Introduction

Boards and executive teams face a question they often can't answer: Are our security controls actually working? Not whether they're documented. Not whether policy says they should work. Whether they're performing right now, under current conditions, in the real environment.

That gap matters. According to PwC's 2026 Global Digital Trust Insights Survey, only 6% of business and technology leaders feel very capable of withstanding cyber attacks across all surveyed vulnerabilities. That's not a technology problem — it's a visibility and governance problem.

A Security Controls Assessment (SCA) is the structured process for closing that gap. It answers whether the controls you rely on are correctly implemented, operating as intended, and producing the outcomes they're supposed to produce.

Organizations that skip or delay SCAs carry more than cyber risk. They carry regulatory liability and board-level accountability failures that compound quietly until an incident or audit forces the issue.

This guide walks through what an SCA is, why it belongs in governance conversations, and exactly how to run one.

Key Takeaways

- An SCA evaluates whether security controls are implemented correctly and working as intended — not just whether they exist on paper

- SCAs differ from risk assessments: risk assessments identify threats; SCAs verify whether controls addressing those threats are actually performing

- Framework choice — NIST CSF, NIST 800-53, ISO 27001, or CIS Controls — depends on your industry and compliance obligations

- The SCA process follows a repeatable cycle: scope → evidence → test → document → remediate → monitor

- For boards, SCA findings should translate into a clear risk posture update with decisions required — not a list of technical vulnerabilities

What Is a Security Controls Assessment?

NIST defines a security control assessment as the testing or evaluation of security controls to determine whether they are implemented correctly, operating as intended, and producing the desired outcome. That definition sets a high bar. Documentation alone won't cut it, and policy attestation doesn't either. You need evidence of performance.

SCA vs. Risk Assessment: A Critical Distinction

These two are frequently confused, and that confusion creates false confidence.

| Question It Answers | |

|---|---|

| Risk Assessment | What threats and vulnerabilities exist, and how severe is the exposure? |

| Controls Assessment | Are the safeguards we rely on actually implemented and working? |

Both are valuable. But an organization that completes a thorough risk assessment and assumes its controls are functioning hasn't answered the right question. The risk assessment identifies what you need protection from; the SCA confirms whether that protection exists in practice.

What an SCA Can Cover

Scope depends on which assets are most critical, but common control categories include:

- Access and identity management

- Data protection and encryption controls

- Incident response readiness

- Application security controls

- Infrastructure configuration and hardening

- Cloud and SaaS environment controls

- Vendor and third-party access

Why Security Controls Assessments Matter for Enterprise Governance

Controls drift. Software updates, personnel changes, vendor integrations, cloud migrations — any of these can quietly degrade a control that passed its last review. The organization still believes it's protected, but the gap lives between what the policy says and what the environment actually does.

NIST SP 800-37 Rev. 2 formally incorporates continuous monitoring into the Risk Management Framework specifically because of this reality: systems and environments change, and controls must be re-validated as they do.

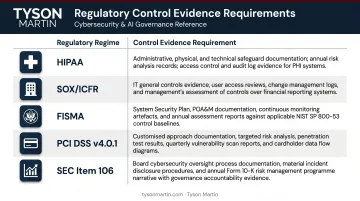

The Regulatory Case

Regulators don't accept policy documentation as proof that controls work. They expect evidence of effectiveness:

| Regime | Requirement |

|---|---|

| HIPAA Security Rule | Periodic technical and nontechnical evaluations required after environmental or operational changes affecting ePHI |

| SOX / ICFR | Material weaknesses in ICFR render internal controls ineffective; PCAOB AS 2201 requires IT general control evaluation |

| FISMA | Annual independent evaluations of information security programs against implemented-correctly/operating-as-intended standards |

| PCI DSS v4.0.1 | Customized controls require documented evidence of effectiveness, not just policy description |

| SEC Item 106 | Public companies must describe processes for assessing and managing material cybersecurity risks, and board oversight of those processes |

The HIPAA data illustrates how often these requirements go unmet. HHS OCR's audit report found that 86% of covered entities failed to substantially fulfill security risk analysis requirements, and 94% failed risk management requirements. These organizations had programs. They didn't have evidence of control performance.

