Introduction

Audit committees were built for a specific job: financial reporting, internal controls, external auditor management. That job hasn't disappeared — but it's now surrounded by a much larger one.

Cybersecurity, AI governance, data privacy, geopolitical disruption, operational resilience. These risks keep landing on audit committee agendas not by design, but because they had nowhere else to go.

Recent research from Russell Reynolds Associates, based on interviews with 15 audit committee chairs, is direct: financial reporting is now "table stakes." The real pressure comes from risks that are less structured, less standardized, and harder to delegate. The CPA Journal's April 2026 analysis confirms it: audit committees must function as enterprise-wide risk stewards, not just financial watchdogs.

This article covers what that shift looks like in practice — the emerging risks dominating boardroom agendas, what effective oversight actually requires, and how committees can govern intelligently without crossing into management's lane.

Key Takeaways

- Audit committees have become the board's default destination for enterprise risk — absorbing cyber, AI, and operational risks that lack clear ownership elsewhere.

- AI, cybersecurity, and data privacy are one interconnected governance challenge, not three separate agenda items.

- Effective committees prioritize ruthlessly: agenda design is a strategic discipline, not an administrative task.

- Composition gaps around technology fluency are forcing boards to rethink who belongs in the room.

- PCAOB transitions, SEC enforcement trends, and proxy advisor updates are accelerating — committees that aren't tracking them are already behind.

The Expanding Mandate: From Financial Oversight to Enterprise Risk Stewardship

The audit committee's original scope was clear. Financial reporting. Internal controls. External auditor relationships. Discrete, bounded, and manageable.

That clarity has eroded steadily — not through a single decision, but through accumulation.

The "Catcher's Mitt" Problem

Eric Brandt, quoted in the Russell Reynolds study, described it directly: "The audit committee has become the catcher's mitt for anything that doesn't have a clear home."

Cybersecurity. Data privacy. AI governance. Trade and tariff volatility. Geopolitical disruption. Each of these migrated onto audit agendas because another committee didn't own them, and the audit committee was the default destination for enterprise-level risk.

The irony is that financial reporting — the original mandate — has become the most stable part of the role. Mature finance organizations, experienced auditors, and well-established processes have routinized it. That stability means more committee bandwidth now flows toward risks that are harder to evaluate, harder to measure, and harder to delegate.

The Accountability Without Control Dynamic

Audit committee chairs carry fiduciary responsibility for risks they don't manage day-to-day. They must challenge, probe, and anticipate without crossing into management's operational territory — and that line keeps moving as scope expands.

BDO's 2025 Audit Committee Priorities report puts numbers to the pressure:

- 47% of organizations assign ERM oversight primarily to the audit committee

- 31% of directors identify enterprise risk management as the governance process requiring the most time and effort over the next 12 months

- 73% of directors discuss cybersecurity on a quarterly basis

- 27% expect to spend significant time evaluating committee structure and responsibilities

Broader agendas without more meeting time force difficult prioritization decisions. When the mandate outgrows the structure, that's a governance design problem — and restructuring the committee's scope is the only durable answer.

Cyber, AI, and Data: One Interconnected Governance Challenge

The instinct to treat cybersecurity, AI risk, and data privacy as separate agenda items is understandable. Each has its own vocabulary, its own regulators, its own set of technical specialists. But that separation creates blind spots at the board level.

PwC's AI oversight framework for audit committees identifies six oversight areas where AI intersects directly with existing audit committee responsibilities: financial reporting and internal controls, internal audit, external audit, compliance and fraud prevention, risk management, and cybersecurity. AI doesn't sit outside these domains — it runs through all of them.

Data integrity failures cascade across all three areas simultaneously. AI amplifies existing cyber vulnerabilities. Disclosure obligations tie them together. A committee that governs these topics in separate silos misses the connections that matter most.

What This Looks Like in Practice

According to CAQ and Ideagen Audit Analytics, 64% of S&P 500 boards have assigned cybersecurity oversight to the audit committee. Yet the structural model hasn't fully caught up with the reality of convergence — committees still receive separate briefings on AI initiatives, cyber risk, and data privacy rather than an integrated risk picture.

The AI governance gap is notable. NACD's 2025 survey found that more than 62% of directors say boards now set aside agenda time for AI — but fewer than 1 in 4 have formal governance practices in place. Setting aside time is a starting point, not a governance model. Without defined oversight responsibilities, escalation thresholds, and reporting cadence, AI risk remains unmanaged regardless of how often it appears on the agenda.

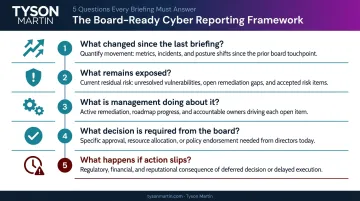

What Board-Ready Cyber Reporting Actually Looks Like

Audit committees typically receive too much of the wrong information, not too little. Dense, activity-based briefings that report patch counts, training completion rates, and tool rollouts give committees no basis for making decisions — and no way to distinguish a worsening situation from a stable one.

