Introduction

Global cybersecurity spending is projected to reach $211.6 billion in 2025, according to Gartner's latest forecast — a 15% jump in a single year. Yet the average data breach now costs $4.88 million, up 10% from 2023. More spending, higher losses. That gap points to a specific failure: spending without visibility into whether controls are actually working.

The question boards will ask after the next incident is not "How much did we spend?" It's "Were our controls actually working?"

Most organizations run security risk assessments. But their value hinges almost entirely on how well controls are documented, tested, and connected to business decisions. An assessment without rigorous control evaluation produces findings — not risk reduction.

What follows covers how controls determine the credibility of a risk assessment — and what boards and executives should be asking about them before the next incident forces the conversation.

Key Takeaways

- Security controls reduce identified risks — without them, an assessment produces findings with no path to action.

- Controls make residual risk calculable: the number boards need for real decisions, not theoretical worst-case scenarios.

- Well-documented, tested controls are what separate an assessment that drives investment from one that gets ignored.

- Missing or untested controls produce inflated risk ratings, weak audit outcomes, and reactive incident management.

- Full value requires controls mapped to specific risks, periodic validation, and output formatted for governance review.

What Are Security Controls in a Risk Assessment?

Security controls are structured safeguards — policies, processes, and technologies — that an organization puts in place to prevent, detect, or respond to specific risks. NIST defines them as safeguards or countermeasures prescribed to protect confidentiality, integrity, and availability.

A policy states intent. A control enforces it — and that distinction matters more than most governance documents acknowledge.

Where Controls Fit in the Assessment Process

Controls appear after threats and vulnerabilities are identified, and before final risk ratings are assigned. They are what shift a risk from its inherent level (raw, pre-control exposure) to its residual level (what remains after defenses are applied).

Without that shift, every identified threat registers at full severity. The risk register becomes either alarming or, worse, routinely ignored.

What Controls Are Actually For

Controls give leadership a verifiable, reportable picture of actual exposure — replacing theoretical worst-case scenarios with a defensible, current reading of managed risk. That's the deliverable that matters to the audiences evaluating your program:

- Boards and audit committees — need to confirm exposure is understood and managed

- Regulators — assess whether controls exist and are operating as designed

- Cyber insurers — underwrite based on control maturity, not policy intent

Why Security Controls Matter: Three Key Advantages

These three advantages are practical. Each one changes how organizations make decisions, allocate resources, and defend their risk posture under scrutiny.

Advantage 1: They Convert Threats Into Measurable Residual Risk

Without documented, operational controls, a risk assessment can only measure inherent risk — raw, unmitigated exposure. Controls are what make residual risk calculable.

Assessors evaluate which controls are in place, test whether they are operating as intended, and apply those findings to adjust risk scores. Where controls are failing, risk stays elevated. Where they are effective and tested, scores come down — and that difference is defensible.

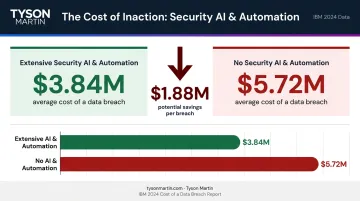

The cost case for tested controls is concrete. IBM's 2024 Cost of a Data Breach Report found that organizations with extensive security AI and automation averaged $3.84M in breach costs, versus $5.72M for those with no use — a $1.88M difference. Maturity in security controls directly affects loss exposure.

For boards, residual risk is the only number that supports a defensible decision. Without it, executives either over-invest in areas already controlled or under-invest in genuine gaps. NACD's 2026 Cyber Risk Oversight guidance explicitly calls for risk quantification models that translate technical metrics into objective decision-making inputs.

Track these metrics to verify the control-to-risk connection is working:

- Residual risk score per asset class

- High-risk findings reduced to acceptable levels

- Percentage of identified threats with active, tested controls

Board risk briefings, regulatory examinations, and post-incident reviews are where this advantage surfaces — any moment leadership must show that risks are managed, not just catalogued.

Advantage 2: They Enable Prioritized, Defensible Resource Allocation

When control coverage is mapped against identified threats, gaps become visible and rankable. Leadership can see which risks are already mitigated and where spending is genuinely needed.

A control gap analysis within a risk assessment produces a prioritized remediation list, ordered by residual risk severity, business impact, and control feasibility. Security and finance leadership get a shared basis for budget decisions — not competing opinions.

