The Equifax breach didn't just expose 147 million consumers. It exposed something equally consequential: that public companies had no coherent framework for deciding when a cyber incident becomes material, who has authority to make that call, or what disclosure obligations follow. The SEC noticed.

This article covers the SEC's investigation of Equifax's cyber risk disclosure failures, the insider trading charges that followed, and what the case means for boards, audit committees, and any organization that holds sensitive data and trades on public markets.

Key Takeaways

- Equifax discovered the breach July 29, 2017, but waited 40 days to disclose publicly — while executives traded stock

- The SEC had already flagged Equifax's cyber disclosure gap in a 2012 comment letter, years before the breach

- Jun Ying, CIO of Equifax's U.S. business unit, sold over $950,000 in shares during the blackout window and pleaded guilty

- Governance — not technology — was the core failure: no materiality threshold, no escalation path

- The SEC's 2023 mandatory rules — 4-day disclosure, annual board oversight reporting — are the direct regulatory legacy of this case

What Happened: The Equifax Breach in Brief

Attackers accessed Equifax's systems from mid-May through July 2017. Equifax discovered the intrusion on July 29, 2017, but didn't tell the public until September 7 — 40 days later.

The breach affected approximately 147 million U.S. consumers, with the House Oversight Committee rounding the final total to 148 million. Data exposed included:

- Social Security numbers, birth dates, and addresses

- Driver's license numbers

- Credit card numbers for approximately 209,000 consumers

- Dispute documents for approximately 182,000 consumers

The Financial Fallout

The market reacted immediately. According to the House Oversight Committee report, Equifax's market capitalization stood at $17.02 billion before disclosure. Its stock fell 35% in the first week, erasing $6 billion in market value.

The legal and regulatory response was equally swift. More than 300 class action lawsuits followed in federal and state courts, along with inquiries from 49 state attorneys general, the FTC, CFPB, SEC, DOJ, and multiple foreign regulators.

The Timing Problem

Among all those regulators, the SEC's interest centered on something more specific than the breach itself. The 40-day gap between discovery and disclosure meant senior executives held material nonpublic information about an event that would clearly move the stock — and some of them traded during that window. That combination of timing, knowledge, and trading activity put the SEC's investigation on a predictable path.

What SEC Cyber Risk Disclosure Rules Actually Require

The legal framework governing Equifax's obligations traces back to the SEC's October 2011 CF Disclosure Guidance: Topic No. 2, which applied existing disclosure obligations to cybersecurity events. It wasn't a new rule: it was an interpretation of existing securities law.

The standard is straightforward. Public companies must disclose cybersecurity risks and incidents when a "reasonable investor would consider the information important to an investment decision."

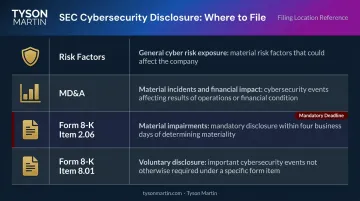

Where Disclosures Belong in SEC Filings

| Filing Location | What Goes There |

|---|---|

| Risk Factors | General cyber risk exposure |

| MD&A | Specific material incidents and financial impact |

| Form 8-K Item 2.06 | Material impairments with mandatory filing deadline |

| Form 8-K Item 8.01 | Voluntary disclosure for events deemed important |

The distinction between Item 8.01 (voluntary, no mandatory deadline) and Item 2.06 (material impairment, deadline-triggered) is central to the SEC's enforcement case against Equifax. Equifax used Item 8.01.

The 2012 Warning Nobody Remembered

Here's the detail most coverage misses: the SEC had already flagged the issue directly with Equifax. In a September 7, 2012 comment letter (File No. 001-06605), SEC staff explicitly asked Equifax to address cyber attack risk disclosure and to include prior attacks for context. Equifax responded that it had not experienced any material breach and would modify its risk factor disclosures starting with its Q3 2012 filing.

Five years later, when the breach hit, regulators had a paper trail showing they had already raised this issue with the company.

The 2018 Guidance and the Insider Trading Extension

That 2012 paper trail established what Equifax knew and when. The 2018 guidance added a second enforcement angle entirely.

The SEC's February 2018 interpretive release (Nos. 33-10459; 34-82746) expanded the framework in one critical direction: it declared that cybersecurity incident information qualifies as material nonpublic information (MNPI), and that insider trading policies must explicitly address cyber events and restrict trading during breach investigations. For any company actively managing a breach at the time of disclosure, that guidance transformed an open question about disclosure timing into a direct insider trading exposure.

