The governance opportunity is real, but so is the gap. Many PE portfolio company boards remain insular — populated almost entirely by deal team members and management, with no independent voices challenging assumptions or catching blind spots before they become problems.

This post covers what separates high-performing PE boards from average ones, why board composition matters more than most firms acknowledge, why technology governance has become a direct valuation issue, and how governance decisions made during the hold period shape exit outcomes.

Key Takeaways

- PE boards have a structural alignment advantage over public company boards, yet most don't fully use it

- High-performing PE boards share four characteristics: focus, decisiveness, results orientation, and genuine operational engagement

- Independent directors reduce insularity and protect exit value

- 45% of private company directors say improving board-level cybersecurity expertise is very or extremely important

- Cyber risk now affects M&A valuations: buyers use diligence findings to renegotiate price or require pre-close remediation

- Governance quality is increasingly part of buyer diligence; well-documented board processes support faster, higher-value exits

Why PE Boards Are Uniquely Positioned to Drive Value

Public company boards face an inherent tension. They must balance hedge funds seeking short-term returns, pension funds with 20-year horizons, retail investors with varied risk tolerances, and executives whose compensation may not align with any of those groups. The result is often a governance structure optimized for managing conflict rather than creating value.

PE boards don't have that problem. Directors are either proprietors or their direct representatives, with personal capital at risk and a shared investment timeline. Everyone around the table wants the same thing. That alignment shortens decision loops and sharpens accountability.

McKinsey's analysis of PE versus public company boards illustrates how differently this plays out in practice:

| Metric | PE Boards | S&P 500 Boards |

|---|---|---|

| Board size (median) | 7 directors | 10.8 directors |

| Time on strategic initiatives | Higher by 21% | Baseline |

| Self-reported high impact on value creation | 47% | 11% |

| Time spent with management | Higher by 41% | Baseline |

PE directors don't wait for quarterly presentations. They probe at a level of detail that would feel intrusive in a public company setting, and management expects it.

The Governance Gap That Undermines This Advantage

Despite this structural edge, many PE portfolio boards remain insular. Deal team members fill every seat, management is uncontested, and no independent voice exists to challenge the dominant view or speak plainly when performance deteriorates.

The result is a board with all the structural advantages of PE governance but none of the independent challenge that makes oversight effective. Without that friction, poor performance goes uncontested longer than it should — and decisive action arrives too late.

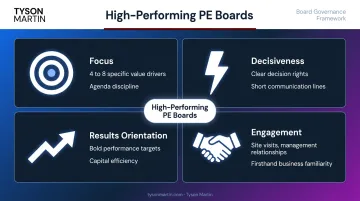

The Four Hallmarks of High-Performing PE Boards

The best PE boards don't look alike in every respect, but they share four consistent characteristics.

Focus

Effective PE boards agree with management on a small number of clear, measurable objectives — typically 4 to 8 specific value drivers — and build every agenda around them. This focus isn't passive. It requires actively declining to engage with peripheral issues that consume meeting time without moving the needle.

A board that spends half its meeting time on compliance updates and committee housekeeping is not focused. A board that spends that time on strategic initiatives, performance variances, and capital allocation decisions is.

Decisiveness

Short communication lines and a proprietorial mindset allow PE boards to act quickly. PE directors receive information more directly, press management on specifics, and make contrarian calls without being paralyzed by the consensus-building that slows public company governance.

This decisiveness is not impulsiveness. It's the product of clear decision rights and a board culture that treats unresolved issues as costs.

Results Orientation

PE boards are unburdened by a company's history. They set performance expectations that may seem aggressive to management, and they hold them. They continuously look for ways to release capital, improve productivity, and accelerate growth — treating each idea as worth evaluating regardless of how it was done before.

That requires a board willing to distinguish between "we've never done it that way" and "it can't be done."

Engagement

PE directors don't limit their involvement to formal board meetings. They visit operations, build relationships across management layers, and develop firsthand familiarity with the business that makes board conversations carry real weight.

Management at PE-backed companies consistently reports a different kind of board engagement than they experienced at public companies. The questions are more specific, the follow-through more persistent. The relationship is direct in a way that changes how management prepares and communicates.

Building the Right Board: Composition and Independent Directors

The Case for Independent Directors

Independent directors are not on the company's payroll or the fund's. That independence has concrete governance value: they can challenge a dominant view, insist on a proper sale process, or push back on a CEO decision when the deal team is reluctant to act.

