Introduction

Regulated organizations generate more compliance reports than ever before. Yet when a risk event hits, boards still say they didn't see it coming.

The problem isn't a shortage of data. It's the gap between what gets filed with regulators and what actually reaches leadership in a form they can act on. Most organizations invest heavily in the filing obligation — quarterly filings, structured submissions, annual audits — and underinvest in the governance layer that translates that data into board-level insight.

A 2023 Gartner survey found that fewer than 40% of board members feel they receive actionable risk information from management. The reports exist. The decisions don't follow.

This guide defines regulatory risk reporting clearly, explains what it must include, identifies the most common failure points, and shows how organizations can build a framework that supports defensible decisions at the board level.

Key Takeaways

- Regulatory risk reporting serves two audiences: external regulators who require structured filings, and boards who need plain-English risk posture summaries.

- Financial services, healthcare, and retail each juggle overlapping obligations from multiple authorities — often with conflicting deadlines and incompatible data formats.

- Strong reports answer three questions: what changed, what the exposure means for the business, and what decision is required.

- Common failure modes include data silos, stale reporting, and metrics that measure activity instead of risk trend.

- Pre-defining escalation thresholds and decision rights is what separates reports that prompt action from reports that prompt follow-up meetings.

What Is Regulatory Risk Reporting — And Why It Matters to the Board

Regulatory risk reporting is the systematic process of collecting, analyzing, and submitting data to regulatory authorities to demonstrate compliance. That's the external obligation.

There's a second function most organizations underinvest in: the internal governance layer that translates that same data into strategic insight for boards. Treating the filing as the finish line is where most reporting programs break down.

Regulatory Risk vs. Compliance Risk

These terms get used interchangeably, but they describe different problems:

- Regulatory risk — the possibility that changes to laws, regulations, or enforcement priorities will adversely affect operations, finances, or strategy

- Compliance risk — the internal failure to meet requirements that already exist

Boards need visibility into both. An organization can be fully compliant today and still face significant regulatory risk if proposed rule changes would require costly operational restructuring.

The Stakes Are Real

The consequences of weak regulatory risk reporting aren't abstract. In FY2024, the SEC filed 583 enforcement actions and ordered $8.2 billion in financial remedies, including $2.1 billion in civil penalties alone. That number reflects the enforcement environment boards are operating in.

Why This Is a Board-Level Responsibility

Regulators have moved beyond expecting boards to simply delegate oversight. Two rules define the current expectation clearly:

- SEC Cybersecurity Rule (July 2023) — public companies must describe how their boards oversee cybersecurity risks and how they are kept informed, not just that a CISO exists

- FDIC examination guidance — holds boards accountable for sound policies, effective supervision, and systems to monitor legal compliance

When that reporting infrastructure is missing or fragmented, boards can't demonstrate the oversight regulators expect — and can't exercise it in practice either.

Types of Regulatory Reports Organizations Must Know

Categories of Required Reports

The specific mix varies by industry and jurisdiction, but most regulated organizations must manage some combination of the following:

| Report Type | Purpose | Example |

|---|---|---|

| Financial statements | Investor visibility | Balance sheets, income statements, cash flow |

| Risk exposure reports | Demonstrate risk posture | Credit, market, operational risk metrics |

| Transaction reports | Activity monitoring | Trade details, payment records |

| Compliance reports | Demonstrate rule adherence | Environmental, safety, cybersecurity controls |

| Capital adequacy reports | Demonstrate solvency | Regulatory capital calculations |

| Incident disclosures | Event-driven notifications | Breach reports, material cybersecurity incidents |

Reporting Frequency and Deadlines

Frequency varies by obligation — and missed deadlines carry penalties in most frameworks:

- Quarterly — FR Y-9C filings, Call Reports, SEC periodic filings

- Monthly — liquidity reports, certain AML monitoring outputs

- Annual — audits, compliance attestations, annual HIPAA breach reports for smaller incidents

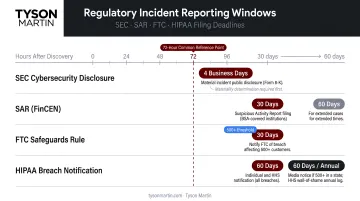

- Event-driven — SEC Form 8-K material cybersecurity incidents (generally within four business days of determining materiality), HIPAA breach notifications (within 60 days for breaches affecting 500 or more individuals), SAR filings (within 30 calendar days)

Regulatory Reporting vs. Financial Reporting

These are related but distinct. Financial reporting (balance sheets, income statements, cash flow statements) is prepared for investors and follows accounting standards set by FASB. Regulatory reporting is filed with authorities to demonstrate rule compliance, in formats those authorities prescribe. Both often draw from the same underlying data, but conflating them — submitting investor-facing financials in place of regulator-prescribed formats, or vice versa — is a common source of compliance gaps.