Where Equifax's Disclosure Failed the SEC's Standard

The Pre-Breach Gap

Equifax's 2015 Form 10-K contained a generic risk factor: "Security breaches and other disruptions to our information technology infrastructure could interfere with our operations..." The same filing stated Equifax was "not aware of any material breach of our data, properties, networks or systems."

Given the 2012 SEC comment letter, and given that Equifax operated one of the largest consumer data repositories in the country, this boilerplate disclosure created a foundational enforcement problem. The company's public filings failed to communicate the specificity of risk a reasonable investor would need — and the SEC had already put the company on notice that generic language wasn't sufficient.

The 40-Day Window

Equifax learned of the breach on July 29 and disclosed September 7. The SEC scrutinizes both the length of that delay and what happened during it. SEC Chairman Jay Clayton signaled the enforcement posture directly on September 20, 2017, stating publicly that failure to meet disclosure obligations "may result in an enforcement action."

A 40-day window during which executives hold stock and material non-public information exists creates two distinct exposure tracks: a disclosure violation and a potential securities fraud claim.

The Form 8-K Classification Problem

Equifax filed its September 7 breach disclosure under Item 8.01 Other Events rather than Item 2.06 Material Impairments. The distinction matters:

| Filing Item | Mandatory Deadline? | Equifax's Position |

|---|---|---|

| Item 8.01 — Other Events | No | Filed here |

| Item 2.06 — Material Impairments | Yes | Not used |

The SEC's investigation focused on whether that classification was defensible given the scale of the breach, or whether it was used to avoid a triggered deadline. For a breach affecting nearly half the U.S. adult population, the "voluntary disclosure" framing was difficult to sustain.

The Books and Records Exposure

The SEC's 2011 guidance also noted that material breaches may require companies to recognize impaired assets and reduce projected future cash flows in their financial statements. Equifax's delayed accounting for the breach's financial impact created a potential books and records violation — separate from and independent of any disclosure-based theory.

The Jun Ying Insider Trading Case

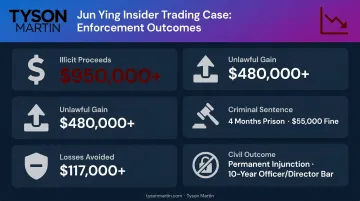

Jun Ying was the Chief Information Officer of Equifax's U.S. Information Solutions business unit. After receiving confidential information about the breach, he exercised all 6,815 of his vested stock options on August 28, 2017 — ten days before public disclosure — and sold the resulting shares.

The numbers from the SEC complaint and DOJ records:

- Proceeds: Over $950,000

- Gain: Over $480,000

- Losses avoided: More than $117,000

- Sentence: 4 months in prison, 1 year supervised release, $55,000 fine, forfeiture of $117,117.61

- Civil outcome: Permanent injunction and 10-year officer/director bar

Parallel criminal charges were filed by the U.S. Attorney's Office for the Northern District of Georgia. Ying pleaded guilty to securities fraud on March 7, 2019.

A second Equifax employee, software engineering manager Sudhakar Reddy Bonthu, faced separate SEC and DOJ charges for alleged ill-gotten gains of $75,167.68 — over a 3,500% return on his trades.

What the Ying Case Added to the Regulatory Picture

The individual charges did something strategically important for the SEC: they demonstrated that cyber incidents, once known internally, create an immediate trading blackout obligation for anyone with access to that information. Missing explicit policies covering cyber-related MNPI is a governance failure — one the SEC is now prepared to treat as such.

Two governance implications follow directly:

- Trading blackout scope: Insider trading policies must explicitly cover cyber-related MNPI, not just financial events

- Board oversight obligation: Directors need documented evidence of active oversight during breach investigations, not just after disclosure

SEC Chairman Clayton called on registrants to "examine their controls and procedures, with not only their securities law disclosure obligations in mind, but also reputational considerations around sales of securities by executives."

Boards that cannot show active oversight of insider trading policies during a breach investigation face a specific risk: SEC enforcement action, director liability exposure, and the reputational damage that follows public charges against executives who traded while the board stayed silent.

What the SEC's Equifax Investigation Signals for Boards and Executive Teams

The Equifax investigation didn't end with individual charges. It built the regulatory architecture boards operate under today.