According to NACD's research, 71% of private company directors say outside board members were added as a source of new ideas — not just oversight. Independent directors bring industry-specific strategic insight, financial discipline, and operational experience that complements the PE firm's deal-making perspective. They protect both governance quality and exit value.

Filling the Technology Expertise Gap

Traditional PE boards have underinvested in technology and cybersecurity expertise at the board level. That gap has become expensive.

NACD data shows 45% of private company directors say improving board-level cybersecurity expertise is very or extremely important, with **49% identifying better committee oversight of cyber risk** as a comparable priority. Yet most portfolio company boards still lack a director or advisor with genuine technology fluency.

This matters because a board without that expertise receives management's cyber and technology reporting without the ability to interrogate it. Directors can't assess whether reported posture matches actual risk, distinguish trends from snapshots, or know whether the metrics they're seeing are the ones that matter.

A board advisor with enterprise security leadership experience — covering large-scale environments like AWS and major retailers, combined with active NACD governance engagement — fills a gap that deal team directors cannot cover. Tyson Martin brings exactly that combination to PE portfolio company boards in data-intensive or regulated industries, where technology governance questions surface across every phase of the hold period, not just at exit.

Practical Composition Criteria

Evaluating board composition requires more than counting seats. Consider these four criteria:

- Review board expertise against portfolio company needs at least annually — not just at the time of investment

- Verify genuine coverage across finance, operations, the relevant industry, and technology/cyber risk

- Build in structured onboarding for new PE board directors: Deloitte recommends site visits and targeted introductions to compress time-to-impact

- Prioritize varied professional backgrounds — homogeneous boards miss assumptions that diverse perspectives surface

Technology and Cyber Governance: The Overlooked Value Driver

Why Cyber Risk Is Now a Valuation Issue

Acquirers — both strategic buyers and secondary PE funds — conduct cyber due diligence as standard practice. According to PwC, cyber diligence can uncover security risks, liabilities, and remediation costs that cause buyers to reconsider a target's value and price — requiring pre-close remediation commitments or renegotiated terms.

With IBM reporting a global average data breach cost of $4.44 million in 2025, the financial materiality of unresolved cyber exposure is no longer a theoretical concern for deal teams. Digital footprint findings routinely surface in diligence to inform negotiation terms, shift valuation, and extract pre-closure remediation commitments from sellers.

Any portfolio company entering an exit process with unresolved technology debt or security vulnerabilities has handed buyers a documented reason to reduce the purchase price.

What the Governance Gap Actually Looks Like

Most PE portfolio company boards lack a director or advisor with genuine technology and security fluency. The practical consequence:

- Management controls what the board sees and how it's framed

- Boards can't distinguish between a well-secured environment and a well-presented one

- Escalation thresholds for technology failures and cyber incidents are undefined or untested

- Exit diligence surfaces surprises that should have been addressed years earlier

What Effective Technology Governance Looks Like

Boards don't need to become technical experts. They need governance infrastructure that makes technology risk visible, comparable, and actionable. That means:

- Plain-English risk reporting — what changed since the last briefing, not just the current state

- Trend-based dashboards — showing movement over time rather than point-in-time snapshots that hide deterioration

- Defined decision rights — explicit clarity on what requires board approval versus management authority

- Tested escalation thresholds — documented before a crisis, not invented during one

Tyson Martin's board advisory methodology is built around exactly this infrastructure: a one-page risk view covering top risks, trends, ownership, and next actions; a board dashboard with trend indicators; and a decision rights map for cyber escalation. The result is independent board visibility that doesn't pull management into constant reporting overhead.

Decision Rights and Escalation Frameworks

Most governance breakdowns don't happen because of bad intent. They happen because nobody defined who owns the decision.

Decision rights in PE board governance means the explicit assignment of which decisions belong to the board versus management, including what thresholds (financial, operational, reputational, or security-related) trigger mandatory escalation. Without that clarity, ambiguity fills the gap, and ambiguity is most dangerous during incidents.

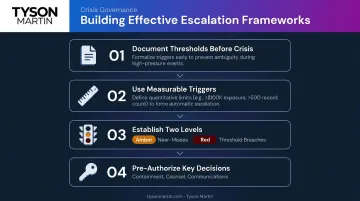

Building Escalation Thresholds That Hold Under Pressure

Effective escalation frameworks share a few structural requirements:

- Document thresholds before a crisis — ones defined during an incident almost always reflect the pressure of the moment rather than clear thinking

- Use measurable triggers — "material impact" is not a threshold; "more than $500K in operational disruption" or "customer data affecting more than 1,000 records" is

- Establish two levels: amber triggers for worsening trends or near-misses, and red triggers for threshold breaches requiring immediate board notification

- Pre-authorize key decisions: who can approve containment actions that disrupt operations, when to engage outside counsel, who speaks publicly, and who owns customer communications

Tyson Martin's workshop approach to escalation frameworks produces two concrete outputs: a one-page risk appetite statement and a one-page escalation ladder. Both can typically be drafted in a single working session, then validated through a tabletop exercise that tests whether the thresholds hold under simulated pressure.

