Introduction

Sitting on a board carries real legal weight. Directors are entrusted with governing organizations on behalf of shareholders, and that trust comes with enforceable obligations — not just ethical expectations.

Many directors — particularly those new to board service — are unclear on exactly where their legal obligations begin and end. Regulatory scrutiny has intensified, shareholder litigation has grown more sophisticated, and cybersecurity has created entirely new categories of governance exposure.

A 2024 Cornerstone Research study found that nearly half of settled securities class actions from 2019–2023 had a parallel shareholder derivative action running alongside them. That's how aggressively governance failures are pursued.

This guide covers what fiduciary duties are, the core obligations directors must fulfill, what constitutes a breach, and how to build a governance posture that holds up under scrutiny — including the growing area of technology and cyber risk liability.

Key Takeaways

- Directors owe fiduciary duties — the duty of care, duty of loyalty, and duty of obedience — to the corporation and its shareholders under state corporate law

- The Business Judgment Rule protects directors who act in good faith, on an informed basis, and without conflicts — protection that disappears without documented process

- Most breaches trace to inattention or undisclosed conflicts, not bad intent

- Boards face real exposure for failure to act — not only for decisions that go wrong

- Cybersecurity oversight is now a formal fiduciary obligation, codified by the SEC's 2023 disclosure rules

What Are Fiduciary Duties?

The word "fiduciary" comes from the Latin fiducia, meaning trust. A fiduciary is someone entrusted to act on behalf of another, with a legal obligation to prioritize that party's interests above their own.

For corporate directors, fiduciary duties flow primarily to the corporation through its shareholders. Delaware courts have been unambiguous on this point.

In eBay Domestic Holdings v. Newmark, the Court of Chancery held that directors of a for-profit Delaware corporation must promote value for stockholders and cannot openly pursue strategies that subordinate shareholder wealth maximization to other goals. That framing also shapes who else — beyond shareholders — can make claims on directors. In North American Catholic Educational Programming Foundation v. Gheewalla, the Delaware Supreme Court held that creditors of an insolvent corporation may bring derivative claims against directors — though directors continue to owe duties to the corporation itself, not directly to creditors.

This question of who duties run to sits at the center of the shareholder primacy vs. stakeholder theory debate. The Business Roundtable's 2019 statement committed member companies to deliver value to customers, employees, suppliers, and communities — not just shareholders. Delaware case law for ordinary for-profit corporations, however, remains more shareholder-centric.

Legal Sources of Fiduciary Duty

- Delaware General Corporation Law (DGCL) — particularly Sections 141(a), 141(e), 144, and 102(b)(7)

- Common law equity principles developed through decades of Court of Chancery decisions

- Applicable federal regulations — including SEC rules that have formalized governance obligations in areas like cybersecurity disclosure

66.7% of Fortune 500 companies are incorporated in Delaware, making Delaware's fiduciary framework the de facto standard for major US corporate governance.

The Core Fiduciary Duties of Directors

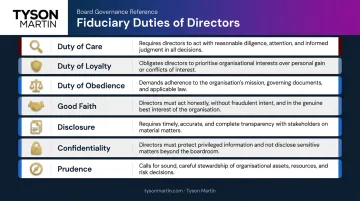

Three duties form the foundation of US corporate governance: duty of care, duty of loyalty, and duty of obedience. Additional duties — good faith, confidentiality, disclosure, and prudence — complete the framework.

Duty of Care

The duty of care requires directors to make informed decisions with the diligence a reasonably prudent person would exercise in the same role. In Smith v. Van Gorkom, the Delaware Supreme Court held that duty-of-care liability is predicated on gross negligence — and that directors must inform themselves of all material information reasonably available before acting.

