The implications for portfolio company leadership are direct. A weak security posture can depress valuations, trigger mandatory post-close remediation spend, or invite targeted attacks at precisely the moments when a company is most exposed — during fundraising, integration, or an approaching IPO. Boards and executive teams at PE-backed companies can no longer treat this as someone else's problem.

This article covers what PE firms are actually requiring, when portfolio companies face the greatest exposure, what credible board oversight looks like in practice, and how to build a program that satisfies investor expectations without a multi-year transformation.

Key Takeaways

- 96% of PE firms require formal governance policies including incident response plans; 95% mandate baseline technical controls like MFA and privileged access management

- 97% require portfolio companies to provide ongoing visibility and incident reporting after deal close

- Among PE respondents, 54% reported that up to 25% of their portfolio companies experienced a cyber incident in the past year

- Highest-risk windows: pre-deal data sharing, post-announcement, and IT integration

- Boards bear direct accountability — PE firms want evidence of dedicated cyber leadership, not just an IT team with security responsibilities

Why Cyber Has Become a Core PE Investment Criterion

The Regulatory and Market Pressure Is Real

For two consecutive years, cyber threats have ranked among the top global risks in the World Economic Forum's Global Risks Report — fifth in the two-year outlook and eighth over ten years in 2025. That consistent ranking has moved cybersecurity out of the compliance column and into enterprise risk conversations at the board level.

Regulatory pressure is accelerating this shift. The SEC's 2023 cybersecurity disclosure rules require public companies to report material incidents within four business days and disclose how their board oversees cyber risk. PE firms preparing portfolio companies for IPO or strategic sale are building toward these standards years in advance, well before the S-1 stage forces the issue.

Regulatory requirements aren't the only external force. Insurance markets are applying the same pressure from a different direction. Insurers now require documented technical controls before issuing cyber coverage, and PE firms increasingly view an uninsurable portfolio company as carrying deal-level risk. According to QBE's 2025 Private Equity Cyber Survey, 60% of PE respondents said fewer than half of their target companies had cyber insurance coverage before investment.

Breaches Damage More Than the Balance Sheet

The 2025 IBM Cost of a Data Breach Report puts the average global breach cost at $4.44 million — but that number understates the real impact for PE-backed companies. Remediation costs can be budgeted for. Customer trust, brand perception, and exit multiples cannot be reimbursed. A breach in the 12 months before a planned sale doesn't just cost money — it creates renegotiated deal conditions, price adjustments, and mandatory escrow provisions that compress returns.

Threat actors have gotten smarter about timing their attacks, too. Several signals that routinely attract attention include:

- Due diligence disclosures — data-rich processes that expand the target surface temporarily

- Funding announcements — public signals of high-value assets with potentially incomplete defenses

- Integration activity — transitional periods when security controls are often in flux

The Specific Windows of Vulnerability for Portfolio Companies

PE-backed companies face elevated risk at four distinct points in their lifecycle. Understanding these windows is the first step to defending them.

Pre-Deal and Pre-Announcement

Before a deal closes, sensitive financial, legal, and operational data moves across multiple parties. That data flow creates real exposure — and Deloitte's M&A cyber due diligence practice notes that digital footprint analysis during this period regularly uncovers typosquatting and lookalike domains designed to intercept deal communications. Employees involved in corporate development are among the most targeted individuals in any transaction.

Post-Announcement

Public funding announcements draw attention from threat actors who view newly backed companies as high-value, potentially under-defended targets. The ransom calculus is simple: a company that just closed a $200M round has both the resources to pay and the reputational pressure to make a problem go away quietly.

Among portfolio companies that had already experienced a cyberattack, 46% of PE respondents reported that 26% to 50% of those companies faced ransomware or extortion incidents specifically.

IT Integration

Integration is where structural risk catches up with external threats. As two systems start connecting, attack surfaces expand faster than most teams anticipate:

- Access controls get temporarily relaxed during cutover periods

- Credential management becomes inconsistent across merged environments

- Network segmentation that held in a standalone setup develops gaps

KPMG's 2025 Technology Sector M&A Survey found 71% of PE/VC respondents identified cybersecurity risks as a key consequence of unaddressed tech debt — and integration is exactly when that debt comes due.

