The financial exposure is real. The SEC obtained $8.2 billion in financial remedies from 583 enforcement actions in FY2024 alone. Meanwhile, PwC's 2025 Global Compliance Survey found that 85% of organizations say compliance requirements grew more complex over the prior three years—yet only 7% rate themselves as leading in compliance maturity.

The gap isn't effort. It's approach. Most organizations manage compliance reactively: update checklists after rules change, pass audits, repeat. That cycle doesn't prepare you for what's coming next.

This post walks through a five-step scenario planning process built specifically for regulatory risk—written for boards, executive teams, and CISOs who need to make defensible decisions before a crisis forces their hand.

Key Takeaways

- Regulatory fines are board-material events, not compliance team problems

- Checklists prove past adherence; scenario planning prepares you for what changes next

- The five steps are: map exposures, define trigger-based scenarios, build response playbooks, quantify financial impact, and monitor with early warning signals

- Decision rights set in advance are the difference between fast response and chaotic debate

- A fractional CISO or board advisor compresses the timeline for organizations managing overlapping regulatory frameworks

Why Compliance Checklists Alone Won't Protect You

A compliance calendar tells you when to file. Scenario planning tells you what happens to your operations when the SEC updates cybersecurity disclosure rules mid-year, or when the FTC finalizes a breach-notification amendment with a six-month runway.

These aren't hypotheticals. Three major regulatory changes landed within 18 months:

- SEC cyber disclosure rules (July 2023): material incident disclosure required within four business days of a materiality determination

- FTC Safeguards Rule breach-notification amendments: effective May 2024

- NYDFS cybersecurity regulation amendment: November 2023

Organizations tracking these through annual compliance reviews discovered the gap too late to build readiness.

The Framework Overlap Problem

Financial services, healthcare, and retail face a specific challenge: their regulatory frameworks don't operate independently.

- A retailer handling payment data faces PCI DSS, state privacy laws (CCPA, and growing state equivalents), FTC Safeguards requirements, and potentially NYDFS if they operate in New York

- A healthcare organization navigating a proposed HHS OCR cybersecurity rule must simultaneously track HIPAA enforcement trends and state-level privacy actions

- Public companies in any sector now layer SEC cyber disclosure controls on top of existing compliance programs

Thomson Reuters tracked 61,228 regulatory events in 2022 across 1,374 regulators—averaging 234 daily alerts. No compliance checklist keeps pace with that volume.

Board Accountability Has Shifted

Regulators aren't just watching organizations anymore. The FTC's Drizly enforcement order named the CEO directly and imposed future security-program obligations on him personally. Thomson Reuters found 49% of respondents expected compliance officers' personal liability to grow, and 71% said regulatory focus on conduct risk would increase senior manager personal liability.

The board's job has shifted from passive oversight of compliance status to defensible governance over regulatory preparedness. Scenario planning is the mechanism that makes that governance inspectable—before a regulator asks for evidence.

Step 1: Map and Prioritize Your Regulatory Risk Landscape

The first step isn't building a compliance inventory. It's building a living risk map—one that answers not just "what rules apply today" but "what rules are in flux, what agencies are signaling new guidance, and what peer enforcement actions suggest is coming."

What Goes Into the Map

Start with four input categories:

- Current rules and obligations: sector-specific regulations, data privacy laws, financial reporting requirements, cross-border obligations

- Rules in flux: proposed rulemakings, agency Requests for Information, pending amendments (e.g., HHS OCR's proposed HIPAA cybersecurity rule from December 2024)

- Enforcement signals: recent consent orders, civil money penalties, and settlements against peer organizations

- Internal audit findings: gaps that already exist and would be visible to a regulator today

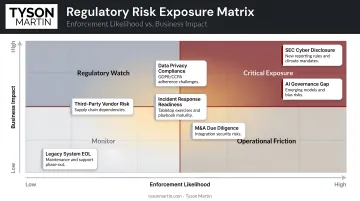

Ranking Exposures

Move from list to ranked map by scoring each exposure on two dimensions:

- Business impact — potential fine size, operational disruption, reputational damage, and customer notification obligations

- Likelihood of enforcement — active rulemaking, recent peer enforcement, agency leadership shifts, legislative attention

The intersection of high impact and high likelihood defines the scenarios worth building. The $1.2M CCPA settlement against Sephora, for example, is a direct enforcement signal for any retailer processing California consumer data. For financial institutions with consumer-facing products, the $3.7B CFPB order against Wells Fargo carries the same weight.

Reliable Intelligence Sources

- SEC Rules and Regulations page and EDGAR filings

- Federal Register entries for SEC, FTC, and CFPB

- CFPB and HHS OCR enforcement action databases

- NRF Retail Law Resource Center and ABA Compliance resources

- Industry body alerts and internal audit outcomes

Treat this as an ongoing intelligence function. Assign explicit ownership — regulatory monitoring without a named owner tends to slip through the cracks.

