This isn't a knowledge problem. It's a structural one. GRC gets treated as a compliance label rather than a decision-making discipline, which means the framework exists on paper but doesn't hold when regulators show up or something goes wrong.

This article is written for board members, audit and risk committee members, CEOs, COOs, and risk leaders in regulated financial institutions. It explains what GRC is, why it's structurally required in financial services, how the three pillars function together, and where the framework most commonly breaks down at the leadership level.

Key Takeaways

- GRC — Governance, Risk, and Compliance — aligns how a financial institution is directed, what threats it tracks, and what rules it must follow

- Regulators require it, enforcement actions reinforce it, and post-incident scrutiny makes gaps impossible to hide

- The three pillars only work when connected — siloed functions without governance accountability create exposure

- The most common failure is treating GRC as a compliance exercise rather than a decision-making discipline

- Boards need clear oversight structures and honest reporting, not just annual risk briefings

What Is GRC in Financial Services?

GRC — Governance, Risk, and Compliance — is an integrated organizational approach that aligns how a financial institution is led, how it identifies and responds to threats, and how it meets its regulatory obligations, so these three functions reinforce rather than contradict each other. Done well, GRC produces fewer regulatory surprises, clearer accountability when something goes wrong, and a leadership team that makes decisions based on risk posture — not reaction.

Where most institutions go wrong is conflating GRC with standalone compliance. The distinction matters:

- Compliance tracks whether rules are being followed

- Risk quantifies exposure that persists even when rules are followed

- Governance establishes who owns which decisions and how leadership is held accountable for outcomes

That last point — accountability for outcomes — is what separates functional GRC from documentation that satisfies examiners without changing behavior on the floor.

Why Financial Services Organizations Cannot Afford to Operate Without GRC

The Regulatory Density Problem

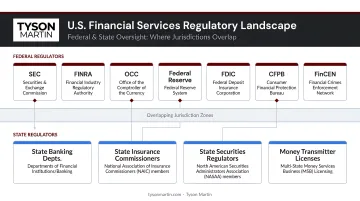

Financial services operates under one of the most complex regulatory environments of any industry. The GAO has described the U.S. financial regulatory structure as "complex," "fragmented," and characterized by overlapping authorities. That structure spans:

- Federal prudential regulators: OCC, Federal Reserve, FDIC, NCUA

- Consumer oversight bodies: CFPB, FTC

- Securities and derivatives regulators: SEC, CFTC

- Housing finance and systemic risk oversight

- 56 state insurance regulators across states and territories

A financial institution's examination obligations compound this. Per GAO reporting, FDIC, the Federal Reserve, and OCC must conduct full-scope, on-site examinations at least every 12 months, with an 18-month interval available only for qualifying smaller institutions. Examination readiness isn't a periodic project — it's a standing operating requirement.

Institutions without a functioning GRC framework manage each of these relationships in isolation — no unified view of obligations, no visibility into overlaps, no way to spot gaps before examiners do.

What Happens When GRC Is Siloed

The 2008 financial crisis is the most documented example of what fragmented governance and risk management produce. The Financial Crisis Inquiry Commission concluded that "dramatic failures of corporate governance and risk management at many systemically important financial institutions were a key cause" of the crisis. The Basel Committee's post-crisis analysis added that banks "lacked the ability to aggregate risk exposures and identify concentrations quickly and accurately at the bank group level, across business lines and between legal entities."

Three disconnected narratives reached leadership simultaneously:

- Governance activity — board decisions made without full risk context

- Risk assessments — exposure data that never aggregated across business lines

- Compliance status — obligations tracked in silos, not as an integrated picture

That fragmentation drove decisions that no individual failure could fully explain.

The Cyber and Technology Dimension

The financial sector's digital exposure has made GRC complexity worse. IBM's 2024 data breach analysis found that financial-industry breaches averaged $6.08 million — 22% higher than the global average — with massive breaches involving 50 million or more records averaging $375 million.

These aren't IT metrics. They're board-level operational and compliance risk figures.

Board Accountability Is Personal

Director exposure is explicit across the major prudential frameworks:

- Federal Reserve SR 21-3 — boards must oversee strategy and risk appetite, and hold management accountable for effective risk management and internal controls

- OCC Director's Book — directors can face civil money penalties for breach of fiduciary duty

- FDIC guidance — institution-affiliated parties, including directors, may face penalties for violations, unsafe practices, or fiduciary failures

Board members who lack the information structures and decision rights to act on these obligations cannot discharge them defensibly. Receiving an annual risk briefing is not the same as exercising oversight.

The Three Pillars of GRC in Financial Services

The three pillars are interdependent, not parallel. Governance sets direction. Risk identifies what could disrupt that direction. Compliance confirms the institution is operating within the boundaries regulators have established. When one pillar weakens, the others cannot compensate.

Governance: How the Institution Is Directed and Held Accountable

Governance in financial services goes beyond board structure. It is the system of decision rights, reporting obligations, and accountability mechanisms that determine who authorizes what, who is informed when, and who is answerable when outcomes fall short.