That validation matters. McKinsey research finds 80% of organizations struggle with decision-making — not because the decisions are hard, but because ownership is unclear. Clear decision rights frameworks fix that: management gains autonomy within defined boundaries, and the board maintains visibility without overreaching into day-to-day operations.

How Governance Shapes Exit Value

Exit outcomes are shaped throughout the hold period, not just in the final months before a sale process. By the time buyers are running diligence, the governance record is largely fixed.

According to McKinsey, as of 2025 there were 16,000 buyout-backed companies held for more than four years, representing 52% of total buyout-backed inventory — with average holding periods reaching 6.6 years. Leading firms respond by using dedicated exit committees to review each portfolio company's exit readiness every three months, not just when a transaction is imminent.

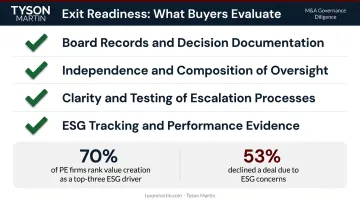

Buyers now evaluate governance quality as part of standard diligence — and ESG has become one of the most scrutinized dimensions:

- Board records and decision documentation

- Independence and composition of oversight

- Clarity and testing of escalation processes

- ESG tracking and actual performance evidence (not just stated policies)

ESG as a Governance Dimension

PwC's Private Equity Responsible Investment Survey found that 70% of PE firms rank value creation as a top-three driver for ESG activity, and 53% chose not to pursue a deal at least once in the prior year because of ESG considerations. Boards that have integrated ESG tracking into their oversight cadence — rather than treating it as a reporting exercise — are better positioned when acquirers probe this area.

The Board's Exit Preparation Role

As the investment nears its planned exit window, the board's agenda should shift toward ensuring governance practices are ready for buyer scrutiny:

- Close documentation gaps in board records and committee processes

- Resolve outstanding compliance issues that could surface in diligence

- Prepare management to narrate the company's governance story clearly

- Address any cyber or technology vulnerabilities before they become negotiating points for buyers

Independent oversight, documented decisions, and tested escalation processes all contribute to a smoother, faster, and higher-value exit. Tyson Martin's M&A cyber due diligence work — which produces a board-ready risk summary, valuation impact assessment, and post-close remediation roadmap — helps PE-backed boards enter that final window with their governance record in order, not scrambling to close gaps under buyer pressure.

Frequently Asked Questions

What is board governance in private equity?

PE board governance is the framework through which PE sponsors, independent directors, and management collaborate to set strategy, monitor performance, manage risk, and create enterprise value. It differs from compliance-oriented governance in its active, results-focused orientation — the board is a working participant in value creation, not a passive oversight body.

How is a PE board different from a public company board?

PE boards represent a more homogeneous shareholder base with aligned financial interests, operate with shorter communication lines to management, set bolder performance targets, and engage more directly in operations. Public company boards must balance competing investor interests and time horizons, which often limits their decisiveness.

Why should PE portfolio companies have independent directors?

Independent directors provide perspectives free from financial dependency on management or the fund. They can challenge assumptions, enforce process discipline, and speak candidly during high-stakes decisions. That independence reduces governance risk and sustains oversight quality through the full hold period.

What role does technology governance play in PE value creation?

Technology and cyber risk directly affects valuation during M&A diligence. Boards that establish clear technology oversight — inspectable reporting, defined escalation paths, and tested incident protocols — give buyers fewer grounds to reduce purchase price or delay closings.

How does board governance affect a PE exit?

Buyers evaluate governance quality as part of diligence, including board records, composition, and decision documentation. Companies with well-documented board processes, independent oversight, and clean governance records achieve stronger valuations and move through exit processes faster with less friction.

What makes a PE board "high-performing"?

High-performing PE boards combine four behaviors — focus, decisiveness, results orientation, and genuine business engagement — with the right expertise mix. That mix includes independent directors who challenge management constructively and, increasingly, advisors with technology and cyber governance fluency to cover what deal team directors typically cannot.