Introduction

Compliance violations rarely end with just a fine. The more damaging consequences arrive afterward — regulatory scrutiny that consumes executive bandwidth for years, board confidence that erodes quietly, and operational disruptions that cost far more than the original penalty.

Consider Wells Fargo: the Federal Reserve's 2018 enforcement action imposed an asset-growth restriction that remained in place until June 2025, nearly seven years of constrained business operations stemming from governance and compliance failures. The penalty made news. The asset cap reshaped the business.

This guide walks through compliance risk assessment from the ground up — what it is, how to run one, which risk types matter most, and how boards and executive teams should engage with the results. Whether you're building a program from scratch or pressure-testing what's already in place, it covers the full cycle: scoping, scoring, prioritization, and governance reporting.

Key Takeaways

- A compliance risk assessment identifies where your organization faces regulatory exposure, evaluates likelihood and severity, and implements controls to reduce it.

- The process covers five stages: map operations, identify risk contact points, evaluate controls, prioritize gaps, and repeat on a set cadence.

- The four primary risk types — regulatory, financial/operational, reputational, and third-party/supply chain — each require distinct controls and ownership.

- Under DOJ and FFIEC standards, board oversight is an evaluated factor — not just a formality regulators check off.

What Is a Compliance Risk Assessment?

A compliance risk assessment is the documented process of identifying, evaluating, and defining an organization's regulatory risk profile. From there, controls, monitoring, and remediation are tailored to match that profile. Unlike a general IT risk assessment or security audit — which focus on technical vulnerabilities — a compliance risk assessment focuses on where business operations create exposure to regulatory violation.

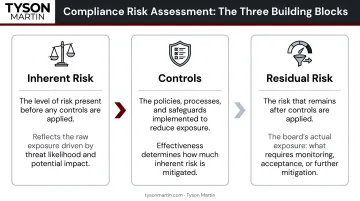

Three Foundational Concepts

Every assessment is built on the same three building blocks:

- Inherent risk — the raw exposure that exists before any controls are applied, based on customers, products, geographies, and transaction types

- Risk management — policies, oversight structures, and technical controls currently in place to reduce that exposure

- Residual risk — what remains after controls are applied. Compare this directly against the board's stated risk appetite

The OCC defines compliance risk as "risk to a bank's condition or resilience arising from violations of laws or regulations or nonconformance with prescribed practices, internal policies, or ethical standards." The framing applies beyond banking — any regulated organization faces the same three vectors: legal violations, policy nonconformance, and ethical failures.

This Is Not a Checkbox Exercise

The DOJ's September 2024 Evaluation of Corporate Compliance Programs asks specifically whether a company's risk assessment is "current and subject to periodic review" and whether that review reflects "continuous access to operational data and information across functions" — not just a point-in-time snapshot. Regulators expect assessments to be living documents, not annual filings.

Industries with the highest compliance stakes:

| Sector | Key Frameworks |

|---|---|

| Financial Services | AML/BSA, SOX, SEC requirements |

| Healthcare | HIPAA Security Rule (45 CFR 164.308), state privacy laws |

| Retail / Technology | GDPR, CCPA/CPRA, PCI DSS |

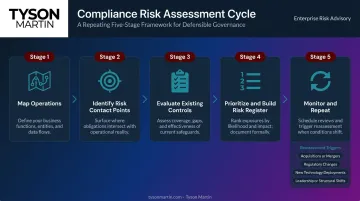

How to Conduct a Compliance Risk Assessment: 5 Key Steps

Step 1: Map Operations and the Regulatory Landscape

Start by documenting key business processes, systems, and transaction flows. Then answer two foundational questions: where does the organization operate, and what rules govern businesses like this one?

Don't rely solely on your compliance team for this step. Business-line owners hold the most detailed process knowledge — they know which systems touch customer data, which vendors handle transactions, and which workflows haven't been updated in years. Cross-functional input is what separates a defensible assessment from a compliance team's best guess.

Step 2: Identify Risk Contact Points

Once operations are mapped, identify the specific places where a regulatory violation could plausibly occur. A compliance risk assessment matrix — scoring each contact point by likelihood (1–5) and impact (1–5) — makes risks comparable across business units and creates an auditable record of your reasoning.

This step answers: where are we most exposed, and how does that exposure compare across the organization?

Step 3: Evaluate Existing Controls

For each identified risk contact point, assess whether current policies, procedures, and technical controls are sufficient to prevent, detect, and correct violations. The critical output here is the gap list — where identified risks outpace existing controls. That gap list becomes the foundation of your remediation plan.