A functional governance layer means the board can direct management and inspect results — not merely receive status updates.

Weak governance looks like:

- Risk decisions with unclear ownership

- Reporting that shows activity rather than posture

- Leadership teams that react to regulatory findings rather than anticipate them

- Risk exceptions approved by email with no expiry date

- Audit findings that repeat because deadlines aren't enforced

The fastest diagnostic: ask who owns your top three risks, by name and role. If that question produces debate rather than a 30-second answer with documentation, the governance layer isn't functional.

Risk Management: Identifying and Prioritizing What Could Go Wrong

Risk management in financial services extends well beyond credit and market risk. The OCC's Corporate and Risk Governance Handbook identifies eight distinct risk categories: credit, interest rate, liquidity, price, operational, compliance, strategic, and reputation. Modern institutions treat cyber and technology risk as a governance matter — owned at the executive and board level, not delegated to IT.

The CISO and CRO now share direct oversight responsibility. FFIEC cybersecurity guidance requires that enterprise-wide risk management incorporate cyber threat information and report vulnerabilities directly to the board and senior management.

An effective risk management process produces three outputs for leadership:

- Which risks are acceptable given current business objectives and risk appetite

- Which risks require mitigation and at what priority

- Which risks require escalation and who makes that call

Identifying risks without ranking them against business objectives produces long lists, not decisions.

Compliance: Meeting Regulatory Obligations Without Losing Business Speed

Compliance in financial services covers a broad set of external obligations:

- BSA/AML — recordkeeping, currency transaction reporting above $10,000, suspicious activity reporting

- SOX Section 404 — management reports on internal control over financial reporting for public institutions

- GLBA — policies and controls to prevent unauthorized disclosure of customer financial information

- FFIEC guidelines — examination guidance across BSA/AML, information security, and cybersecurity

- State banking law — varying by charter and service area

Compliance programs must track regulatory change continuously — not just at audit time. Institutions that treat compliance as a standalone function consistently spend more, move slower, and still face regulatory findings. The reason is consistent: compliance activity isn't connected to how the institution actually makes decisions.

How GRC Functions at the Board and Executive Level

GRC is not an IT or compliance department function. It's a leadership operating model.

The board's role:

- Set risk appetite

- Approve the governance framework

- Receive reporting that is honest about where exposures exist and what management is doing about them

Management's role:

- Execute within those parameters

- Escalate when conditions change

What Effective Board-Level GRC Reporting Looks Like

Most board risk reporting is built for audit readiness, not decision-making. Effective reporting looks different:

- Plain-language risk posture : skip control counts or compliance percentages

- Trend direction over time, not one-time snapshots

- Clear metrics that distinguish meaningful change from noise

- Explicit identification of decisions the board must make versus items that are informational only

One practical structure: a one-page packet covering the five metrics that matter (with trends and thresholds), top risks and what changed, incidents and near-misses, program delivery tied to risk reduction, and decisions needed from the board. If management needs 40 slides, the story isn't ready.

Clear reporting only works when the organization has also defined who acts on it. That's the function of escalation thresholds.

Escalation Thresholds and Decision Rights

A GRC framework that doesn't define when risk decisions move from management to the board will default to informal judgment during incidents — and that's where institutions run into regulatory and legal trouble.

Escalation thresholds should answer five questions without debate:

- Who accepts risk, and at what dollar or impact threshold?

- Who approves security exceptions, and for how long?

- Who decides budget tradeoffs when security competes with delivery?

- Who declares incident severity and can authorize system shutdowns?

- Who owns vendor go/no-go decisions for critical suppliers?

Tyson Martin's advisory work focuses on building these decision-rights frameworks: mapping escalation triggers to business impact rather than technical severity, and establishing them before an incident forces the question. Institutions that define these parameters in advance arrive at incidents with clear authority — not competing interpretations of who decides what.

Implementation Sequence Matters

Organizations in transition (new leadership, post-incident, M&A, modernization) often build compliance infrastructure before establishing governance accountability. When that happens, controls exist on paper with no one responsible for outcomes.

The right sequence:

- Governance structures first — accountability before everything else

- Risk frameworks second — scope and appetite defined before controls

- Compliance programs layered in once ownership is clear

Common GRC Failures in Financial Services

The Checkbox Compliance Trap

Institutions that build GRC programs around audit readiness rather than risk reduction end up with documentation that satisfies examiners but doesn't change behavior. The OCC's enforcement policy is explicit: an institution "must not be deemed in compliance simply because the board and management have made progress" — validation requires confirming the "effectiveness and sustainability" of corrective actions.

Regulators have become sophisticated at identifying compliance theater. Policies look complete, controls look mapped, exceptions get politely documented — meanwhile, real paths to material loss stay open.

Data Fragmentation as a Structural Failure

When governance, risk, and compliance data live in separate systems with separate owners and no common reporting layer, leadership cannot see the institution's actual risk posture. They see three separate stories that may contradict each other — and that gap is exactly where enforcement actions originate.

