersecurity gets compressed into a late-stage checklist. This article covers the full lifecycle — from pre-deal due diligence through post-close integration — and what leadership teams must get right at each stage.

Key Takeaways

- Undisclosed breaches have repriced, restructured, and killed deals — Yahoo/Verizon being the most cited example

- Cyber due diligence must start before the term sheet, not after it's signed

- The pre-close window carries peak risk: new access, wire transfers, and distracted teams create cover for attackers

- Post-close integration expands the attack surface and requires sustained monitoring, not a one-time assessment

- Boards are now accountable for cyber oversight under SEC disclosure rules, including during M&A

Why Cybersecurity Can Make or Break an M&A Deal

The M&A transaction window is unusually attractive to threat actors. Systems are being connected, personnel are uncertain about their roles, and defensive attention is divided across legal, financial, and operational workstreams. Gaps open — some deliberately exploited, others simply inherited.

The FBI IC3's 2025 annual report recorded $20.877 billion in cyber-enabled crime losses — a 26% increase from the prior year — across more than one million complaints. That's the environment in which M&A transactions are being executed today.

The Inherited Liability Problem

When an acquirer absorbs a target's undisclosed breach history, unpatched systems, or non-compliant data practices, those costs transfer at close. The seller is gone. The liability isn't.

The Marriott/Starwood acquisition is the instructive case. Marriott acquired Starwood in 2016. The Starwood breach had already occurred, but Marriott didn't discover it until 2018.

What followed: a £18.4 million (~$23 million) ICO penalty, a 2024 FTC final order, and years of regulatory scrutiny. None of that was priced into the original deal.

How Cyber Risk Affects Valuation

Vulnerabilities introduce uncertainty into projected cash flows, remediation costs, and regulatory exposure. Sophisticated acquirers translate that uncertainty directly into deal economics:

- Price reduction — as Verizon demonstrated with Yahoo

- Escrow provisions — funds held pending remediation milestones

- Representations and warranties — contractual disclosure requirements tied to indemnification

- Closing conditions — remediation required before a deal can proceed

- Walk-away rights — material undisclosed incidents as deal breakers

That last point isn't theoretical. According to Forescout research, 73% of respondents said an undisclosed breach would be an immediate deal breaker in their company's M&A strategy.

Both sides carry risk. Sellers with weak controls face price reduction or deal loss. Buyers who skip proper assessment absorb those vulnerabilities — plus the regulatory penalties that follow.

Cybersecurity Due Diligence: What Acquirers Must Assess Before Signing

Due diligence must begin before a term sheet is finalized — not after. Early discovery gives acquirers negotiating leverage: require remediation as a deal condition, adjust price, or exit cleanly. The Forescout survey found only 36% of IT decision-makers strongly agreed their teams were given adequate time to review a target's cybersecurity standards before close.

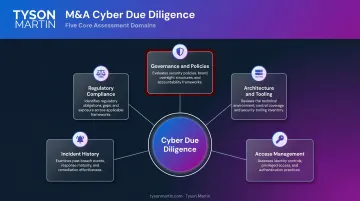

Assessing the Target's Security Posture

A thorough posture assessment goes well beyond a vulnerability scan. It should cover:

- Governance and policies — security frameworks in use, policy documentation, ownership

- Architecture and tooling — network controls, cloud infrastructure, endpoint inventory

- Access management — privileged access practices, identity systems, admin account hygiene

- Incident history — material security events in the past 24 months, unaddressed audit findings

- Compliance gaps — HIPAA, PCI-DSS, GDPR, CCPA, SOX — depending on industry and geography

The difference between a scan and a real assessment is depth. A structured assessment probes questions that a checklist won't surface:

- What visibility does the security team actually have into endpoints and cloud workloads?

- Are there data residency risks that conflict with the acquirer's footprint?

- Have any audit findings gone unresolved for more than 90 days?

Organizations without a dedicated CISO — common among mid-market targets — often benefit from bringing in an independent advisor to lead or validate this work.

Tyson Martin's M&A cyber due diligence engagements run three to four weeks and deliver a target risk profile, a board red-flag memo, a post-close remediation roadmap, and a valuation impact assessment. The work is conducted independently of the target's own security team and vendors, which matters when objectivity is the point.

Mapping Third-Party and Vendor Risk

Even a well-secured target can carry significant exposure through its vendor ecosystem. Third-party relationships must be inventoried and assessed as part of diligence scope — posture is only as strong as the least-secure supplier.

According to Verizon's 2026 Data Breach Investigations Report, third parties were involved in 48% of breaches — up 60% from the prior year's dataset. The exposure vendor relationships carry doesn't stop at M&A boundaries.