Board-ready cyber reporting, by contrast, is structured around five questions:

- What changed since the last briefing?

- What remains exposed?

- What is management doing about it?

- What decision is required from the board?

- What happens if action slips?

Effective reporting shows trend over time — not a one-time snapshot. It connects cyber risk to business outcomes: financial reporting integrity, operational uptime, customer trust, and legal exposure. And it uses a consistent format so committees can track movement rather than reconstruct context at every meeting.

Tyson Martin's board advisory work addresses this translation problem directly — converting technical cyber briefings into one-page, decision-ready summaries with clear ownership, escalation thresholds, and trend lines. The output is a stable dashboard that shows direction and momentum, not activity volume.

What Effective Audit Committee Oversight Actually Looks Like

Good governance doesn't start when the meeting begins. It starts weeks earlier — in agenda design, pre-read materials, and the informal conversations that shape what actually gets discussed.

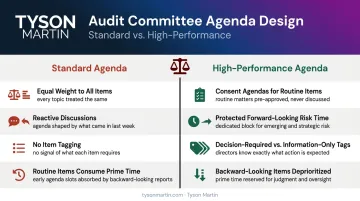

Agenda Design as a Leadership Discipline

The agenda is not an administrative artifact. It determines what the committee actually does with its limited time. High-performing committees:

- Use consent agendas to handle routine items without consuming prime meeting time

- Protect time for forward-looking risk discussions

- Tag every agenda item explicitly as decision-required or information-only

- Move backward-looking items out of prime time

When every item gets equal weight, nothing gets adequate attention. Agenda design is how committees make that tradeoff explicit.

Pre-Meeting Materials That Work

Best practice calls for delivering materials one week in advance, structured to enable judgment rather than just comprehension:

- Concise executive summaries per major item

- Dashboards with trend lines, not raw data

- Clear notation of what changed since the last meeting

- Technical appendices for those who want depth

Information overload is a governance failure, not just an inconvenience. When committees receive 40-slide presentations with no clear ask, they default to passive reception rather than active judgment.

Between-Meeting Engagement

Regular one-on-ones between the committee chair and the CFO, Chief Audit Executive, CRO, CISO, and General Counsel serve several functions beyond what formal meeting time allows:

- Surface emerging risks before they become formal agenda items

- Build the trust that makes formal sessions more candid

- Allow the chair to shape upcoming agendas based on real-time awareness

Chairs who do this stay ahead of issues rather than reacting to them.

Private Sessions as an Underused Tool

Executive sessions — committee only, without management present — create space for questions that formal presentations suppress. Pre- and post-meeting private sessions with key executives serve the same function. In practice, they enable:

- Candid course-correction without the constraints of the formal record

- Sensitive escalation that wouldn't surface in a full session

- Direct feedback to executives that improves the next meeting, not just this one

These tools are available to every audit committee. Most use them infrequently.

Structural Realities: Composition and Scope Creep

The Composition Gap

What counted as specialized expertise two years ago has become a baseline expectation. No single director can possess deep expertise across finance, operations, technology, cyber, regulatory affairs, and risk management. The goal isn't to find unicorns — it's to build a committee where the necessary fluency exists collectively.

CAQ's 2025 data shows 65% of S&P 500 boards now disclose having a cybersecurity expert — up from 51% in 2023. That's meaningful progress, but board-level expertise doesn't automatically translate to effective audit committee oversight.

The committee needs members who can engage with technical risk in business terms, ask the right questions, and recognize when a briefing is performance rather than substance.

When Charters Don't Keep Up

Composition gaps often surface a deeper structural problem: charters that haven't kept pace. Additional responsibilities accumulate, meeting structures don't change, and the committee ends up carrying an expanded mandate with a governance design built for a different era.

The practical fix isn't complicated, but it requires deliberate action:

- Map which risks landed in the committee by default versus by intentional design — that distinction matters for accountability.

- Assess whether the current scope creates coherent enterprise oversight, or whether fragmentation across committees is quietly producing blind spots.

- Revisit the charter — not just rolling it forward annually, but genuinely re-examining whether composition, scope, and time allocation match today's risk environment.

For committees without a standalone risk or technology committee, the audit committee typically absorbs everything. That's a legitimate structure — but it requires explicit time allocation, clear escalation thresholds, and a committee composition that reflects the actual scope of oversight being asked for.

The Regulatory Landscape Audit Committees Can't Ignore in 2026

PCAOB Transitions and Standard-Setting

The PCAOB is in transition. Chair Erica Y. Williams departed on July 22, 2025. Board Member Christina Ho concluded service effective January 31, 2026. Leadership continuity at the PCAOB affects the pace and direction of standard-setting — and audit committees should be asking their external auditors how these changes affect upcoming audit cycles.

