Introduction

Regulatory audits are not internal reviews with friendly stakes. When HIPAA, SOX, PCI DSS, GDPR, or FINRA examiners arrive, the consequences for gaps are real — fines, enforcement actions, reputational damage, and board-level scrutiny that can follow an organization for years.

Many organizations treat compliance as a documentation exercise. They have policies written, frameworks named, and tools deployed. What they often lack is the continuous evidence trail, access governance, and board-level visibility that regulators actually test for.

The difference between controls on paper and controls that demonstrably operate is where audits are won or lost. Compliance solutions can shift compliance from a periodic scramble into an always-on operational function.

Tools alone don't close that gap, though. The governance structure around them determines whether the data those tools produce holds up when regulators start asking hard questions.

Key Takeaways

- Regulators test whether controls operate consistently, not just whether they exist on paper

- The most common audit failures involve access control gaps, missing documentation, and leadership blind spots — not missing software

- Compliance solutions automate evidence collection, but governance structure is what makes that data actionable

- Boards need trend metrics, named finding owners, and escalation thresholds — not raw platform data

- Audit readiness is a governance posture, not a pre-audit project

What Regulators Actually Examine During a Compliance Audit

Regulatory audits across frameworks — HIPAA, SOX, PCI DSS, GDPR, FINRA — follow a common logic. Auditors are not primarily checking whether policies exist. They are testing whether stated controls are operating consistently. That distinction between design effectiveness and operating effectiveness is the difference between passing and receiving a material finding.

PCAOB AS 2201 makes this explicit: design testing determines whether controls can prevent or detect material misstatements; operating effectiveness testing determines whether they actually do. Inquiry alone is not sufficient. Auditors expect four methods of evidence gathering: observation, documentation inspection, reperformance, and direct inquiry — in combination, not as substitutes for one another.

The Four Areas Auditors Assess

Across frameworks, auditors focus on four primary areas:

- Documentation and policy currency — Are policies current, and is there evidence they have been reviewed on a defined cycle?

- Control execution evidence — Access logs, change records, access review documentation, and incident records showing controls are actually running

- Personnel knowledge and behavior — Whether employees understand their obligations and act accordingly

- Corrective action history — Whether prior findings were assigned owners, remediated, and closed with documented evidence

Each of these requires continuous upkeep. Point-in-time preparation before an audit notice arrives is never sufficient.

The Governance Accountability Shift

Regulators increasingly focus beyond technical controls to governance accountability: who owns compliance obligations, how issues escalate, and whether leadership has genuine visibility into the compliance posture.

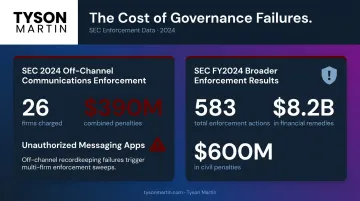

The SEC's FY2024 enforcement results reported 583 enforcement actions and $8.2 billion in financial remedies, including more than $600 million in civil penalties against more than 70 firms for recordkeeping failures tied to off-channel communications. Those penalties didn't reflect missing software. They reflected governance failures.

Why Organizations Struggle When Auditors Arrive

Most organizations that stumble during regulatory audits aren't missing compliance frameworks. They are missing the operational discipline to maintain evidence continuously and the governance structure to surface problems before regulators do.

The Documentation Gap

Organizations frequently have policies written but cannot produce evidence those policies are being followed. Missing logs, outdated records, and inconsistent timestamps are audit red flags — and regulators tend to assume the worst when evidence is absent rather than giving organizations the benefit of the doubt. HHS OCR enforcement records reflect this pattern directly: a Health Fitness Corporation settlement noted the organization failed to conduct an accurate and thorough HIPAA risk analysis until January 19, 2024 — years after the obligation existed.

The Access Control Problem

Over-privileged accounts, former employees retaining system access, and role changes without corresponding permission updates are among the most consistent findings in regulated industries. The Verizon 2024 Data Breach Investigations Report found stolen credentials involved in 24% of breaches and internal actors present in 35%. HHS OCR enforcement records include a case where a city health department failed to terminate a former employee's access to protected health information — a deprovisioning failure with direct regulatory consequences.