Key assessment areas for vendor risk:

- Complete third-party inventory ranked by business criticality

- Vendor contracts reviewed for security requirements, breach notification timelines, and audit rights

- Concentration risks — single-cloud, single-identity-provider, or single-MSP dependencies

- Unmanaged SaaS spend and data-sharing contracts that may not fit the combined entity

Evaluating Regulatory Compliance

Inherited noncompliance becomes the acquirer's problem at close — regulators don't accept "we didn't know" as a defense. Depending on the target's industry and geography, gaps may include:

- HIPAA — healthcare and adjacent industries

- PCI-DSS — any company handling cardholder data

- GDPR / CCPA — data privacy obligations tied to customer geography

- SEC disclosure rules — public companies subject to material incident reporting

- SOX — financial reporting controls for public entities

Post-close compliance gaps generate real costs. Marriott's acquisition of Starwood illustrates the stakes: the inherited breach — undiscovered for four years — ultimately drew a £99 million ICO fine and years of remediation work that fell entirely on the acquirer.

Incident Response Capabilities

A documented incident response plan is not the same as a functioning one. Assess whether the target's IR plan has been tested, exercised, and is owned by named individuals. IBM's 2025 Cost of a Data Breach Report puts the global average breach cost at $4.44 million — a figure that effective incident response planning can materially reduce through faster detection and containment.

The Pre-Close Window: When Cyber Risk Peaks

The days immediately before closing carry the highest concentration of risk. Approvals are being issued. Systems are being granted new access. Wire transfers are being authorized. And everyone's attention is on the finish line, not the perimeter.

That's exactly when monitoring should be heightened — not relaxed.

Crown Jewel Identification

Before any systems are connected, acquirers should identify which digital assets are mission-critical. Not all assets are equal — intellectual property, customer data, financial systems, and core infrastructure carry different risk profiles. The integration plan should reflect that hierarchy explicitly.

Tyson Martin's 45-day post-acquisition framework begins with a crown jewels map tied to business services: what data matters, where it lives, and how it moves. That map drives everything else — what gets protected first, what gets connected last, and what requires board-level escalation if compromised.

Access and Identity Controls

During the pre-close period, specialists, bankers, IT consultants, and advisors may require access to sensitive systems. Strict identity and access management controls must be enforced:

- Approved user lists with documented business justification

- Time-limited access that expires automatically

- Full audit logging of all privileged activity

- MFA enforced across all new access grants

Insider risk deserves specific attention here. Employees facing role elimination may download intellectual property or sensitive data before close. Verizon's 2024 DBIR found internal actors responsible for a meaningful share of breaches, with end users accounting for the majority of those incidents. That risk is amplified when headcount uncertainty is high.

Written Integration Plan With Clear Decision Rights

A cybersecurity integration plan must be written, decision-mapped, and stress-tested before it's needed. Key elements include:

- Who owns each security decision during integration

- What gets connected when, and what the "ready-to-connect" criteria are

- How security concerns escalate — to whom, on what timeline

- What triggers board-level notification

When decision rights aren't defined in advance, every security question becomes a negotiation under pressure. A plan that can't hold up during a tense close isn't a plan — it's a placeholder.

Post-Close Integration: Building a Secure Combined Entity

Post-close is when theoretical vulnerabilities become operational ones. New hybrid networks create new attack surfaces. Legacy systems connect to modern environments with different security assumptions. Monitoring gaps emerge across seams that didn't exist before.

53% of IT decision-makers reported finding unaccounted IoT or OT devices after completing acquisition integration — assets that weren't in the inventory, now connected to the combined network.

A one-time scan at close is not sufficient. Sustained threat monitoring of imported systems is required throughout the integration period. The same discipline applies to the people side of integration.

Managing Insider Risk Post-Close

The insider threat window extends well past closing. Employees facing role changes or elimination represent an elevated risk — departures spike after close, and so does the risk of data exfiltration.

Structured monitoring during this period should include:

- Behavioral analytics on accounts belonging to employees in affected roles

- Automatic disabling of accounts for departing employees on their last day

- Locking down local admin rights and stale accounts as immediate priorities

- Clear policies defining who can approve access changes and for how long

This doesn't require creating a surveillance culture. It requires the same access hygiene that should exist in any well-run organization — applied consistently during a period when the stakes are higher.

Continual Governance Reassessment

What was acceptable risk pre-close may not be acceptable in the combined entity. Risk tolerance, compliance obligations, and operational dependencies change when two organizations merge.

Boards and leadership teams should establish a regular review cadence — not treat integration as a one-time project with a fixed end date. Full integration can take 12 to 24 months depending on complexity. A structured 90-day security stabilization period addresses the most urgent work — but the board's oversight role doesn't end there. Governance checkpoints at 90 days, 6 months, and 12 months give leadership the visibility needed to confirm that security posture is improving, not just stabilizing.

