Introduction

Boards and executive teams rarely lose sleep over their own systems — they lose sleep over vendors. The organizations they've outsourced to, integrated with, and granted access to represent some of the hardest risks to see and the easiest to underestimate. Most enterprises maintain dependencies with dozens of third-party vendors. Some deal with hundreds.

According to a study cited by Imprivata, nearly half of organizations suffered a third-party data breach in 2024. When a vendor incident hits, the cascade is predictable: headlines, regulatory scrutiny, and board-level questions no one rehearsed.

A vendor risk assessment (VRA) is the process that surfaces those risks before they become crises. This guide covers:

- What a VRA actually is and why it matters at the governance level

- Which risk categories must be addressed

- How to conduct one, step by step

- What the assessment report should contain

- What boards and executives need to understand about their oversight role

Key Takeaways

- A vendor risk assessment is a structured evaluation of the risks a specific third-party vendor relationship carries.

- Six risk categories matter most: cybersecurity, compliance, operational, financial, reputational, and fourth-party exposure.

- Effective assessments start with vendor tiering—not every vendor deserves the same depth of scrutiny.

- The VRA report must work for both the security team and the boardroom — summary up top, supporting detail below.

- Boards own risk appetite and exception decisions — management owns execution and ongoing vendor oversight.

What Is a Vendor Risk Assessment?

A vendor risk assessment is a structured process for evaluating the risks an organization takes on when engaging a third-party vendor, supplier, or service provider. It covers cybersecurity exposure, compliance posture, operational dependencies, and financial stability.

It is not the same as third-party risk management (TPRM). TPRM is the broader program and lifecycle — vendor selection, contracting, monitoring, offboarding. A VRA is one specific activity within that program: the structured evaluation that produces evidence and findings to inform those decisions.

Why VRAs Are Legally and Regulatorily Required

Regulators treat vendor risk assessment as a required governance control, not an optional best practice:

- OCC/FFIEC (financial services): Interagency Guidance on Third-Party Relationships requires documented risk management across the vendor lifecycle

- HIPAA (healthcare): Business Associate Agreements and the Security Rule mandate vendor oversight

- PCI DSS (payments/retail): Third-party security assurance requirements apply to any vendor touching cardholder data

- GDPR: Article 28 requires formal contracts with data processors and ongoing accountability

- NIST CSF 2.0: Vendor risk management is embedded across the framework's Govern and Identify functions

Organizations without documented VRA processes face audit exposure and direct regulatory liability. The OCC assessed a $250 million civil money penalty against one institution in 2024, with vendor management control deficiencies as a contributing factor.

When to Conduct a VRA

| Trigger | Description |

|---|---|

| Initial onboarding | Before a contract is signed |

| Scope change | Vendor gains new access or expands services |

| Security incident | Any breach or event involving the vendor |

| Periodic reassessment | Based on vendor risk tier (annually for critical vendors) |

The goal isn't a completed checklist. It's a defensible, documented record of due diligence that supports a risk-based business decision — one where risk is understood, accepted, and clearly owned.

Types of Vendor Risk You Need to Evaluate

The core risk categories every VRA must address:

- Cybersecurity risk — data breach exposure, access controls, vulnerability management, incident response capability

- Compliance risk — adherence to applicable regulations and contractual obligations

- Operational risk — vendor stability, service continuity, and disaster recovery capability

Those three get most of the attention. These next three tend to surface only after something goes wrong:

- Financial risk — vendor solvency and capacity to sustain service delivery long-term

- Reputational risk — vendor conduct, public incidents, or ESG exposure that could reflect on your organization

- Fourth-party/supply chain risk — the vendors your vendor relies on, which extend your exposure further down the chain

The relevant categories depend on what the vendor does and what data or systems they can access. A payroll processor carries different risk than a marketing platform. Vendor tiering and scoping need to happen before any assessment begins. Without it, you're evaluating everything against the same standard — which wastes resources and distorts the findings that actually matter.

How to Conduct a Vendor Risk Assessment: Step-by-Step

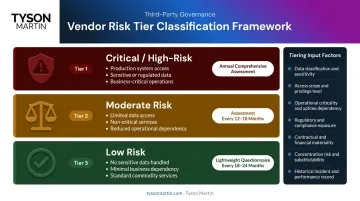

Step 1: Tier and Scope the Assessment

Vendor tiering is the prerequisite for everything else. Before gathering a single piece of evidence, classify the vendor by inherent risk level:

- Tier 1 (Critical/High-Risk): Production access, sensitive data, business-critical operations — failure would stop revenue or trigger a compliance violation

- Tier 2 (Moderate): Limited data access, non-critical services, manageable substitution options

- Tier 3 (Low-Risk): No sensitive data access, minimal operational dependency

Tiering inputs should include: data sensitivity, system access level, operational criticality, regulatory exposure, and concentration risk.