The Business Case

Compliance is the floor, not the ceiling. An effective SCA also delivers:

- Prioritizes remediation spending toward controls that most directly reduce real risk, not just the ones easiest to fix

- Reduces breach likelihood and cost — IBM's 2025 Cost of a Data Breach Report puts the global average breach at $4.4M, with $1.9M in average savings for organizations using security AI and automation effectively

- Gives leadership a defensible, inspectable view of security posture that holds up under regulatory scrutiny and board questioning

How to Perform a Security Controls Assessment: Step by Step

The SCA process works best as a repeatable governance cycle, not a one-time compliance event. The most common failure point: organizations assess controls in isolation from the assets and risks those controls are supposed to protect. Don't let that happen. Ground every step in what actually matters to the business.

Step 1 – Define Scope and Objectives

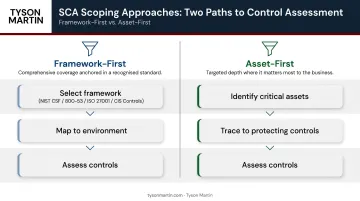

Start by identifying which controls to assess. Two approaches work well:

- Framework-first: Use NIST CSF, NIST 800-53, ISO 27001, or CIS Controls as your control catalog, then map to your environment

- Asset-first: Identify the organization's most critical information assets, then trace back to the controls protecting them

The asset-first "heatmap" approach keeps the assessment focused on what matters most, not only where documentation happens to exist.

For each control in scope, document its objective . Without a defined objective, there's no basis for determining whether the control is working.

Step 2 – Assign Ownership and Establish Process Structure

Clarify roles before any testing begins:

- Who leads the overall SCA?

- Who owns individual control domains (identity, infrastructure, incident response, etc.)?

- What is the escalation path when deficiencies are found?

- Who has authority to accept identified risk versus who must escalate?

In lean teams, this is shared responsibility — which means it needs explicit scheduling and manager buy-in, not just an assumption that everyone knows their role.

External support is often valuable here. An independent assessor such as a fractional CISO reduces self-assessment bias and brings objectivity that internal teams, who are close to the work, cannot easily provide on their own.

Step 3 – Gather Control Documentation and Evidence

Collect existing documentation for each control in scope:

- Policy statements and procedures

- Configuration records and system security plans

- Prior assessment results and audit findings

- Vendor contracts and access records

Two things to expect: documentation is frequently incomplete, and what exists is often outdated. Both are findings, not just inconveniences.

Before testing begins, verify that each control's documented objective still matches current operational reality. Gaps discovered here frequently reveal controls that were modified through updates, vendor changes, or organizational shifts without any formal review.

Step 4 – Test Controls and Evaluate Effectiveness

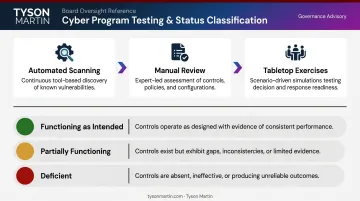

NIST SP 800-53A Rev. 5 describes three assessment methods: examine, interview, and test. In practice, effective SCA testing combines:

- Automated scanning for configuration and vulnerability controls

- Manual review for policy and process controls

- Tabletop exercises or simulations for incident response and continuity controls

The output of testing isn't just raw data. Analyze results against each control's objective and classify each as:

- Functioning as intended — evidence confirms the control operates correctly

- Partially functioning — the control exists but has gaps in coverage or consistency

- Deficient — the control fails to meet its objective under one or more conditions

Document the specific conditions under which deficiencies occur. Raw data without that analysis is not a finding.

Step 5 – Document Findings and Update Control Records

Produce a findings report that states for each control:

- Whether it is adequate or deficient

- What evidence supports that determination

- What the potential risk impact is if the deficiency goes unaddressed

Write findings so that risk managers and executives can read them — not just security engineers. A technical finding buried in configuration output is not governance-ready.

Update all control documentation to reflect current state, including integrations, dependencies, and system changes that may have altered how controls operate since last review.

Step 6 – Remediate, Assign Owners, and Plan for Continuous Monitoring

Prioritize remediation by risk impact, not ease of fix. For each deficiency:

- Assign a named owner — a role, not a committee

- Set a specific deadline

- Define the proof required for closure (test results, logs, screenshots)

- Estimate cost and dependencies

For monitoring after the assessment, establish a cadence that matches control risk level:

- High-risk controls in regulated environments: continuous automated monitoring with amber/red escalation thresholds

- Standard controls: monthly review cadence tied to executive reporting

- Full SCA cycle: annually, or triggered by significant system changes, M&A, new leadership, or a security incident

Treat the completed assessment as a baseline, not a finish line. Controls drift as systems change, teams turn over, and new vendors come online — so the monitoring cadence is what keeps the SCA useful between full cycles.