The Board's Role in M&A Cybersecurity Governance

Boards are now expected — by regulators, shareholders, and auditors — to demonstrate active oversight of cybersecurity risk. That expectation doesn't pause during M&A. If anything, the stakes are higher.

The SEC's 2023 cybersecurity rules (effective September 5, 2023) require material incident disclosure on Form 8-K within four business days of a materiality determination, and annual disclosure of board oversight processes under Regulation S-K Item 106. Boards that treat cyber as a purely technical matter during M&A face real legal and financial exposure — the SEC's $35 million action against Altaba for non-disclosure demonstrates what enforcement looks like.

What Effective Board Oversight Looks Like

Boards don't need to get into technical details. They need to ask the right questions — clearly, consistently, and early enough to matter:

- Has a full cybersecurity assessment of the target been completed?

- What are the top three inherited risks and who owns remediation?

- What is the integration timeline and who holds security decision authority?

- What triggers board escalation if an incident occurs pre- or post-close?

- Are compliance gaps identified, and what is the remediation plan?

Getting those questions answered reliably requires more than good intentions. Organizations navigating M&A without a permanent CISO — or with a CISO who lacks board communication experience — benefit from an independent advisor who can bridge governance and execution.

Tyson Martin's board advisory work translates technical findings into the terms boards act on: financial exposure, legal risk, operational impact, and brand trust — without drowning directors in technical noise.

Common Cybersecurity Mistakes That Derail M&A Deals

Mistake 1: Treating Cyber as a Late-Stage Checklist

By the time legal teams are negotiating representations and warranties, it's too late to walk away cleanly from a material vulnerability. Early-stage cyber screening allows acquirers to negotiate remediation requirements, adjust price, or exit before significant deal costs have been incurred.

Only 36% of IT decision-makers in the Forescout survey said their teams had adequate time for pre-close cyber review. The cost of that compressed timeline shows up in buyers' remorse statistics — and in post-close remediation bills.

Mistake 2: Connecting Systems Too Quickly

Pressure to realize synergies fast regularly overrides secure integration discipline. The result: one company's security problem becomes both companies' problem.

Connectivity should follow security readiness, not the calendar. Before any network connections are established, establish visibility into admin access and endpoints on both sides. Run systems in parallel where necessary. Define explicit "ready-to-connect" criteria — and hold to them even when business teams push for speed.

Mistake 3: Failing to Rationalize Access Rights

Permissions inherited from an acquired company often far exceed what the new role requires. Accounts that were appropriate in the target's environment may carry excessive privileges in the combined entity.

Least-privilege enforcement in the first 90 days post-close should include:

- Immediate lockdown of stale accounts and local admin rights

- Review of privileged access across both entities

- Clear joiner/mover/leaver processes that account for the acquisition's organizational changes

- MFA enforcement across all newly migrated accounts

Left unaddressed, over-permissioned accounts create the exact conditions that enable months-long data exfiltration to go undetected — often long after the deal has closed.

Frequently Asked Questions

Frequently Asked Questions

How does a cybersecurity breach affect M&A deal value?

Undisclosed breaches or weak security controls can reduce a target's valuation, trigger price renegotiation, or collapse a deal entirely. Verizon reduced the Yahoo purchase price by $350 million after discovering undisclosed attacks, and 73% of M&A decision-makers in the Forescout survey said an undisclosed breach would be an immediate deal breaker.

When should cybersecurity due diligence begin in the M&A process?

Due diligence should begin at the initial screening phase — before a term sheet is signed. Early discovery gives acquirers leverage to negotiate remediation requirements into deal terms, require price adjustments, or exit before substantial costs accumulate.

What are the biggest cybersecurity risks during M&A integration?

The three highest-risk areas are:

- Expanded attack surface from connecting previously separate systems

- Insider threats from employees facing role changes or elimination

- Legacy system vulnerabilities that activate when merged with modern environments

What should a board ask before approving an M&A deal from a cybersecurity standpoint?

Key questions: Has a full security assessment been completed? What are the top inherited risks and who owns remediation? Who holds cybersecurity decision authority during integration, and what triggers escalation to the board?

What is the role of a CISO in an M&A transaction?

The CISO leads technical due diligence, defines integration security standards, and serves as the primary risk advisor to the deal team. Organizations without a permanent CISO often bring in a fractional CISO for transaction support, gaining pattern recognition from multiple deals that an internal generalist team may lack.

How long does post-M&A cybersecurity integration typically take?

Full integration typically takes 12 to 24 months depending on organizational complexity. The highest-risk window is the first 90 days — access controls, network connections, and governance structures must be stabilized before broader integration proceeds.