What Should a Regulatory Risk Report Include?

Core Elements of an Effective Report

Whether submitted to a regulator or presented to the board, a useful regulatory risk report shares the same structural logic:

- Current risk posture summary — where things stand now

- Prior period comparison — what changed and why

- Risk drivers — what's causing the movement

- Decision or escalation item — what action is required

Reports without a clear "so what" aren't serving governance. They're producing documentation.

For Formal Regulatory Submissions

Regulators require structured data in prescribed formats. The specific data components depend on the framework, but typically include:

- Entity financial data and capital calculations

- Risk exposure metrics (credit, market, operational)

- Transaction-level detail where required

- Customer information for AML/KYC compliance

- Source documentation and data lineage records

Unverified or inconsistently defined data creates more regulatory exposure than it resolves. Traceability isn't a formality — it's what regulators pull when a submission gets scrutinized.

For the Board

Board-facing reports operate differently. Directors don't need every metric — they need the right signals. A board-ready regulatory risk summary should include:

- Current posture in plain English, including whether it's improved or deteriorated since last quarter

- Trend lines across at least three periods — a single data point doesn't show direction

- The two or three risks that materially changed, not an exhaustive inventory

- A specific decision or escalation item — what the board is being asked to do, and by when

In practice, this fits on one page or two slides: a dashboard against approved thresholds, a short narrative on what shifted since the last briefing, and a decision section that names the options, the recommended path, and who owns execution.

What a Compliance Report Must Also Document

Strong compliance reports go beyond metrics. They document:

- Controls currently in place and their coverage

- Gaps identified during the period

- Remediation actions underway, with named owners and deadlines

- Prior period commitments — what was promised, what was delivered

This creates an auditable record of governance accountability. That record is what protects the organization — and the board — when regulators or auditors ask what was known and when.

Common Regulatory Reporting Requirements by Industry

Financial Services

Banks and financial institutions face some of the most demanding and overlapping reporting obligations in any regulated sector:

- Call Reports — quarterly filings to the FDIC via the FFIEC Central Data Repository

- FR Y-9C — quarterly consolidated financial statements for holding companies with $3 billion or more in assets, used by the Federal Reserve as a primary monitoring tool between on-site examinations

- SARs — Suspicious Activity Reports filed through FinCEN's BSA E-Filing within 30 calendar days of identifying a reportable transaction

- CTRs — Currency Transaction Reports required for cash transactions over $10,000

- SEC Form 8-K Item 1.05 — cybersecurity incident disclosures generally due within four business days of determining materiality

The SEC's 2023 cybersecurity disclosure rule added further obligations. Beyond incident reporting, Item 106 of Regulation S-K requires public companies to describe board oversight processes specifically — not just assert that oversight exists.

Healthcare and Retail

HIPAA-regulated entities must report breaches affecting 500 or more individuals to HHS within 60 days of discovery. Smaller breaches are reported annually. As of late 2024, HHS's Office for Civil Rights had received over 374,000 HIPAA complaints and collected nearly $145 million in settlements and civil penalties.

Retailers face a different but equally layered picture:

- PCI DSS — compliance attestations via SAQs and ROCs

- FTC Safeguards Rule — notifications for events affecting 500 or more consumers, due within 30 days

- CCPA — disclosure obligations for California residents

Cross-sector organizations — a retailer with a financial product, a healthcare system that processes payments — often face requirements from multiple regulators simultaneously, each with distinct formats, deadlines, and data definitions.

The Landscape Keeps Shifting

According to Thomson Reuters' 2023 Cost of Compliance report, 70% of firms expected compliance costs to increase over the next 12 months, with 68% anticipating budget increases and 69% expecting headcount growth. Organizations must treat regulatory monitoring as an ongoing function, not a periodic project.

Top Challenges in Regulatory Risk Reporting

Data Quality and Fragmentation

Most organizations pull reporting data from multiple systems that don't connect. The result: inconsistencies, reconciliation delays, and errors that create compliance exposure rather than reducing it. The Basel Committee's 2023 progress report on BCBS 239 found that only 10 of 30 global systemically important banks were fully compliant with risk data aggregation principles — nearly a decade after those principles were published. The root cause is almost always the absence of a single source of truth for risk data.

When data quality is uncertain, transparency matters. Labeling data confidence levels explicitly — and disclosing when a metric definition changes — is a governance practice that builds credibility with both regulators and boards.

Reporting Lag and Stale Risk Signals

When a board report reflects conditions from 60 or 90 days ago, decisions are being made on outdated information. Specific obligations already impose tight timelines:

- 4 business days for SEC material cyber incident disclosures

- 30 days for SAR filings

- 30 days for FTC Safeguards notifications

Organizations relying on manual processes cannot meet these cadences reliably. When they miss them, the reporting failure itself becomes the enforcement issue.