In practice, this means:

- Attending and preparing for board meetings

- Reviewing financial reports and materials before votes

- Asking probing questions rather than rubber-stamping management recommendations

- Engaging independent experts when decisions exceed the board's existing knowledge base

The Business Judgment Rule is the legal protection that flows from properly fulfilling this duty. Under Aronson v. Lewis, courts presume that directors acted on an informed basis, in good faith, and in the honest belief that their action served the company's best interests. That presumption can be rebutted — but when it holds, courts generally defer to the board's decision even if the outcome was poor.

That deference is not guaranteed, however. Van Gorkom demonstrated that a weak or undocumented decision process can defeat the presumption entirely. Board minutes, expert reports, committee reviews, and recorded deliberation are the evidence base for the "informed basis" element.

Duty of Loyalty

The duty of loyalty requires directors to place the corporation's interests above personal financial interests or the interests of any third party. Guth v. Loft articulated the standard: directors may not use positions of trust to further private interests and owe "undivided and unselfish loyalty" to the corporation.

Two core applications:

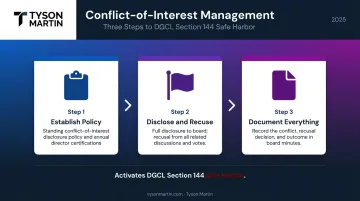

- Avoiding and disclosing conflicts of interest — DGCL Section 144 provides a safe harbor for interested-director transactions when material facts are disclosed and the transaction is approved in good faith by disinterested directors or stockholders, or is fair to the corporation

- Not appropriating corporate opportunities — the Guth test holds that an opportunity belongs to the corporation when it's in the company's line of business, the company has an interest or reasonable expectancy in it, and taking it personally creates a conflict

Proper conflict management requires full disclosure to the board, recusal from all related discussions and votes, and documentation of that recusal in board minutes. These same principles — disclosure, process integrity, and documented deliberation — carry through to the remaining duties that round out the governance framework.

Duty of Obedience and Beyond

The duty of obedience — traditionally articulated in nonprofit governance — requires directors to ensure the organization operates within the law, its governing documents, and its stated mission. For Delaware for-profit corporations, this obligation is enforced through a combination of duties: care, loyalty, good faith, oversight, and statutory compliance requirements.

Additional duties that complete the framework:

| Duty | What It Requires |

|---|---|

| Good Faith | Honest, integrity-driven decisions — located within the duty of loyalty per Stone v. Ritter |

| Disclosure | Communicating honestly with shareholders about material corporate affairs (Malone v. Brincat) |

| Confidentiality | Protecting non-public information obtained in the director role |

| Prudence | Risk-aware, data-informed decision-making on matters affecting the company |

Common Breaches of Fiduciary Duty

Most breaches aren't malicious. They stem from inattention, poor process, or undisclosed conflicts. Understanding the patterns is the most practical form of risk management available to any director.

Self-Dealing and Conflicts of Interest

Self-dealing occurs when a director approves a transaction that financially benefits themselves, a family member, or an affiliated business — without proper disclosure and recusal. It is the most litigated form of fiduciary breach and one of the clearest violations of the duty of loyalty.

The Enron board offers the most documented cautionary example. The US Senate Permanent Subcommittee on Investigations concluded that Enron's board failed to safeguard shareholders by allowing high-risk accounting, extensive undisclosed off-balance-sheet activity, and inappropriate conflict-of-interest transactions — including approving code-of-conduct waivers for CFO Andrew Fastow to participate in partnerships specifically designed to do business with Enron. Directors who waive their own conflict policies in private create the very evidence plaintiffs need in litigation.

Failure to Exercise Informed Judgment

Courts have found directors liable not for making wrong decisions but for failing to engage in the process of deciding at all. This breach takes several forms:

- Skipping board meetings without reviewing materials

- Voting on significant transactions without independent analysis

- Accepting management recommendations without scrutiny or questions

The Business Judgment Rule offers no protection here. Deference requires an informed process — and a director who shows up unprepared and votes yes has documented their own liability.