Scoping follows directly from tiering. Tier 1 vendors get comprehensive assessments with extensive evidence requirements and annual reassessment cycles. Tier 3 vendors may need only a lightweight questionnaire every 18–24 months.

Applying the same full assessment to every vendor is one of the most common program failures — it burns resources without improving security outcomes.

One practical trigger list from Tyson Martin's advisory practice: if a vendor has production access, stores employee or customer data, processes payments, supports business-critical operations, or whose failure would create a compliance violation — that's a Tier 1 conversation.

Step 2: Gather Evidence and Issue the Questionnaire

Primary evidence-gathering methods:

- Security questionnaires — NIST CSF-aligned, SIG Lite/Core, or custom frameworks calibrated to vendor tier

- Third-party audit reports — SOC 2 Type II, ISO 27001 certification, penetration test summaries

- Direct documentation requests — business continuity plans, incident response procedures, sub-processor lists

Questionnaire responses are self-reported. They must be validated against independent evidence. A current SOC 2 Type II report provides stronger assurance than a vendor attestation form.

Flag stale documentation as a finding in itself. Audit reports older than 12–18 months may not reflect current controls. SOC 2 reports are generally considered valid for 12 months — anything beyond that warrants a direct inquiry.

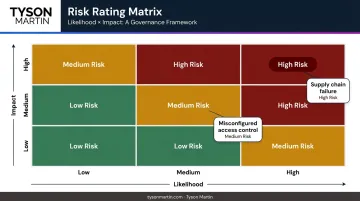

Step 3: Evaluate, Score, and Document Findings

Evaluate each identified gap or risk on two dimensions:

- Likelihood — how probable is exploitation or failure in the next 12 months?

- Impact — what is the business consequence if it occurs?

That combination produces a risk rating (high, medium, low) that drives prioritization. A misconfigured access control with high likelihood but limited blast radius ranks very differently from a low-probability supply chain failure that could halt operations for a week.

Document the assessment methodology explicitly. Regulators and auditors want to see not just findings, but the process used to reach them — documented scope, evidence reviewed, assessor qualifications, and the rationale behind each risk rating.

Treat the methodology record as part of the deliverable, not an afterthought.

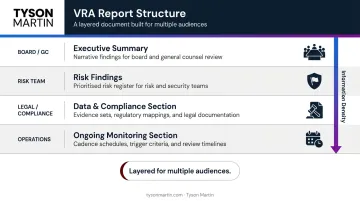

Key Components of a Vendor Risk Assessment Report

The VRA report is the formal output of the process. It needs to serve multiple audiences — technical teams, risk and compliance stakeholders, and executive leadership — which means layering information from summary to detail.

Executive Summary

One page, non-technical. It should state:

- The vendor's business function

- Assessment scope

- Top three to five findings

- Recommended course of action

If a board member or general counsel cannot understand the situation in two minutes, the summary needs revision. That readability is a governance requirement, not a courtesy. Board-ready vendor reporting pairs every top risk with a clear decision path: accept, reduce, transfer, or replace — each with a named owner.

Risk Findings Section

Each finding should include:

- A plain-language description of the issue

- Risk rating (high/medium/low) with rationale

- Why it matters to the business in business terms

- The affected control or obligation

- A specific, measurable remediation recommendation with an accountable owner and deadline

Vague findings like "vendor should improve patching" are not actionable. A useful finding states what was observed, what the exposure is, and who is responsible for closing it by when.

Data and Compliance Section

Document:

- What data the vendor will access, process, or store — classified by sensitivity

- How the vendor protects that data

- Which regulatory requirements apply (HIPAA, PCI DSS, GDPR, CCPA, etc.)

This section gives legal and compliance teams what they need to structure contractual protections. Breach notice windows, audit rights, subprocessor transparency, and recovery objectives aligned with your business continuity tolerance all belong here.