Security budgets are under real pressure. IANS/Artico research found that 71% of average security spend goes toward running daily operations, leaving limited budget for improvement. Without control-informed prioritization, organizations tend to protect areas that look risky rather than areas that are risky.

One pattern worth noting: organizations frequently measure activity rather than outcomes — patch counts, training completions, blocked alerts. Those metrics describe motion. Residual risk data describes whether the program is actually reducing exposure.

Control-to-risk mapping makes the prioritization argument before the budget conversation starts. It removes political friction from remediation decisions by grounding them in data. That matters: Verizon's 2024 DBIR found organizations take roughly 55 days to remediate 50% of critical vulnerabilities, while median exploitation time for known vulnerabilities is 5 days. Closing that gap requires funded priorities, not activity reports.

What to measure:

- Security budget allocation against highest-severity gaps

- Critical gaps with funded remediation plans

- Time-to-remediation for high-severity findings

Annual planning cycles, M&A due diligence, and regulatory readiness reviews are the moments this pays off — when security investment decisions must be explained clearly to non-technical stakeholders.

Advantage 3: They Provide the Evidence Layer for Compliance and Audit Readiness

Regulators, auditors, and cyber insurers do not evaluate intent. They evaluate what controls exist, whether they are operating correctly, and how gaps are being managed.

Major frameworks require organizations to not only identify risks but demonstrate what controls address them:

- HIPAA Security Rule (45 CFR 164.308) requires both a thorough risk analysis and implementation of controls sufficient to reduce identified risks to a reasonable level

- NIST CSF 2.0 structures outcomes around governance, risk identification, and risk treatment

- ISO/IEC 27001:2022 requires documented risk assessment and risk treatment tied to specific controls

- PCI DSS v4.0.1 includes targeted risk analysis requirements with documented control justifications

A risk assessment with full control mapping satisfies these requirements directly. One without it creates a secondary documentation project every time an auditor asks for evidence.

HHS OCR's April 2026 ransomware settlement announcements are instructive: multiple investigations cited failures to conduct accurate and thorough risk analysis as a primary deficiency — not the breach itself, but the absence of documented, managed risk assessment.

In regulated industries, absent control documentation is itself a compliance deficiency — not just a gap to address later. Organizations with organized, current control evidence spend measurably less time in audit remediation cycles. Cyber insurers apply the same lens: Marsh's guidance identifies specific controls — MFA for privileged access, endpoint detection, secure backups, patch management — as direct inputs to risk posture evaluation.

What auditors and insurers will look for:

- Audit finding count and severity

- Time spent on evidence collection during examinations

- Regulatory examination outcomes

- Cyber insurance application outcomes

For organizations under active regulatory oversight, preparing for SOC 2 or ISO certification, or operating in sectors where an incident triggers mandatory inquiry, this is where documentation quality directly determines outcomes.

What Happens When Security Controls Are Missing or Ignored

The most immediate consequence is inflated residual risk. Without controls in the assessment, every identified threat registers at full inherent severity. Risk registers become either alarming by default — or, if leaders learn to discount them, ignored entirely. Either outcome is expensive.

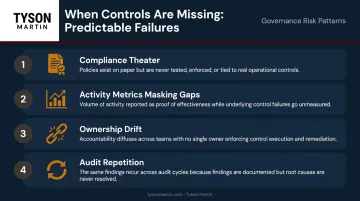

Recurring Failure Patterns

Organizations without well-integrated controls in their risk assessments tend to show predictable governance failures:

- Compliance theater: Strong documentation, weak operational reality. "MFA required" in policy; admins still using shared accounts. Backup standards on paper; no proven restores on revenue-critical systems.

- Activity metrics masking gaps: Patch counts, training completions, and blocked alert volumes look busy but don't answer whether crown-jewel systems are actually protected.

- Ownership drift: Findings accumulate with no named owner, no due date, no evidence of closure. Risk becomes background noise.

- Audit repetition: The same findings appear cycle after cycle because no one confirmed the fix held.

These patterns are manageable in stable conditions. Under pressure, they become liabilities.

Where It Gets Expensive

Organizations in leadership transitions, M&A events, or regulatory scrutiny are especially exposed. Gaps that were always present surface at the moment the organization can least afford them.