Turning SCA Findings Into Board-Ready Decisions

The most common failure after an SCA isn't in the assessment itself. It's in translation. Findings stay in a technical report. They never reach the board in a form that enables decisions. A 40-page findings document is not a governance artifact — it's a way to avoid a governance conversation.

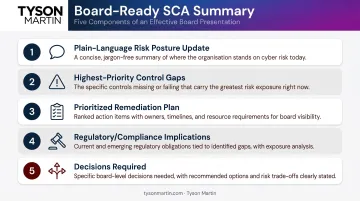

What Board-Ready SCA Reporting Looks Like

A board-ready SCA summary should contain:

- Plain-language risk posture update — what changed since last review, not a list of technical findings

- Highest-priority control gaps with potential business exposure (revenue, operations, legal, regulatory)

- Prioritized remediation plan with named owners and deadlines

- Regulatory or compliance implications requiring board awareness

- Decisions required — which gaps require board approval versus management action

The SCA should clarify which remediation decisions belong to management and which require board-level escalation. Ambiguity here is where incidents turn into governance failures.

Decision Rights in Practice

The SEC's cybersecurity disclosure rules, effective for fiscal years ending December 15, 2023 onward, require public companies to describe how the board oversees material cybersecurity risks and how management assesses and manages them. SCA output needs to connect directly to board decision authority — not sit in an IT department queue.

For each significant finding, the board packet should answer:

- Risk accepted or formally declined

- Remediation funded with a budget decision on record

- Accountable owner assigned by name

- Deadline approved and tracked

- Residual risk escalated if it exceeds the board's stated risk appetite

Those are governance decisions. Anything less is just reporting.

How Tyson Martin Can Help

Running a Security Controls Assessment that actually drives decisions — rather than just producing documentation — requires technical depth and the ability to translate findings into plain-English governance reporting. That's where Tyson Martin works.

Tyson holds CISSP certification and PCI Internal Security Assessor (ISA) credentials, with senior executive experience at AWS, Home Depot, Best Buy, and across regulated industries.

As a fractional or interim CISO, he steps in to lead or structure an organization's SCA process, build the governance framework around it, and ensure findings reach boards and executive teams in clear, actionable language.

For organizations doing a first-time assessment or working through a transition — new leadership, post-incident recovery, M&A — Tyson offers a structured 10-to-15-business-day sprint that delivers:

- A decision-rights map (RACI) with clear ownership across control domains

- A control maturity snapshot covering what's strong, weak, and inconsistent

- An evidence gaps list identifying what cannot currently be proven to auditors or the board

- A 90-day remediation plan with named owners, due dates, and proof requirements

- Draft metrics for a stable leadership scorecard

The outcome is an inspectable, repeatable process: defined decision rights, escalation thresholds, and a remediation plan tied to measurable outcomes. When regulators, auditors, or the board ask hard questions, the answers are already documented.

Frequently Asked Questions

What is a security controls assessment?

A Security Controls Assessment is a formal evaluation that tests whether an organization's security controls are correctly implemented, operating as intended, and producing the desired security outcomes. It confirms controls actually work — not just that they exist on paper.

Is SOC 2 an audit or assessment?

SOC 2 is a formal audit conducted by an independent CPA firm that produces a third-party attestation report used for customer and partner trust. A security controls assessment is typically an internal or advisory-led evaluation — it can prepare an organization for SOC 2, but it is not itself a CPA attestation.

What is the difference between a security controls assessment and a risk assessment?

A risk assessment identifies threats, vulnerabilities, and their likelihood and impact. A controls assessment evaluates whether the controls designed to address those risks are correctly implemented and working. Both are valuable and complementary, but they answer different questions.

How often should a security controls assessment be performed?

Most organizations run a full SCA cycle annually, with continuous monitoring for high-risk controls in regulated environments. Additional triggers include significant system changes, new leadership, M&A activity, or a security incident.

What frameworks are typically used in a security controls assessment?

Common frameworks include NIST CSF 2.0, NIST SP 800-53 Rev. 5, ISO/IEC 27001:2022, and CIS Controls v8. Regulated industries may also align to the HIPAA Security Rule, SOX ITGC controls, or PCI DSS v4.0.1 — the right choice depends on the organization's compliance obligations and risk profile.

Who should lead a security controls assessment?

An SCA can be led by an internal security team, a compliance function, or an external advisor. Independent assessment is generally preferred to reduce self-assessment bias. Organizations in transition, or those without a full-time CISO, frequently benefit from a fractional or interim security executive leading the process with objectivity and governance focus.