Ongoing Monitoring Section

A VRA report that stops at a point-in-time finding has a short shelf life. It specifies:

- Reassessment schedule by tier

- Triggers for unplanned reassessment (major vendor changes, incidents, M&A activity)

- Metrics tracked between formal reviews

This converts the report from a snapshot into a living governance document. Without it, the assessment sits in a folder until something breaks.

How Boards and Executives Should Oversee Vendor Risk Assessments

The Board's Specific Accountability

Boards do not conduct assessments. Their role is to ensure a credible program exists and that material vendor risks reach the right level of authority at the right time.

Board-level decisions include:

- Approving risk appetite and defining what "in tolerance" means for critical vendors

- Funding risk reduction initiatives when exposure is real and time-bound

- Approving exceptions when the business accepts risk for speed or cost

- Deciding when to exit a vendor or pause a rollout

- Setting accountability frameworks — who owns remediation, who can grant extensions

Management owns:

- Day-to-day vendor processes and questionnaire execution

- Remediation tracking and vendor communication

- Operational monitoring between formal assessments

When decision rights aren't explicit, vendor risk findings either get escalated to the board unnecessarily or never reach them at all.

What Meaningful Board Reporting Looks Like

Boards should not receive a spreadsheet of every vendor finding. Effective vendor risk reporting fits in one to two pages or two to four slides and stays consistent from quarter to quarter so boards can spot drift.

A well-structured dashboard includes:

- Coverage and exposure — total critical vendors in scope, how many are out of tolerance, concentration risk (top five vendors by business impact)

- Trend indicators — new critical vendors added, vendors that improved or degraded with drivers, major open actions with owners and due dates

- A "Decisions requested" box — one to three items with options, cost ranges, and a recommended path

Martin's advisory practice recommends keeping the critical vendor tier small — typically 10 to 30 vendors. If the "critical" list contains 120 vendors, it's a catalog, not a tier.

Separate "risk level" from "confidence" in the reporting. The board should know when data is thin or stale — a vendor rated medium-risk based on a two-year-old SOC 2 report is a very different situation than one rated medium-risk based on current evidence.

The Value of Independent Oversight

Organizations navigating complex vendor ecosystems — particularly those in regulated industries or going through M&A — should consider bringing in an independent board advisor or fractional CISO to validate the program's governance structure. An internal CISO is accountable for delivery; an independent advisor provides unbiased challenge and board-ready framing — those are structurally different roles.

That separation matters most in vendor risk governance, where operational pressures and commercial relationships can quietly narrow what internal teams are willing to flag. An independent advisor can assess:

- Concentration risk without a stake in the vendor relationships

- Contract gaps without pressure to preserve existing agreements

- Remediation progress without the internal politics that slow escalation

In M&A specifically, inherited vendor relationships often aren't visible until after close. By then, unknown risks have become acquired risks.

Frequently Asked Questions

How is a vendor risk assessment different from third-party risk management?

TPRM is the overall framework covering the full vendor lifecycle: selection, contracting, monitoring, and offboarding. A vendor risk assessment is the structured evaluation activity within that program — used to document risk for a specific vendor at a specific point in time.

How often should vendor risk assessments be conducted?

Frequency should match vendor risk tier. Critical or high-risk vendors typically require annual formal assessments with continuous monitoring between cycles. Lower-risk vendors may be assessed every 18–24 months, supplemented by trigger-based reviews after significant vendor changes or incidents.

What is the difference between inherent risk and residual risk in vendor assessments?

Inherent risk is the level of risk a vendor relationship carries before any controls are applied. Residual risk is what remains after the vendor's security controls and contractual protections are accounted for. Residual risk is what organizations should compare against their defined risk appetite.

What regulatory frameworks require vendor risk assessments?

Several major frameworks mandate or strongly recommend VRAs, including HIPAA, PCI DSS, SOC 2, NIST CSF, and OCC/FFIEC for financial services. Organizations subject to GDPR must also assess data processors under Article 28.

What are the most common mistakes organizations make in vendor risk assessments?

The most common failure modes are applying one-size-fits-all assessments regardless of vendor risk tier, treating questionnaire responses as sufficient without independent validation, and producing vendor catalogs instead of decision-ready findings. All three undermine the program's value to leadership.

How should boards oversee vendor risk without getting lost in technical detail?

Boards should set risk appetite and demand aggregate, trend-based reporting rather than vendor-by-vendor technical detail. The right board report shows whether critical vendor risk is within acceptable bounds, which findings are overdue for remediation, and what decisions require board-level authorization versus management delegation.