The cost of getting this wrong is steep. IBM's 2024 breach cost data puts the global average at $4.88M per incident, with financial services breaches averaging $6.08M.

This guide is written for boards, C-suite executives, general counsel, and audit committees—not just compliance teams. Decisions about which vendors to trust, under what conditions, and how to monitor ongoing risk are governance decisions. This guide covers what SOC 2 vendor risk assessments actually measure, what executives must check in a vendor's report, where most organizations go wrong, and how to build this into a repeatable governance cycle.

Key Takeaways

- A SOC 2 report is an independent audit of a vendor's security controls—receiving one does not mean the vendor is low risk

- SOC 2 Type II reports are far more meaningful for vendor due diligence than Type I snapshot assessments

- Executives and boards must check the auditor's opinion, scope, control exceptions, and Complementary User Entity Controls—not just that a report exists

- The most dangerous mistake: accepting a data-center-level SOC 2 as evidence of company-wide security posture

- SOC 2 vendor risk assessment belongs in a recurring governance cycle tied to contract renewals and annual reviews, not a one-time onboarding checkbox

What Is a SOC 2 Vendor Risk Assessment—and Why It Belongs in Your Governance Program

A vendor risk assessment evaluates whether a third party has adequate security controls, operational practices, and compliance posture before—and after—you entrust them with sensitive data or critical business functions. A vendor questionnaire is self-reported and unverified. A SOC 2 assessment is not.

What Makes SOC 2 the Right Lens

SOC 2 (System and Organization Controls 2) is a framework developed by the AICPA requiring an independent, licensed auditor to verify whether a vendor's controls actually work. It focuses directly on data security, availability, and operational integrity, unlike SOC 1, which addresses financial reporting controls.

The three report types differ significantly:

| Report Type | What It Covers | Usefulness for Vendor Due Diligence |

|---|---|---|

| SOC 1 | Financial reporting controls | Out of scope for security assessment |

| SOC 2 | Security, availability, processing integrity, confidentiality, privacy | Core evidence standard |

| SOC 3 | Same subject matter as SOC 2, public-facing summary | Limited—lacks detailed testing results |

Why This Is a Governance Responsibility

When a vendor handling your customer data suffers a breach, the regulatory and reputational consequences fall on your organization. The interagency Third-Party Risk Management guide issued by OCC/FRB/FDIC in May 2024 explicitly states that boards are ultimately responsible for oversight of third-party risk management and holding management accountable.

The Federal Reserve's June 2024 enforcement action against Evolve Bank & Trust cited an ineffective risk-management framework for fintech partnerships as a primary deficiency. It is a named precedent every board and audit committee should have on record.

The Five Risk Categories Every Vendor SOC 2 Assessment Covers

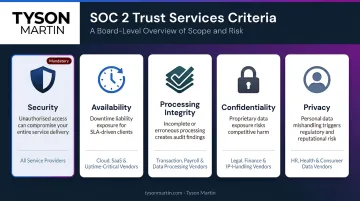

SOC 2 assessments are structured around five Trust Services Criteria (TSC) established by the AICPA. Security is mandatory. The other four are optional, included based on the vendor's service scope. Think of these as business risk dimensions, not technical categories.

The Five Criteria at a Glance

- Security (mandatory): Protects systems and data from unauthorized access — logical access controls, encryption, intrusion detection, and vulnerability management. Every SOC 2 report must include this criterion.

- Availability: Confirms systems are available as committed. Critical for vendors running mission-critical platforms, cloud infrastructure, or payment processing — an availability gap causes operational disruption even without a breach.

- Processing Integrity: Verifies data is processed accurately, completely, and without unauthorized modification. Relevant for financial transactions, data analytics, and healthcare record management.

- Confidentiality: Confirms data designated as confidential is protected throughout its lifecycle — in transit, at rest, and at disposition. Applies to any vendor with access to proprietary or non-public information.

- Privacy: Validates that the vendor's handling of personally identifiable information aligns with your obligations under GDPR, CCPA, or HIPAA. Priority criterion for healthcare, fintech, and retail vendors.

Vendor Tiering: The Prerequisite Decision

Before requesting a SOC 2 report, your organization needs a tiering system. A practical framework classifies vendors by three criteria:

- Service criticality: Would this vendor's failure stop sales, operations, or patient care?

- Data sensitivity — Does the vendor store, process, or transmit regulated or high-value data?

- Concentration risk: Single point of failure, or the only realistic option in that category?

Aim for 10 to 30 vendors at the top tier — that's the range where board-level visibility stays manageable. The TSC criteria you require should correspond to that tier assignment and the data the vendor touches. A payroll processor warrants Security, Confidentiality, and Privacy. A design tool with no sensitive exports needs Security alone. Getting that scoping decision right upfront saves significant back-and-forth when reports arrive.

How to Read a Vendor SOC 2 Report: What Executives and Boards Need to Check

Most organizations confirm a SOC 2 report exists and move on. That approach misses where the actual risk lives.