Third-Party and Vendor Risk

Post-investment growth typically means adding vendors. Each new vendor is an access point. This risk compounds quickly without a structured vendor tiering process, and without tiering in place, the cost of discovery tends to arrive after a vendor has already been granted access — not before.

What PE Firms Are Now Requiring: The Full Spectrum

The QBE survey data is specific enough to function as a compliance checklist. Here's what PE firms are actually mandating:

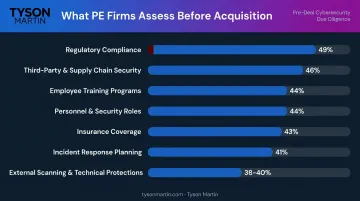

Pre-Deal Due Diligence

PE firms assess multiple areas before acquiring a company. The top categories evaluated (with the percentage of firms conducting each):

- Regulatory compliance: 49%

- Third-party and supply chain security: 46%

- Employee training programs: 44%

- Personnel and security roles: 44%

- Insurance coverage: 43%

- Incident response planning: 41%

- External scanning and technical protections: 38–40%

These are the exact questions an acquirer's due diligence team will ask. Leadership that runs a proactive assessment against this list enters any process with a defensible starting point.

Post-Acquisition Technical and Governance Requirements

Where pre-deal reviews vary by firm, post-close mandates converge sharply — nearly every PE firm requires the same three things:

| Requirement | % of PE Firms Requiring |

|---|---|

| Incident visibility and reporting | 97% |

| Governance policies (IR plans, data classification, asset management) | 96% |

| Baseline technical controls (MFA, PAM, endpoint protection, DLP) | 95% |

Ongoing Oversight Cadence

Cyber oversight doesn't stop at deal close. PE firms conduct post-acquisition reviews on the following schedule:

- Monthly: 23%

- Quarterly: 34%

- Semi-annually: 21%

- Annually: 19%

- Multiple times per month: 3%

Most portfolio companies face at least quarterly scrutiny. That cadence demands governance infrastructure with clear ownership, a stable reporting format, and metrics that hold up across every review cycle — not documentation assembled in the weeks before each check-in.

The Board's Role in Meeting PE Cybersecurity Expectations

Establishing Decision Rights Before Pressure Hits

Boards don't manage security operationally — but they own the decision rights architecture. The specific questions a PE firm will ask are: Who can declare an incident? Who has authority to shut systems down? Who owns external disclosure? When those answers are unclear, risk gets expensive fast.

That's why effective boards establish escalation thresholds before an incident forces the question. That means defining what requires board escalation, what stays with management, and who can accept risk on the organization's behalf. A RACI-style decision-rights map — covering the CEO, COO, General Counsel, and Security leadership — gives everyone pre-approved authority during high-pressure situations.

What Useful Board Reporting Actually Looks Like

Most boards receive technical reports designed for security operations teams. What directors actually need is a stable dashboard covering:

- Top enterprise risks — with named owners and directional trend (improving, stable, worsening)

- Incident readiness signals — backup restore test results, response time targets

- Control health on critical assets — identity, patching, logging status

- Third-party exceptions that could affect operations

- Decisions required — funding approvals, risk acceptances, escalations

The format should fit on one to two pages. Eight to twelve metrics maximum, each with a target, a trend, and a trigger. Boards that receive raw scan counts or tool feature lists cannot govern effectively — they can only react.

The Dedicated Cyber Leadership Expectation

PE firms want evidence of qualified cyber leadership at the executive level. That means a named owner accountable for program governance, board reporting, and incident response — not necessarily a full-time CISO, but someone with clear authority.

For boards navigating this expectation, Tyson Martin's board advisory and interim CISO engagements deliver the governance artifacts PE firms look for. Within the first 30 days, an engagement produces a ranked risk list with business impact, a decision-rights map, a 90-day plan with owners and milestones, and a board-ready reporting cadence — the exact artifacts PE firms look for during post-acquisition reviews.