A useful frame: every control should serve at least one of three functions for each risk:

- Prevent — stops the violation from occurring

- Detect — surfaces it quickly if it does occur

- Correct — remediates the damage and closes the gap

If a control only covers one function, document the exposure explicitly.

Step 4: Prioritize and Build a Risk Register

Not every gap can be fixed simultaneously. Rank compliance gaps by risk criticality and remediation effort. Then consolidate findings into a compliance risk register — a centralized document that tracks:

- Each high-priority risk with a named owner

- Remediation timeline and current status

- Residual risk level after planned remediation

- Escalation threshold (when does this reach the board?)

A well-maintained risk register gives executives and auditors a coherent, time-stamped view of where the organization stands and what progress looks like.

Step 5: Monitor, Update, and Repeat

A compliance risk assessment isn't a one-time exercise — your exposure changes whenever the business or regulatory environment shifts. Triggering events that should prompt a reassessment include:

- Acquisitions or divestitures

- Geographic expansion or new product lines

- Leadership transitions

- Material regulatory changes

- A significant audit finding or enforcement action

The DOJ uses "periodic review" rather than a fixed calendar interval. HHS OCR, for HIPAA assessments, expects ongoing updates when "environmental or operational changes" occur. The practical standard: if something material changed in your business or regulatory environment, your assessment is already stale.

The Four Most Common Types of Compliance Risk

Regulatory and Legal Risk

The most direct form. This is the risk of violating specific laws or regulations — GDPR, HIPAA, AML/BSA, SOX, CCPA. Penalty structures are defined; exposure is calculable.

TD Bank's 2024 DOJ resolution required over $1.8 billion in penalties for Bank Secrecy Act and money laundering violations, plus mandatory compliance monitoring and governance remediation. The monetary penalty was significant — the mandatory governance overhaul and multi-year monitorship that followed proved far more operationally disruptive.

Financial and Operational Risk

The downstream consequence of non-compliance — fines, remediation costs, transaction disruption, mandatory audits, and restatements. Financial-crime compliance alone costs U.S. and Canadian financial institutions $61 billion annually, with costs escalating for 99% of institutions in 2024, according to LexisNexis Risk Solutions' True Cost of Financial Crime Compliance study.

Staffing, monitoring, and remediation drive those figures — most of it spent outside any formal enforcement action.

Reputational Risk

Often the most durable damage. Research summarized by the Harvard Law School Forum on Corporate Governance found that regulatory sanctions create market-value losses that can exceed formal penalties — particularly when misconduct harms customers or investors. A public consent order or enforcement action can undermine years of relationship-building with customers, investors, and the regulator itself.

Third-Party and Supply Chain Risk

Organizations are generally held responsible for compliance violations committed by vendors operating under their direction. Two enforcement examples make this concrete:

- CFPB vs. Citibank: Citibank was ordered to provide $700 million in consumer relief for illegal credit-card add-on practices involving service providers.

- HHS OCR vs. North Memorial Health Care: A $1.55 million HIPAA settlement followed failures in business associate agreements and risk analysis.

Vendor due diligence isn't optional — it's a required element of any complete compliance risk assessment.

Compliance Risk Assessment Tools and Methods

Choosing the Right Tool for Your Complexity

| Tool Type | Best For | Trade-Off |

|---|---|---|

| Checklists / Questionnaires | Small teams, single-framework compliance | Limited scalability, no trend tracking |

| Spreadsheets | Mid-size organizations with simple risk profiles | Manual effort, version control issues |

| Compliance Management Software | Organizations with multiple frameworks | Requires configuration; moderate cost |

| GRC Platforms | Enterprises needing audit trails and dashboards | Higher setup investment; strongest auditability |

As regulatory scope expands across jurisdictions and business units, GRC platforms provide the audit trails, automated workflows, and cross-framework trend visibility that spreadsheets cannot replicate.

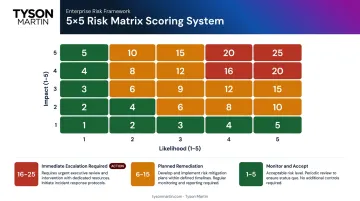

The 5×5 Risk Matrix

The 5×5 methodology scores each compliance risk by plotting likelihood (1–5) against impact (1–5), producing a risk score from 1 to 25. This gives compliance teams and executives a shared, objective language for discussing risk severity — and a defensible record of how prioritization decisions were made.