Step 1: Check the Type and Coverage Period—Always Request Type II

A SOC 2 Type I report confirms controls existed on a specific date. A Type II report evaluates how those controls performed over a sustained period—typically 6 to 12 months. For vendor due diligence, Type I provides minimal assurance. Type II is the meaningful standard.

Also check the report's date. A report more than 12 months old should prompt a request for an updated one. Control environments change; a stale report may not reflect current reality.

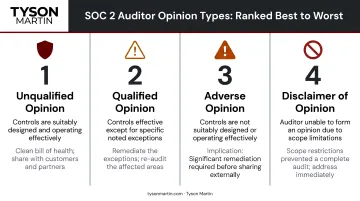

Step 2: Assess the Auditor's Opinion

The Independent Service Auditor's Report contains the opinion. Four outcomes are possible:

| Opinion Type | What It Means |

|---|---|

| Unqualified | No material issues found—the best outcome |

| Qualified | "Except for" language indicating at least one control failure |

| Adverse | Controls materially failed |

| Disclaimer | Auditor could not form an opinion |

A qualified opinion is not automatically disqualifying, but it requires documented follow-up. Your team should confirm:

- What the specific finding was and its business impact

- Whether the vendor has remediated it and when

- Whether your organization's risk threshold policy covers this scenario—and who approves exceptions

Build that policy before you need it.

Step 3: Verify the Report Scope Matches Your Actual Relationship

An often-skipped step: confirm that the systems and services in the SOC 2's System Description actually cover what your organization uses. If the vendor hosts your data in a cloud environment not mentioned in scope—or if a business unit you rely on is excluded—the report provides no assurance for your real exposure.

Before accepting a report as valid, verify:

- The specific services your organization uses are listed in the System Description

- The data environments where your data resides are in scope

- Any third-party subprocessors the vendor uses are addressed

Step 4: Scrutinize Control Testing Results—Exceptions Are Where the Risk Lives

Section 4 of the SOC 2 contains detailed control testing results, including any exceptions or deviations the auditor found. Boards should confirm their teams are reviewing this section—not just the auditor's summary opinion.

For each exception, evaluate:

- Severity and business impact

- Whether it has been remediated

- Whether the vendor's management response provides credible corrective action with a timeline

Step 5: Review Complementary User Entity Controls (CUECs)

CUECs are the security controls your organization is expected to have in place for the vendor's controls to work as designed. If the vendor assumes you enforce multi-factor authentication or restrict third-party access, and your organization doesn't, the SOC 2 provides false assurance.

Your team should review and confirm CUECs during vendor onboarding. Specifically:

- Map each CUEC requirement against your existing controls

- Document gaps and assign remediation owners

- Include CUEC compliance in your ongoing vendor review cadence

Finding a gap after a breach is far more expensive than finding it on day one.

The Most Dangerous Mistakes in SOC 2 Vendor Due Diligence

Confusing a Data-Center SOC 2 for a Company-Wide SOC 2

Many vendors provide a SOC 2 report from their hosting provider—AWS, Azure, or a colocation facility—instead of their own company-level report. The data center report confirms the infrastructure is secure. It says nothing about the vendor's own employees who access your data, their internal governance, their subcontractors, or their incident response processes.

Boards need to insist on the vendor's own SOC 2, not just the infrastructure provider's.

Treating SOC 2 Review as a One-Time Onboarding Checkbox

Accepting a SOC 2 report at the start of a vendor relationship and not reviewing it again for three or four years is a governance failure. SOC 2 reports are annual. New services, acquisitions, cloud migrations, and staffing changes can introduce risks that weren't present when the original report was issued.

The right question for boards is: what is the cycle for re-reviewing critical vendor SOC 2 reports—and is it documented and inspectable?

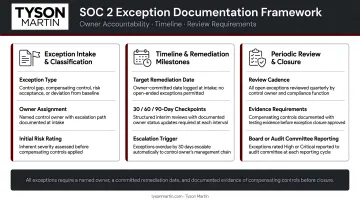

Ignoring Exceptions Without Documented Rationale

Accepting vendors with qualified opinions or control exceptions without documenting why the risk was accepted, by whom, and under what conditions creates gaps that are difficult to defend in regulatory examinations.

Every accepted exception requires:

- A documented risk acceptance decision with a named owner

- A remediation timeline with a defined end date

- A scheduled review before that date — exceptions without expiration dates tend to become permanent

Missing Fourth-Party Risk Through Carved-Out Subservice Organizations

SOC 2 reports often reference subservice organizations—third parties the vendor itself relies on. They appear in two ways: inclusive (the subservice organization's controls are tested within the report) or carved out (explicitly excluded from testing).

When critical subservice organizations are carved out, your organization inherits fourth-party risk the SOC 2 does not address. Your team must conduct additional due diligence—requesting the subservice organization's own certifications or independent assessments.