The Board-Legible Output

The output of Step 1 should be a plain-language summary of where the organization is most exposed and why that exposure is increasing or decreasing. Not a compliance matrix — a risk narrative with business consequences attached.

In organizations managing multiple overlapping frameworks, a fractional CISO or external board advisor can accelerate this mapping by bringing cross-industry regulatory pattern recognition that internal teams typically haven't built up yet.

Step 2: Define Scenarios Around Real Regulatory Triggers

Scenarios built around specific triggering events produce executable decisions. Generic planning produces generic responses — and generic responses don't hold up when regulators are asking questions.

Four Trigger Categories Worth Planning Around

- New legislation or agency rulemaking — the SEC's 2022 proposal and 2023 final cybersecurity disclosure rule is the model; the proposal was public 18 months before enforcement began

- Peer enforcement actions — the SEC's 2024 settlements with Unisys, Avaya, Check Point, and Mimecast for misleading cyber disclosures changed disclosure-control expectations for every public company

- A breach or incident that attracts regulatory scrutiny — the Flagstar $3.55M SEC civil money penalty illustrates how post-incident disclosure handling becomes its own enforcement risk

- Changes in administration or agency leadership that shift enforcement priorities

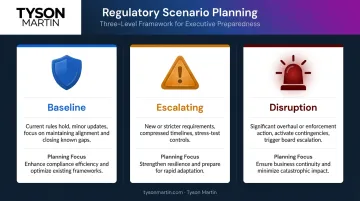

The Three Scenario Types

Every regulatory risk plan should include three scenario levels:

| Scenario | What Changed | Planning Focus |

|---|---|---|

| Baseline | Current rules hold, minor updates | Maintain alignment, close known gaps |

| Escalating | New or stricter requirements, compressed timelines | Stress-test controls and documentation |

| Disruption | Significant overhaul or enforcement action against your organization | Activate contingencies, trigger board escalation |

Each scenario narrative should answer four questions: What changed? What is the regulatory body requiring? What does the timeline look like? What will the organization be expected to demonstrate?

Setting Decision Rights in Advance

The most common failure point when scenarios actually materialize is not a missing control — it's the absence of clear decision authority. When no one can say yes, no, or not yet without a meeting, the organization burns hours on internal debate at exactly the moment speed matters most.

For each scenario, define in advance:

- What threshold triggers board-level review versus management-level response

- Who can approve disclosure decisions, system shutdowns, or external counsel engagement

- Which decisions require the audit committee chair versus the full board

Organizations that define these thresholds before a trigger event arrives reach decisions faster and with less institutional friction — which is precisely what regulators and boards expect to see.

Step 3: Build Response Playbooks Tied to Each Scenario

A scenario without a playbook is just a story. The playbook converts each narrative into concrete actions with owners, timelines, and success criteria.

Basic Playbook Structure

Each playbook should address four time horizons:

- Trigger conditions — the specific signals that activate this playbook

- Immediate actions (0–30 days) — containment, documentation, initial regulatory communication

- Short-term adjustments (1–3 months) — control updates, process changes, evidence preparation

- Structural changes (3+ months) — technology, staffing, and governance overhauls

What Regulatory Playbooks Must Cover

Beyond general incident response, regulatory playbooks need to address:

- Documentation readiness: What would you need to show a regulator today? Is that evidence gathered, organized, and current?

- Communication protocols: Who notifies the board? Who contacts regulators, and by when? Who owns customer notifications?

- Resource pre-positioning: Is outside counsel already engaged? Are forensics vendors pre-contracted?

- Disclosure timing: For public companies, the four-business-day SEC material incident clock starts at materiality determination—does your team know exactly when and how that determination gets made?

Testing Before You Need It

Documented procedures only hold up if they've been tested. NIST SP 800-61r3 requires periodic testing of incident response procedures — and PwC's crisis resilience research shows why it matters: 64% of integrated resilience programs had optimized testing capabilities, versus only 38% of non-integrated programs.

Run tabletop exercises with legal, compliance, IT/security, operations, and an audit committee representative present. The gaps that consistently surface:

- Shutdown authority confusion (who can actually authorize containment actions?)

- Outdated contact lists and unvetted external vendors

- Communication breakdowns between legal, security, and executive teams

- Untested notification triggers and unclear ownership

After each exercise, the CISO or risk leader should produce a single-page summary covering three things: where the organization stands against each scenario, what changed since the last review, and what decisions require board input. If you can't produce that page, the playbook isn't ready.

Step 4: Measure the Impact of Each Scenario Before It Arrives

Impact measurement gives boards and executive teams what they need to make investment decisions before urgency removes all the options.