A three-month trend is more informative than any single snapshot. Building reporting cadences that produce consistent data on a predictable schedule reduces lag and improves the signals boards receive.

Overlapping Requirements and Compliance Burden

Organizations operating across industries, geographies, or with extensive third-party vendor relationships may face dozens of distinct reporting obligations — each with different formats, deadlines, and data definitions. Without a structured regulatory inventory, compliance teams spend more time firefighting than filing. That reactive posture doesn't just create inefficiency — it increases the risk of missing an obligation entirely, which is often where enforcement begins.

Building a Regulatory Risk Reporting Framework That Boards Can Actually Use

Start with a Regulatory Inventory

The foundation is mapping all applicable reporting obligations to the organization's specific profile — industry, geography, size, and business model. This produces a regulatory inventory that drives reporting design rather than an ad hoc response to requirements as they surface.

Without this map, organizations discover obligations after they've already missed a filing deadline.

Establish Data Governance Before Designing Reports

Reporting is only as reliable as the data behind it. Before designing dashboards or board presentations, organizations need to:

- Define who owns each data element

- Set quality and validation standards

- Establish access controls and data lineage documentation

- Create a single source of truth that feeds both regulatory filings and board-facing outputs

When a metric changes definition, it must be disclosed — especially in regulated contexts like SEC 10-K filings. Consistency between regulatory submissions and board reporting is a governance requirement, not a best-effort aspiration.

Design for Two Audiences at Once

Build the underlying data infrastructure to support regulatory submission formats. Then create a board-facing translation layer — a stable dashboard that shows trend over time, highlights what changed since the last briefing, and flags items requiring a decision.

The goal is fewer surprises and faster escalation, not more data. A board report that fits in two slides and ends with a named decision is more useful than a 40-page deck that documents everything without clarifying anything.

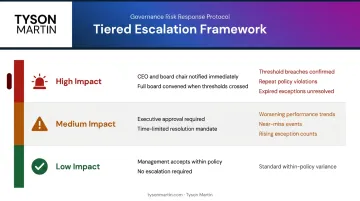

Define Decision Rights and Escalation Thresholds

A reporting framework is only useful if it defines what triggers escalation, who makes which decisions, and what the response protocol is when a threshold is breached. These parameters need to be pre-agreed — not improvised during an incident.

A practical tiered model looks like this:

- Low-impact issues — management accepts within policy, no escalation required

- Medium-impact issues — executive approval required, with time limits on resolution

- High-impact situations — CEO and board committee chair notified immediately; full board when thresholds are crossed

Amber triggers (worsening trends for two consecutive reporting cycles, near-misses, rising exception counts) and red triggers (threshold breaches, repeat violations, expired exceptions without closure) give boards a consistent framework for reading reports rather than debating every data point.

Getting There Faster

For organizations in transition — new leadership, post-incident recovery, M&A integration, or active regulatory scrutiny — standing up a credible reporting framework quickly is especially critical.

Tyson Martin works with boards and executive teams to establish inspectable reporting structures, clear decision rights, and escalation thresholds that hold under real pressure. His 90-day engagement model is structured in three phases:

- Stabilization — surface the truth and clarify ownership

- Alignment — translate findings into board-ready decisions

- Operationalization — build a reporting rhythm that outlasts the engagement

For organizations that need to move fast, that compressed timeline matters.

Frequently Asked Questions

What is regulatory risk reporting?

Regulatory risk reporting is the systematic process of submitting structured compliance data to regulatory authorities — and, internally, communicating risk posture to boards in a form that supports oversight and decision-making. Most organizations focus on the filing obligation and underinvest in the governance layer.

Who needs to do regulatory reporting?

Any organization subject to federal or state oversight — financial services, healthcare, retail, energy, government contractors — has formal reporting obligations. The scope depends on size, sector, and business activities, with agencies including the SEC, FDIC, FTC, and HHS setting specific requirements.

What should a compliance report include?

A strong compliance report covers:

- Current risk posture and comparison to the prior period

- Identified risk drivers and controls in place

- Remediation actions with named owners and deadlines

- A clear statement of what decision or escalation is required

What are examples of regulatory reporting?

Common examples include:

- Bank Call Reports filed with the FDIC

- SEC Form 8-K cybersecurity incident disclosures

- FinCEN Suspicious Activity Reports

- HIPAA breach notifications to HHS

- PCI DSS compliance attestations (SAQs or ROCs)

What is regulatory exposure?

Regulatory exposure refers to the degree to which an organization is vulnerable to adverse consequences — fines, sanctions, reputational harm, or operational restrictions — from changes in regulations or from gaps in its current compliance posture.

What is an example of regulatory risk?

A financial institution that hasn't updated its AML monitoring systems to meet revised BSA requirements faces regulatory risk. If the gap surfaces during an examination, regulators may fine the institution, restrict its activities, or require costly remediation — regardless of whether any suspicious activity occurred.