The Shadow IT Blind Spot

Employees adopt unauthorized tools that process regulated data outside approved channels. The SEC's 2024 off-channel sweep charged 26 firms with more than $390 million in combined penalties for failing to preserve business communications sent through unapproved messaging applications. In many of these cases, senior managers and supervisors were among those using the unauthorized channels. When auditors discover unauthorized tools during an examination rather than the organization finding them first, it signals a governance failure — not a technical gap that can be explained away.

The Corrective Action Gap

Organizations that identify compliance issues but fail to document remediation, assign ownership, or track resolution create compounding risk. Follow-up auditors arrive expecting structured corrective action plans with completion evidence — and find none.

The Leadership Visibility Problem

That operational gap rarely stays contained to the compliance team. Compliance status is typically siloed within IT or legal, leaving boards and executives with no reliable view into whether critical controls are actually working. When regulators or audit committees ask direct questions about organizational risk posture, leaders without that visibility cannot give defensible answers — and that exposure belongs on the governance agenda, not the IT agenda.

How Compliance Solutions Address These Gaps

Modern GRC platforms, identity management tools, and security information systems address audit vulnerabilities by replacing manual, periodic evidence gathering with continuous, automated capture. That shift matters because auditors can tell the difference between logs assembled the week before an audit and evidence that reflects ongoing operational discipline.

Automated Evidence Collection and Audit Trails

Compliance solutions capture user activity, configuration changes, access requests, and policy modifications in structured, timestamped logs. Auditors need to reconstruct what happened and when — automated logs eliminate the credibility risk of manually assembled evidence, which regulators view skeptically regardless of accuracy.

FINRA's books-and-records requirements make the standard explicit: records must be preserved in a non-rewritable, non-erasable format or an audit-trail alternative. The format of evidence matters, not just its existence.

Access Governance Capabilities

Well-governed access controls depend on two operational disciplines:

- Automated provisioning and de-provisioning tied to HR systems, so access rights reflect current roles and employment status in real time

- Documented access reviews conducted on a regular cadence, creating the evidence trail auditors expect for least-privilege compliance

Without that documentation, even well-managed access controls are difficult to defend.

Continuous Monitoring and Risk Surfacing

Compliance platforms that run continuous monitoring can identify control failures, policy deviations, and non-compliant applications between audit cycles — not just during them. The ability to detect a problem, remediate it, and document that remediation before regulators arrive is a material advantage.

IBM's 2025 Cost of a Data Breach Report found that organizations with extensive AI and security automation saved $1.9 million per incident compared to those without those capabilities. That savings gap reflects the same operational rigor regulators look for during an audit.

The Governance Layer That Tools Cannot Replace

Compliance tools surface data. They do not make decisions. The value of those tools scales entirely with the governance structure around them — who defines escalation thresholds, who owns remediation, and how findings reach leadership in a format that supports action.

Without that structure, compliance platforms generate reports that accumulate without consequences. Organizations that build governance around their tooling — clear owners, defined thresholds, actionable escalation paths — produce the evidence infrastructure regulators actually expect to see.

What Boards and Executives Need to Understand About Compliance Readiness

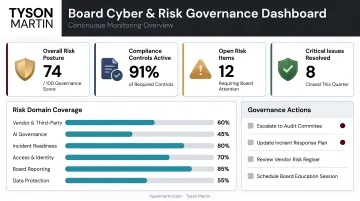

Compliance solutions create information. Boards need that information translated — not raw data exports, but clear risk posture summaries that support defensible decisions.

What Effective Board-Level Reporting Looks Like

Board-level compliance reporting should answer a narrow set of questions clearly:

- Are we in appetite or out of appetite on our key control areas?

- What changed since the last briefing?

- What findings are open, who owns them, and when do they close?

- Where is a decision required from this group?

Trend indicators matter more than point-in-time scores. A single metric showing whether risk exposure is improving, stable, or worsening is more useful to a board than a dashboard of green lights that doesn't show trajectory. Exceptions should remain visible until closed, with dates and consequences if deadlines slip.

Decision Rights: The Missing Governance Element

One of the most consistent governance failures in regulated industries is ambiguity about who is authorized to accept risk, approve exceptions, or escalate issues to the board. Compliance tools can flag issues. Without pre-defined escalation thresholds and ownership, those flags don't translate into action.