The Citibank enforcement actions illustrate the cost. In 2024, the OCC assessed a $75 million civil money penalty against Citibank for insufficient progress on enterprise-wide risk management and data governance, including lack of processes to monitor how data-quality concerns affected regulatory reporting. The Federal Reserve separately assessed $60.6 million against Citigroup for violating its 2020 enforcement action on risk management and internal controls.

The Basel Committee's post-crisis analysis traced this problem to its root: banks couldn't aggregate risk exposures across business lines and legal entities quickly enough to inform decisions. When leadership can't see a consolidated picture, they can't govern — and that's a board-level accountability problem, not just a systems one.

Board Disengagement as a Root Cause

That accountability gap points to the third failure: boards that are structurally removed from the risk conversation. GRC programs that live entirely below the C-suite fail because risk decisions get made without the authority or accountability that only board-level governance can provide.

Common warning signs at the board level:

- Only hearing "green" without seeing tradeoffs or residual risk

- Cyber and risk reporting that's activity-based, not decision-based

- Annual risk briefings substituting for ongoing oversight

- No clear escalation path that brings material risk to the board before it becomes an incident

Boards that ask the right questions — what's our residual risk appetite, what decisions require board sign-off, what would trigger an escalation tonight — create the conditions for GRC programs that actually hold under pressure.

Key Factors That Shape GRC Complexity in Financial Services

Regulatory Fragmentation

U.S. financial services organizations operate under overlapping federal and state regulatory frameworks with different examination cycles, reporting requirements, and enforcement philosophies. A GRC framework must map obligations across all applicable regulators without creating duplicative or contradictory controls. The complexity compounds for institutions with multiple charters, product lines, or geographic footprints.

Third-Party and Vendor Risk

Financial institutions increasingly depend on fintechs, cloud providers, and specialized service firms whose failures or compliance gaps become the institution's problem. In June 2023, the OCC, FDIC, and Federal Reserve issued joint interagency guidance on managing third-party relationship risks across the full relationship lifecycle — from due diligence through exit.

GRC must extend beyond the institution's own walls to include:

- Vendor due diligence before onboarding

- Ongoing monitoring tied to business criticality

- Contractual accountability with breach notification requirements and audit rights

- Concentration risk tracking for critical service dependencies

Cyber Risk as a Governance Matter

Third-party dependencies also expand the cyber attack surface — which is one reason cybersecurity has moved squarely into governance territory. Boards are now expected to understand and oversee cyber risk, not delegate it entirely to IT.

The SEC's 2023 cybersecurity disclosure rules (Release No. 33-11216) require public companies — including public financial institutions — to disclose board oversight of cybersecurity risks and management's role in assessing and managing material cyber risks.

The regulatory expectation is unambiguous: boards are accountable for cyber governance, not merely informed of it. In practice, that means cyber risk must reach board agendas in business terms — not as a technical briefing that leaves directors without a clear path to a decision.

Board-level cyber reporting should connect to:

- Revenue exposure from operational disruption or data loss

- Legal and regulatory liability from breach or non-disclosure

- Operational continuity risk tied to critical systems

- Customer trust and reputational impact from incidents

Frequently Asked Questions

What is governance, risk, and compliance in simple terms?

GRC is an integrated approach where governance establishes who is in charge and accountable, risk management identifies what could go wrong and prioritizes responses, and compliance ensures the organization follows the rules it is legally and ethically bound by. The three functions are designed to work together, not operate as separate programs.

What is governance, risk, and compliance in banking?

In banking, GRC involves navigating a dense, overlapping regulatory environment (FDIC, OCC, Federal Reserve, CFPB, and state regulators) while managing financial, operational, and cyber risks simultaneously. Fragmented programs produce the blind spots that drove regulatory failures in 2008 and continue to generate enforcement actions today.

What is governance, risk, and compliance as a service?

GRC as a service is an engagement model where external advisors or fractional executives provide governance structure, risk oversight, and compliance program design without a full-time hire. It's most common during leadership transitions, post-incident recovery, or when an institution needs board-ready reporting on an accelerated timeline.

What are the pillars of governance, risk, and compliance?

The three pillars are governance (decision rights, accountability, and board oversight), risk management (identifying, assessing, and prioritizing threats against business objectives), and compliance (meeting external regulatory and internal policy requirements). Each pillar shapes and reinforces the others — gaps in one consistently surface as failures in the remaining two.

What are the 7 types of risk in banking?

The OCC identifies eight risk categories: credit, interest rate, liquidity, price, operational, compliance, strategic, and reputation. Cyber and technology risk now receives governance-level treatment alongside these categories. Modern GRC frameworks must address all categories in an integrated way, since gaps in one area frequently create exposure in others.

What are the 5 key areas of compliance in banking?

The five core compliance domains are:

- AML and Bank Secrecy Act obligations

- Data privacy and information security (GLBA, FFIEC)

- Consumer protection regulations (CFPB oversight)

- Capital adequacy and financial reporting (SOX for public institutions)

- Regulatory examination readiness across federal and state supervisors