Building a Cyber Program That Satisfies PE Expectations

Start With Assessment, Not Tools

PE due diligence teams assess current posture before making recommendations. Leadership should do the same. A structured cyber risk assessment — evaluating crown-jewel assets, priority risk areas, governance gaps, and incident response readiness — gives boards a defensible baseline and ensures remediation spend targets the right priorities.

Tyson Martin's cybersecurity program assessments benchmark against NIST CSF 2.0 and ISO 27001, translating technical findings into business-impact language that boards can act on. A focused assessment typically runs 30 to 45 days and delivers a one-page executive summary, a risk register with named owners, and a 90-day remediation roadmap.

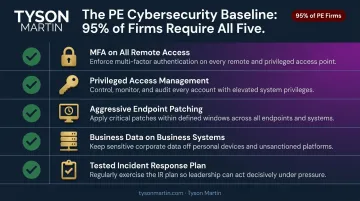

The Foundational Controls PE Firms Evaluate

These are baseline requirements. Roughly 95% of PE firms now mandate all of them:

- MFA on all remote access, including email and cloud platforms

- Privileged access management with documented access review cycles

- Aggressive endpoint patching with measurable SLAs

- Business data on business systems — not personal devices or unmanaged cloud storage

- A tested incident response plan with defined roles, pre-approved communications, and at least one executive tabletop exercise completed

Each of these has a clear owner, a target state, and a way to prove compliance. That's what "inspectable governance" means in practice.

Closing the Leadership Gap

Controls require owners. Many mid-market PE-backed companies lack an executive-level cyber leader who can build the program, communicate risk to the board, and produce the investor-grade reporting PE firms expect. An interim CISO engagement fills that gap without the timeline or cost of a permanent hire.

Tyson Martin's interim CISO engagements run in 90-day phases: by day 30, stabilized basics, risk register, and a 90-day plan; by day 60, governance cadence, vendor risk tiering, and a board-ready narrative; by day 90, tested incident response, long-term roadmap, and security routines the team can run independently.

Monthly retainer engagements typically run $12,000–$35,000 — well below the total cost and organizational risk of a full-time CISO search during an active PE investment cycle.

Frequently Asked Questions

What cybersecurity controls do PE firms typically require from portfolio companies?

The near-universal baseline includes MFA across all remote access, privileged access management, endpoint protection, and data loss prevention. On the governance side, 96% of PE firms require formal incident response plans, data classification policies, and asset management procedures — and 97% require ongoing incident visibility and reporting.

When do PE firms assess the cybersecurity of a target company?

Cyber due diligence now begins before deal close, covering regulatory compliance, third-party risk, employee training, and technical controls. It doesn't stop there — 57% of PE firms conduct post-acquisition reviews quarterly or more frequently throughout the investment lifecycle.

How often are PE-backed companies actually hit by cyberattacks?

According to QBE's 2025 Private Equity Cyber Survey, 54% of PE respondents reported that up to 25% of their portfolio companies experienced a cyber incident in the past year. Among companies that were attacked, ransomware and extortion were the most common incident types.

Does a portfolio company need a full-time CISO to satisfy PE cybersecurity expectations?

Not necessarily. PE firms want inspectable governance — a tested IR plan, a board reporting cadence, and a documented risk register. A fractional or interim CISO can deliver all of this, and is often the practical choice for mid-market companies without the budget or timeline for a permanent hire.

What cybersecurity frameworks should PE-backed companies use?

NIST CSF 2.0 is the most broadly applicable starting point. ISO 27001 matters when customers or counterparties require formal certification; CMMC applies where defense-sector contracts are involved. Selection should be driven by industry, risk profile, and regulatory obligations — not applied uniformly across the portfolio.

How does cybersecurity posture affect valuation in a PE transaction?

Weak cyber posture can compress multiples, trigger deal conditions or price adjustments, and create mandatory post-close remediation commitments that reduce net returns. Deloitte links cyber due diligence findings directly to valuation adjustments and deal terms. Strong posture signals operational maturity and reduces integration risk — material factors in achieving a premium exit multiple.