Clear decision rights cover five areas that should be resolved before a regulatory examination:

- Who accepts risk at what threshold

- Who approves compliance exceptions and for how long

- Who declares incident severity

- Who notifies regulators, counsel, and insurers

- Who owns vendor go/no-go decisions for critical suppliers

The Role of Senior Compliance Leadership

Translating compliance platform outputs into board-level governance requires someone who understands both the technical evidence and how regulators think. Organizations in transition, facing an examination, or lacking senior security leadership often cannot build that capacity internally on a fast timeline.

Tyson Martin works with boards and executive teams in this capacity: clarifying decision rights, tightening governance, and ensuring compliance reporting is defensible in front of regulators. For organizations that need an inspectable governance structure built quickly, the 90-day engagement model delivers a ranked risk view and clear ownership within the first 30 days. Evidence-ready compliance documentation and board-ready reporting follow by day 90.

That 90-day structure reflects a broader principle: audit readiness is not a pre-audit project. Boards that receive regular, consistent compliance metrics are far better positioned to respond to regulator questions than those that scramble to assemble evidence after an audit notice arrives.

Turning Audit Findings Into Governance Improvements

Unfavorable audit findings are most valuable when they surface root causes rather than just symptoms. A finding about missing access logs, for example, points to a process or ownership gap — not just a misconfiguration. Treating findings as systemic inputs, not isolated technical errors, is what separates organizations that improve governance from those that repeat the same findings in successive audit cycles.

What a Strong Post-Audit Corrective Action Process Looks Like

- Findings are assigned to named owners, not teams or departments

- Remediation plans include measurable milestones, not open-ended commitments

- Progress is reported to leadership on a defined cadence — weekly for active findings, monthly for status

- Closure requires evidence, not just a verbal update — "vendor committed to fix" is not done; "evidence received and validated" is done

- The corrective action record itself becomes audit evidence for the next cycle

This structure produces a documented governance trail — one that demonstrates defensible decision-making and follow-through, not just technical fixes, when follow-up auditors return.

Keeping Pace With Regulatory Change

Point-in-time compliance programs fail under sustained regulatory pressure because requirements keep moving. Thomson Reuters' Cost of Compliance survey identifies regulatory change as among the top ongoing challenges for compliance teams — alongside cost pressure, staff turnover, and budget constraints. Organizations in financial services, healthcare, and retail face overlapping and frequently updated requirements across multiple frameworks simultaneously.

The governance framework itself needs the same continuous maintenance as any individual control. Each of the following triggers a governance review — not just a technical update:

- Regulatory requirements revised or reissued

- Control environment changes (new systems, vendors, or processes)

- Key personnel turnover in compliance or risk roles

- Findings from prior audit cycles left unresolved

Organizations that treat these as administrative checkboxes tend to find the same gaps surfacing in the next audit. Those that embed them into a continuous governance calendar close findings — and keep them closed.

Frequently Asked Questions

What is regulatory compliance support?

Regulatory compliance support combines tools, processes, and governance structures that help organizations meet legal and industry requirements continuously — not just before an audit. Unlike one-time exam preparation, it sustains evidence collection, access governance, and leadership reporting across the full examination cycle.

How do you audit regulatory compliance?

A compliance audit follows five core steps: define scope against applicable regulations, test both control design and operating effectiveness, gather evidence from logs and documentation, identify gaps, and produce findings with assigned owners and deadlines. Under frameworks like PCAOB AS 2201, inquiry alone is insufficient — evidence must include documentation and observation.

What is the difference between a compliance audit and a regulatory audit?

An internal compliance audit is a self-assessment organizations use to test their own controls. A regulatory audit is conducted by an external body with enforcement authority — HHS OCR, SEC, FINRA, or PCI assessors — making the standards of evidence and the consequences of gaps significantly higher.

What documentation do regulators typically request during an audit?

Common requests include: access logs and user activity records, policy documents with revision history, evidence of periodic access reviews, prior audit findings and corrective action records, risk assessments, and incident response documentation.

How often should organizations conduct compliance audits?

Frequency depends on the framework. SOX requires annual management assessment with quarterly reviews; HIPAA requires periodic evaluation tied to environmental changes; FINRA Rule 3120 requires annual senior management reporting. Across all frameworks, treat compliance as a continuous operational function — not a calendar event.

What role does leadership play in compliance audit readiness?

Leadership sets the tone, allocates resources, defines decision rights and escalation thresholds, and ensures compliance reporting reaches the board in a format that supports defensible oversight. Without that governance layer, compliance tools generate data that never translates into action — a gap regulators consistently identify during examination.