The SEC's 2023 final rules (Release No. 33-11216), effective September 5, 2023, require:

- Form 8-K Item 1.05: Material incident disclosure within 4 business days of a materiality determination

- Regulation S-K Item 106: Annual Form 10-K disclosures describing the board's oversight of cybersecurity risks and management's role in risk assessment

Boards that treat Equifax as a 2017 story are misreading the timeline — the breach was the catalyst; the 2023 rules are the regulatory consequence.

The Decision Rights Problem Most Boards Haven't Solved

The core failure at Equifax wasn't purely technical. Accountability was diffuse: no single owner held the materiality determination, no threshold triggered board escalation, and no protocol governed communications or trading restrictions during the investigation window.

This pattern, where boards receive fragmented updates after critical decisions are already made, is one Tyson Martin sees repeatedly in organizations that lack a coherent cyber governance framework. It typically manifests as:

- Incident updates reaching the board after containment decisions are already executed

- Risk exceptions approved by email with no expiry date and no documented owner

- No agreed severity threshold for who can declare an incident or authorize shutting systems down

- The first hour of a real incident spent negotiating authority instead of containing damage

Well-governed organizations resolve this with a defined escalation model built around three tiers:

- Management authority: Limited-impact issues handled within existing policy, no escalation required

- Executive approval: Medium-impact issues affecting critical processes, with documented time limits

- Board escalation: High-impact issues capable of causing material outage, regulatory exposure, or brand damage — routed to the CEO and board committee chair, with full board involvement when thresholds are crossed

Boards working with Tyson Martin on disclosure governance and materiality frameworks receive a one-page escalation ladder defining triggers, notification owners, response timelines, and the information required in the first update. That structure satisfies regulators and reduces the chaos that turns a manageable incident into a disclosure failure.

What "Good" Looks Like for Boards Today

Four elements separate boards that can demonstrate defensible oversight from those that cannot:

- A documented cyber materiality threshold in board policy — anchored to dollar impact, downtime, customer harm, and legal exposure

- An incident escalation protocol with defined time windows — who notifies whom, by when, and with what information

- Explicit insider trading restrictions triggered by credible breach indicators — not just standard trading blackouts

- A legal-security coordination process — counsel engaged before any public disclosure decision, not after

Organizations looking to build these four elements before an incident forces the question can work with Tyson Martin through a structured assessment sprint, typically 10 to 15 business days, that delivers a decision-rights map, escalation thresholds, and a board-ready disclosure playbook. The goal is governance that's inspectable and auditable: if the SEC came calling, the board could produce documented evidence of every material decision, who made it, and on what basis.

Frequently Asked Questions

Was my data breached by Equifax?

Visit EquifaxBreachSettlement.com or the FTC's Equifax settlement page to check eligibility. Approximately 147 million U.S. consumers had their data exposed in the 2017 breach, including Social Security numbers, birth dates, and addresses.

When was the last time Equifax had a data breach?

The 2017 breach remains the largest and most consequential. Equifax discovered unauthorized access in mid-May 2017 but didn't disclose publicly until September 7, 2017. No subsequent breach of comparable scale has been confirmed by authoritative sources.

What did the SEC investigate Equifax for?

The SEC investigated whether Equifax failed to adequately disclose known cybersecurity risks before the breach and whether the timing and form of the post-breach disclosure — specifically the use of Form 8-K Item 8.01 rather than Item 2.06 — met securities law standards. The SEC issued a subpoena to Equifax on May 14, 2018 regarding these disclosure issues.

How long did Equifax wait to disclose the breach, and why does it matter legally?

Equifax discovered the breach July 29, 2017 and disclosed publicly September 7 — a 40-day gap. During that window, executives held material nonpublic information and some traded stock. The SEC scrutinizes both the delay and the Item 8.01 classification Equifax used, which carries no mandatory filing deadline and avoided the stricter obligations of Item 2.06.

What are the SEC's current cybersecurity disclosure requirements for public companies?

The SEC's 2023 final rules (Release No. 33-11216) set two core requirements for public companies:

- Incident reporting: Disclose material cybersecurity incidents on Form 8-K Item 1.05 within 4 business days of determining materiality (effective December 18, 2023)

- Annual disclosures: Describe the board's oversight of cybersecurity risks on Form 10-K each year