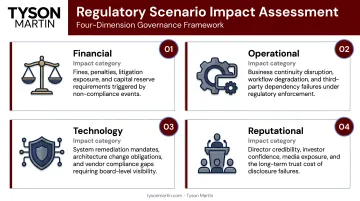

Cross-Functional Impact Assessment

For each scenario, assess four dimensions:

- Financial exposure: estimated fines, remediation costs, legal spend, notification costs. Use directional ranges, not false precision. A $3.7B CFPB order and a $3.55M SEC penalty both represent real data points for sizing exposure in their respective contexts.

- Operational disruption: workflow changes, staffing requirements, system certifications, business process interruptions

- Technology implications: security control gaps, data governance changes, system upgrades required to demonstrate compliance

- Reputational risk: customer notification requirements, regulatory disclosure timelines, public enforcement actions

Connecting Measurement to Investment Decisions

When regulatory risk looks like a business risk—expressed in revenue loss, downtime, legal cost, and trust erosion—boards can compare it, rank it, and allocate resources against it. PwC found that compliance technology investments produced better risk visibility for 64% of organizations, and faster identification of compliance issues for 53%.

The framing that works with boards: show the cost of the scenario versus the cost of the control. An investment in documentation infrastructure or a pre-contracted outside counsel relationship looks different when the alternative is a four-business-day disclosure window with no playbook in place.

Step 5: Build a Living Plan with Early Warning Signals

A scenario plan that isn't actively monitored becomes stale within months. The final step is building a monitoring system that catches regulatory movement before it becomes a compliance crisis.

Signposts Worth Watching

Early warning signals that a scenario is beginning to materialize:

- A regulatory agency issues a Request for Information targeting your sector

- A peer organization receives a consent order or civil money penalty

- A congressional hearing focuses on your industry's practices

- A state-level enforcement sweep precedes federal rulemaking (California's CCPA Sephora settlement preceded broader CPPA enforcement activity)

- Agency leadership changes shift stated enforcement priorities

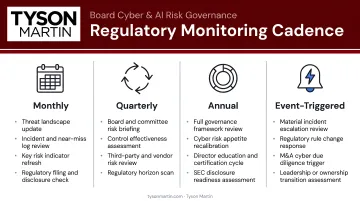

A Sustainable Monitoring Cadence

- Monthly: review legislative and enforcement activity; check Federal Register entries for relevant agencies

- Quarterly: reassess scenario likelihood and response readiness; update board risk reporting with trend indicators

- Annually: full plan refresh with updated scenarios, revised impact estimates, and retested playbooks

- Event-triggered: major peer enforcement actions, new agency guidance, or significant operational changes to your own environment

Assign explicit ownership for each monitoring function — diffuse accountability is the most common reason signal-based systems quietly stop working. The NACD's 2026 cyber-risk reporting guidance reinforces this cadence, recommending structured board cyber-risk reports at least quarterly with ad hoc updates for significant changes.

What Board Reporting Should Show

The monitoring output should feed directly into the board's regular risk reporting cycle. Effective reporting shows:

- Trend over time: is regulatory exposure increasing or decreasing?

- Which scenarios have moved in likelihood since the last review

- What actions are in progress, with owners and due dates

- What decisions require board input now

Boards that do this well stop asking "are we compliant?" and start asking "what's moving, who owns it, and what do we decide today?" That shift — from compliance checkbox to active risk posture — is the difference between a plan that sits in a drawer and one that drives governance decisions in real time.

Frequently Asked Questions

How can scenario planning be used to mitigate regulatory risk?

Scenario planning mitigates regulatory risk by helping organizations identify likely shifts before they occur, pre-build response playbooks, and establish clear decision rights. When a rule changes or an enforcement action emerges, the organization can act quickly and demonstrate preparedness rather than building a response from scratch.

What are the steps of the scenario planning process?

The five steps are: map and prioritize regulatory exposures, define scenarios around specific triggering events, build response playbooks for each scenario, measure cross-functional impact before a scenario arrives, and maintain a living monitoring plan with early warning signals that feed into regular board reporting.

How is regulatory scenario planning different from a standard compliance audit?

A compliance audit assesses adherence to current rules at a point in time. Regulatory scenario planning anticipates how rules might change and prepares the organization to respond before those changes occur—a proactive governance discipline, not a retrospective one.

How often should regulatory risk scenarios be updated?

Plan for monthly monitoring, quarterly reassessment of scenario likelihood and response readiness, and a full annual refresh. Out-of-cycle updates are warranted by major enforcement actions, new legislation, or significant operational or technology changes.

Who should be involved in regulatory scenario planning?

Cross-functional participation is required: legal, compliance, IT/security, operations, and finance. Board or audit committee engagement is essential to set decision rights and ensure the plan is integrated into governance rather than siloed in a single function.