Active standards and amendments to track:

- QC 1000 (Quality Control) — effective December 15, 2025

- Technology-assisted analysis amendments — effective for fiscal years beginning on or after December 15, 2025

- Fraud and going-concern revisions — in progress; public comment requested March 2026

Each of these directly shapes how external auditors conduct work and what they're required to communicate to committees — making them practical agenda items, not background reading.

SEC Enforcement Trends

The Anti-Fraud Collaboration's analysis of 148 PCAOB disciplinary orders and 255 SEC accounting enforcement releases from 2021 through 2024 identified a clear pattern: revenue recognition remains the top regulatory focus, and inconsistent post-M&A accounting is an increasing PCAOB priority.

Audit committee communications themselves are also under the enforcement lens. How committees document their oversight — not just what they oversee — is now a factor regulators examine.

Proxy Advisor Updates

That same documentation scrutiny extends to how institutional investors read governance quality. Glass Lewis published its 2026 U.S. Benchmark Policy Guidelines with updates to pay-for-performance methodology and board responsiveness thresholds. ISS finalized its 2026 benchmark policy changes in December 2025. Audit committees that treat these as investor-relations issues — rather than governance ones — create exposure well beyond financial reporting.

Practical Steps for Boards Ready to Raise Their Governance Game

The gap between governance on paper and governance in practice usually comes down to three things: unclear scope, inadequate reporting, and the absence of an independent outside perspective.

Start with a mandate audit. Map the committee's current responsibilities against today's risk environment — not last year's charter. Identify explicitly which risks landed in the committee by design and which accumulated by default. Make intentional decisions about what belongs in audit, what should escalate to the full board, and what should move to a separate committee if the organization has one.

Fix the reporting before the next crisis. If the committee's current cyber and technology reporting can't answer "what changed, what's at risk, and what decision is needed" — that's the problem to solve before an incident forces the question. A stable, one-page dashboard with trend lines and clear decision points is achievable with the right structure. That transition — from dense technical briefings to decision-ready reporting — is the core of how Tyson Martin structures board advisory work: plain-English risk posture, defined escalation thresholds, and a 90-day plan with named owners and measurable outcomes.

Treat continuous improvement as a committee function. High-performing committees don't wait for a crisis to recalibrate. Specifically, they:

- Run annual self-assessments against charter and risk environment

- Rotate topic leads to distribute expertise across members

- Arrange targeted education sessions on emerging risks

- Seek periodic feedback from management and external auditors

Left unattended, committee effectiveness drifts. Treated as a function, it compounds.

Bringing in an external perspective during governance transitions, M&A activity, or periods of elevated technology risk gives the committee something the in-house CISO can't provide: independence.

An advisor who understands both the technical risk landscape and boardroom communication norms can validate that what management is reporting is accurate, decision-relevant, and appropriately structured — without undermining the internal team.

Frequently Asked Questions

What should audit committees prioritize in 2026?

Current research points to five priorities competing for limited meeting time:

- Agility in a shifting geopolitical and regulatory environment

- Financial reporting and disclosure complexity

- AI and technology risk oversight

- Fraud detection and internal controls monitoring

- Communicating risk posture clearly to the full board

The hard part is sequencing these against a finite agenda.

How should audit committees oversee AI and cybersecurity risks?

Treat them as one interconnected conversation, not separate agenda items. AI amplifies cyber risk, so siloing them produces blind spots. Confirm that the committee receives trend-based reporting, and that escalation thresholds and decision rights are defined before an incident forces the question.

What skills should audit committee members have today?

Financial expertise remains foundational but no longer sufficient. Members need working fluency (not deep technical mastery) in cybersecurity, AI governance, and operational risk, plus the judgment to integrate those domains at the enterprise level. The goal is a committee that asks the right questions, not one that tries to answer them unilaterally.

How often should audit committees engage with the CISO or technology leadership?

Leading committees maintain regular between-meeting touchpoints with the CISO and CTO, not just formal briefings. That cadence keeps the committee ahead of emerging risks, shapes upcoming agendas, and ensures formal presentations reflect what directors need to make decisions rather than what management finds easiest to report.

What is the difference between board-level and management-level cyber oversight?

Management owns cyber risk execution: detection, response, controls, and day-to-day operations. The board's role is to set oversight expectations, confirm clear escalation paths exist, approve risk appetite, and ensure reporting is trustworthy and decision-relevant. When those boundaries blur, accountability for risk acceptance becomes unclear and ownership of risk decisions disappears.

How can audit committees tell if their cyber risk reporting is actually effective?

Effective reporting shows trend over time, reflects what changed since the last briefing, and is structured around risk posture rather than activity volume. A practical test: could the committee make a defensible governance decision based solely on what they received? If not, ask management to reframe the next briefing around decisions the board actually needs to make.