Use these thresholds to guide prioritization decisions:

- Score 16–25: Immediate remediation required; escalate to executive or board level

- Score 6–15: Remediation planned with defined timelines and owners

- Score 1–5: Accept with documented rationale; monitor on a defined cycle

What Your Outputs Must Include

Regardless of which tool you use, every assessment should produce:

- A risk register with named owners and remediation timelines

- A residual risk summary formatted for board-level review

- A documented remediation plan with measurable milestones — not just a score

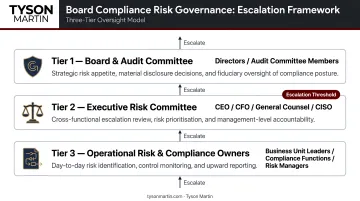

How Boards and Executives Should Engage With Compliance Risk

Board and executive oversight of compliance isn't a governance preference — it's an evaluated factor. Under the FFIEC's Uniform Interagency Consumer Compliance Rating System (UCCRS), "Board and Management Oversight" is a distinct assessment category, covering oversight of the compliance management system, change management, risk identification, and corrective action.

The DOJ's ECCP asks specifically what compliance expertise exists on the board, whether the board has held direct sessions with compliance and control functions, and what information board members have examined in exercising oversight. Passive receipt of annual compliance reports doesn't satisfy that standard.

What Effective Board Reporting Looks Like

Effective compliance reporting gives boards:

- Plain-English residual risk posture — not just a number, but what it means and what changed

- Trend-based metrics — direction matters more than point-in-time scores

- Clear decision points — where does the board need to approve, defer, or decline?

- Escalation status — which risks have crossed defined thresholds?

Ineffective reporting buries boards in control inventories, audit checklists, and technical jargon without connecting findings to business decisions. A board that can't distinguish between a routine compliance gap and a material risk isn't doing oversight — it's receiving paperwork.

Decision Rights and Escalation Thresholds

Three roles, clearly separated:

- Board — sets risk appetite and reviews residual risk against that appetite

- Management — executes within approved boundaries

- Defined triggers — specific events (a new regulation, a failed audit, a third-party breach) automatically escalate to board-level review

Without documented escalation criteria, compliance gaps stay invisible to leadership until they become crises. Pre-approved thresholds tied to business impact prevent the authority negotiations that slow response during actual incidents. Those thresholds should account for:

- Operational downtime and financial exposure

- Data sensitivity and regulatory obligation

When You Don't Have a Chief Compliance Officer

For organizations in transition, navigating M&A, or entering a new regulatory environment without a seasoned compliance executive in place, an interim or fractional CISO fills that role immediately — without the cost or timeline of a permanent hire.

Tyson Martin works with boards and executive teams in regulated industries to build the governance structure, reporting cadence, and escalation framework needed to close gaps quickly. Within 30 days, that typically means a plain-English risk posture assessment and clarified decision rights. By day 90, boards have stable trend reporting, a prioritized remediation roadmap with named owners, and a compliance posture that holds up under audit scrutiny.

Frequently Asked Questions

What is risk assessment in compliance?

Compliance risk assessment identifies which regulations apply to your organization, evaluates where operations create exposure to violations, and determines what controls are needed to close those gaps. Unlike a security assessment, it focuses on regulatory obligations rather than technical vulnerabilities.

What is included in a compliance risk assessment?

Core components include a regulatory inventory, an operations-to-risk mapping, an evaluation of existing controls, a prioritized gap analysis, and a remediation plan with assigned owners and timelines.

What are the four most common types of compliance risk?

Regulatory/legal, financial/operational, reputational, and third-party/supply chain risk. Most assessments address all four — a reputational gap, for example, can trigger regulatory scrutiny, and a third-party lapse can quickly become a financial liability.

What are the main compliance risk assessment tools?

The primary categories are checklists and questionnaires, spreadsheets, compliance management software, GRC platforms, and risk matrices. Tool choice should reflect organizational complexity and the level of auditability required for your regulatory environment.

What is a compliance risk assessment in healthcare?

In healthcare, assessments focus on HIPAA privacy and security requirements under 45 CFR 164.308, patient safety standards, and state regulations. Scope must include both internal processes and third-party vendors who handle protected health information.

What is the 5×5 methodology?

The 5×5 methodology scores risks by multiplying likelihood (1–5) by impact (1–5), producing a score from 1 to 25. This gives teams a consistent, defensible basis for prioritizing where to focus resources first.