In M&A specifically, traditional due diligence often treats cybersecurity as a checkbox. Post-acquisition is when unknown risks become acquired risks — inherited vulnerabilities, unaddressed audit findings, and undocumented access paths discovered after the deal closes.

When control data is absent or unreliable, executive risk reporting defaults to narratives. Boards cannot govern on stories. The practical exposure: under SEC cybersecurity disclosure rules, "knew or should have known" is a legal standard, not a rhetorical one — and missing control evidence makes that standard very hard to meet.

How to Get the Most Value from Security Controls in Risk Assessment

Security controls deliver full value only when three conditions hold consistently:

- Mapped to specific risks — not listed in an appendix but tied to the threats and vulnerabilities identified in the assessment

- Operationally verified — tested periodically rather than assumed, with evidence that proves controls work under realistic conditions

- Connected to governance reporting — formatted to support decisions at the board and committee level, not just tracked in technical dashboards

What Good Looks Like in Practice

The reporting question is where most organizations fall short. A security team that understands controls is one thing. A governance structure that translates control status into clear escalation thresholds and defensible risk decisions is another — and most organizations haven't built the second one.

Boards need a stable, one-page view: top risks tied to business impact, trend metrics with targets, decisions required from leadership, and proof artifacts (test results, exercise outcomes, restore evidence). Not a dense technical report. Not a status update that ends with "we're working on it."

Specific control metrics that translate well to board reporting include:

- Patch SLA performance for crown-jewel systems

- MFA coverage for privileged access

- Backup restore test pass rate

- Time to contain high-severity incidents

- Overdue high-risk remediation items with aging

This is the practical work Tyson Martin does with boards and executive teams: ensuring control data becomes clean, stable, and reportable rather than a source of noise. A typical engagement produces a one-page dashboard, a decision-rights map, and a 90-day remediation roadmap with named owners and measurable outcomes. The structure runs on a quarterly board review cycle, with monthly executive check-ins between formal meetings.

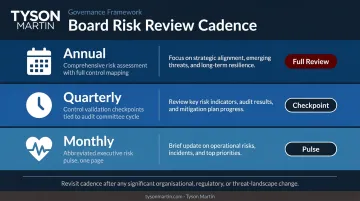

Build a Repeatable Cadence

Threat landscapes shift, systems change, and controls degrade without active management. Control assessment requires a repeatable cadence:

- Annual: Comprehensive risk assessment with full control mapping against the organization's framework of record

- Quarterly: Control validation checkpoints tied to the risk or audit committee review cycle

- Monthly: Abbreviated risk pulse for executive teams — one page, what changed, what needs a decision

Following significant changes (acquisitions, new platforms, leadership transitions, regulatory shifts), revisit immediately rather than waiting for the next scheduled cycle.

Frequently Asked Questions

Why are security controls important in a security risk assessment?

Security controls determine residual risk — without them, assessors can only measure raw, theoretical exposure, not actual managed risk. They translate threat findings into actionable priorities and give leadership a defensible, verifiable picture of what exposure remains after defenses are applied.

How do you evaluate the effectiveness of security controls?

Effectiveness requires active testing — not annual assumption. Confirm controls are implemented correctly, operating under realistic conditions, and producing measurable outcomes: incidents contained, audit findings reduced, recovery times met.

What are the four types of security controls, with examples?

Controls fall into four categories: preventive (firewalls, access controls), detective (SIEM, intrusion detection), corrective (incident response procedures, patch management), and deterrent (security awareness training, policy enforcement) — each serving a different role across the risk reduction lifecycle.

What happens if security controls are not addressed in a risk assessment?

Risk ratings default to worst-case inherent levels, remediation becomes unfocused, and the organization loses its ability to demonstrate managed risk to auditors, regulators, or its own board. The result is findings on paper with no evidence layer to act on or defend.

How often should security controls be reviewed as part of a risk assessment?

At minimum, an annual comprehensive review aligned with the organization's risk assessment cycle. High-criticality controls warrant quarterly validation — or more frequent review following significant changes to systems, leadership, or regulatory requirements.

What is the difference between a security control and a security policy?

A policy states intent ("access to sensitive data will be restricted"). A control is the enforceable mechanism that makes it real — for example, role-based access configured directly in the system. Without controls, a policy documents intent, not protection.