Misuse of Confidential Information

Confidential information obtained as a director — financial projections, M&A activity, strategic plans — cannot be used for personal benefit or shared with outside parties. Two categories of exposure apply:

- Intentional misuse — trading on non-public information or tipping an outside party before an announcement

- Inadvertent disclosure — mentioning a pending acquisition to a business partner, investor, or family member

The obligation runs in both directions. Under Malone v. Brincat — which held that directors owe shareholders an affirmative duty of honest communication — directors must protect information coming in and communicate honestly about material corporate affairs going out.

Consequences of Breaching Fiduciary Duties

Consequences fall into three categories, and they compound quickly.

Legal exposure:

- Personal liability through shareholder derivative lawsuits

- Regulatory enforcement actions

- Criminal charges in cases involving fraud or intentional misconduct

Financial consequences:

- Damage awards and disgorgement of profits

- Regulatory fines

- Substantial legal defense costs

Reputational damage:

- Loss of current and future board seats

- Lasting harm to the organization's stakeholder relationships and public credibility

D&O (Directors and Officers) insurance provides an important financial backstop, but IRMI notes that most D&O policies contain fraud and dishonesty exclusions, typically triggered after a final adjudication establishing the excluded conduct. Directors who acted in bad faith or committed intentional misconduct should not rely on insurance to cover the gap.

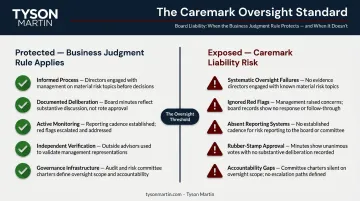

Courts have also moved beyond scrutinizing boards that acted wrongly to scrutinizing boards that failed to act. The Caremark standard, adopted by the Delaware Supreme Court in Stone v. Ritter, holds that directors can face liability for sustained or systematic oversight failures — including failures to implement adequate information and reporting systems.

Delaware courts have applied this analysis to cybersecurity oversight, though the bar remains high: plaintiffs must show an utter failure to oversee risk or a conscious decision to ignore red flags.

Fiduciary Duties in the Modern Boardroom: Cybersecurity and Technology Oversight

As organizations have grown dependent on digital infrastructure, regulators have formalized what responsible technology oversight actually requires — and the expectations are now explicit.

The SEC's 2023 cybersecurity disclosure rules are the clearest signal of this shift. Public companies must now file Form 8-K within four business days of determining a cybersecurity incident is material, and annual Form 10-K filings must describe board oversight of cybersecurity risks under Regulation S-K Item 106. Board oversight of cyber risk is no longer aspirational — it's a disclosure requirement.

The Governance Gap Most Boards Face

The duty of care doesn't require every director to be a technical expert. It requires the board to receive credible, consistent reporting on cyber risk posture, ask informed questions, and demonstrate that material risks are being actively monitored and escalated.

The gap most boards face is structural, not knowledge-based:

- Management presents technical metrics directors cannot interrogate

- There are no established escalation thresholds — no defined trigger for when an issue moves from management to the board

- Board materials describe cyber activity rather than business impact, making it impossible to compare cyber risk against other enterprise risks

This gap creates fiduciary exposure. A board cannot fulfill its oversight duty over something it cannot understand or measure.

Gartner reported in 2025 that 90% of non-executive directors lack confidence in cybersecurity value, with only 10% having strong confidence that cyber initiatives appropriately balance protection and cost. A separate 2024 Gartner survey found that 67% of non-executive directors rated current board practices as inadequate to oversee cyber risk.

What Defensible Cyber Oversight Looks Like

Boards that have addressed this gap share these characteristics:

- Consistent reporting format — a monthly risk pulse showing what changed, what needs a decision, and what is off track, plus quarterly deep reviews

- Business impact framing — risks mapped to financial loss, operational disruption, legal exposure, strategic delay, and reputational harm rather than technical metrics

- Clear escalation thresholds — a one-page escalation ladder defining when issues move from management to the board, with specific triggers and required information

- Independent verification — internal audit reviews, external assessments, and post-incident reviews so the board isn't relying solely on management's self-reporting

Tyson Martin's board advisory engagements address this specific problem. Working independently of the in-house CISO and security vendors, he produces materials that translate cyber risk into the business-impact terms boards can act on:

- A prioritized risk register with named owners tied to revenue, operations, and legal exposure

- Board briefing templates that lead with decisions needed, not activity summaries

- Incident readiness scorecards based on tested behaviors

The goal is clear decision rights, fewer surprises, and governance documentation that holds up when regulators ask questions.

How Directors Can Uphold Fiduciary Duties in Practice

Strong governance is process discipline, applied consistently.

Document Everything

Detailed board minutes are a director's primary legal defense. They should capture the information presented, the questions asked, the alternatives considered, and the rationale behind decisions. The Business Judgment Rule's "informed basis" element lives or dies in the minutes.

Manage Conflicts with Process, Not Instinct

- Establish a standing conflict-of-interest disclosure policy

- Require annual certifications from all directors

- Document every recusal — the conflict, the decision to recuse, and the outcome — in board minutes

Informal conflict management creates informal liability — the Section 144 safe harbor requires documentation to apply.

Treat Governance Competency as an Ongoing Responsibility

Fiduciary duties evolve with case law, regulation, and emerging risk areas. NYSE Section 303A requires listed companies to maintain governance guidelines that include director continuing education expectations.

Spencer Stuart's 2024 US Board Index found that 99% of S&P 500 boards conduct some form of annual performance evaluation — self-assessment catches governance gaps before they become liabilities.

Directors should:

- Engage outside counsel or board advisors before making decisions in unfamiliar territory

- Participate in regular governance-focused education, particularly as new risk areas emerge

- Conduct board self-assessments annually and take the findings seriously

Document a deliberate, informed, conflict-free process — and the Business Judgment Rule's protection stays intact.

Frequently Asked Questions

What are the fiduciary duties of directors?

Fiduciary duties are the legal and ethical obligations directors owe to the corporation and its shareholders, enforceable under state corporate law — particularly in Delaware. The three core duties are duty of care (making informed, diligent decisions), duty of loyalty (placing corporate interests above personal interests), and duty of obedience (operating within the law and governing documents).

What are three examples of breaches of fiduciary duty?

Three common breaches: (1) self-dealing — approving a transaction that personally benefits the director without disclosure or recusal; (2) uninformed decision-making — failing to review materials or attend meetings before voting on significant matters; (3) misappropriating a corporate opportunity — taking a business opportunity for personal gain that should have been offered to the company first.

Can a director be held personally liable for breaching fiduciary duties?

Yes. Directors can face personal liability through shareholder derivative lawsuits, regulatory fines, and — in cases of fraud or intentional misconduct — criminal charges. D&O insurance provides no protection for bad-faith or intentional wrongdoing, so documented process matters regardless of coverage.

What is the Business Judgment Rule and how does it protect directors?

The Business Judgment Rule is a judicial doctrine under which courts defer to a director's decision if it was made in good faith, on an informed basis, and without a conflict of interest. It's the primary legal protection available to directors — but it requires documented, deliberate process to hold. A poorly documented decision process can defeat the protection entirely.

How do fiduciary duties apply to cybersecurity oversight?

Under the duty of care, directors must receive credible cyber risk reporting, ask informed questions, and ensure material vulnerabilities are escalated appropriately. The SEC's 2023 rules require public companies to disclose material incidents within four business days and describe board cyber oversight in annual filings. Technology oversight is now a formal, auditable governance obligation.

How should a director manage a conflict of interest?

Disclose the conflict fully and promptly to the full board. Recuse from all related discussions and votes — not just the final vote. Ensure the recusal, the nature of the conflict, and the board's independent process are documented in the meeting minutes. This documented process is what activates the DGCL Section 144 safe harbor.