Building SOC 2 Vendor Risk Assessment into Your Governance Cycle

Establish a Review Schedule with Defined Escalation Thresholds

Effective governance requires a documented policy defining review frequency by vendor tier and clear escalation thresholds—what types of findings, opinion types, or scope gaps automatically escalate to the CISO, General Counsel, or board audit committee.

A reasonable starting framework:

- Critical vendors: SOC 2 review annually, aligned with report period

- High-risk vendors: Review every 24 months or upon contract renewal

- Medium/low risk: Upon contract renewal or material change

Organizations without a dedicated CISO often benefit from engaging a fractional CISO to design and operationalize this framework. The governance cycle needs to be inspectable—which means documented, assigned, and consistently executed.

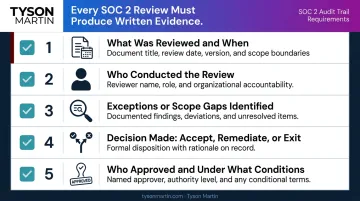

Create a Documented Review Process That Produces an Audit Trail

Every SOC 2 review should produce written evidence:

- What was reviewed and when

- Who conducted the review

- What exceptions or scope gaps were identified

- What decision was made: accept, remediate, or exit the relationship

- Who approved the decision and under what conditions

This documentation serves two purposes. It protects the organization in regulatory examinations. And it gives the board the trend-based reporting it needs to exercise oversight rather than simply receive status updates.

Integrate Findings into Board and Executive Risk Reporting

Vendor risk findings should not stay inside the compliance or procurement function. Critical vendor SOC 2 exceptions, changes in auditor opinion, or vendors that can no longer produce a current report are governance-level signals.

The distinction matters. A board that receives a vendor risk "status" is being informed. A board that sees trend data, exception counts, remediation timelines, and named decision owners is exercising defensible governance.

When regulators examine board oversight, they look for evidence of the second posture. Build your reporting to show it:

- Trend data across vendor tiers, not point-in-time snapshots

- Exception counts with remediation status and target close dates

- Named decision owners for accepted risks and open exceptions

When SOC 2 Alone Isn't Enough

SOC 2 reports do not assess a vendor's financial stability, full incident history, physical security at non-data-center locations, employee background check practices, or fourth-party exposure beyond what is disclosed. For critical vendors, SOC 2 should be supplemented with:

- Security questionnaires (SIG Lite or CAIQ)

- Continuous monitoring tools

- Financial due diligence

- Contractual breach notification windows (measured in hours, not "reasonable time")

- Audit rights and subprocessor transparency requirements

That supplemental rigor matters most when the vendor category itself is outpacing the frameworks designed to govern it. AI vendors are the clearest example right now.

The AI Vendor Gap

As organizations rely on AI-powered vendors for data processing, analytics, fraud detection, and customer interaction, a governance gap is widening.

ISACA's 2024 research across 3,270 digital trust professionals found that only **15% of organizations had formal AI policies**, while 70% reported staff were already using AI tools.

Many AI vendors don't yet have mature SOC 2 programs, and AI-specific controls often fall outside the traditional Trust Services Criteria scope. Boards and risk leaders should be asking AI vendors directly about:

- Data training practices and whether your data is used to train models

- Model access controls and output integrity validation

- Alignment with emerging frameworks such as NIST AI RMF or ISO/IEC 42001

- Fallback plans and rollback criteria if model performance degrades

A standard SOC 2 won't answer any of these questions. Build them into your vendor intake process and require written responses — not acknowledgments, but specifics you can verify at renewal.

Frequently Asked Questions

What is a vendor risk assessment and why is it needed for vendor qualification?

A vendor risk assessment evaluates whether a third party has adequate security controls and compliance posture before being entrusted with sensitive data or critical business functions. Regulatory frameworks hold organizations accountable for the risks their vendors introduce—regardless of where the failure originates.

What factors and criteria are used to assess and rate vendor cybersecurity and overall vendor risk?

Key criteria include data sensitivity, operational criticality, concentration risk, SOC 2 Trust Services Criteria coverage, auditor opinion type, control exceptions, and remediation track record. Tier assignment then determines the evidence standard required: Type II SOC 2, ISO 27001, or supplementary assessments for higher-risk vendors.

What is the difference between a qualified and an unqualified SOC report?

An unqualified opinion means the auditor found no material issues with the vendor's controls. A qualified opinion contains "except for" language indicating at least one control failed or was not operating effectively. A qualified opinion doesn't automatically disqualify a vendor, but it requires documented follow-up, remediation timelines, and a formal risk acceptance decision.

What is a SOC report from a vendor?

A vendor SOC report is an independent audit by a licensed CPA firm that evaluates the effectiveness of a vendor's internal controls over data security, availability, and operational integrity—providing third-party assurance in place of the vendor's self-reported claims.

Is SOC 2 a risk assessment?

No. SOC 2 is an independent audit that validates whether a vendor's controls are designed and operating effectively. A vendor risk assessment uses the SOC 2 report as one input—alongside questionnaires, contractual review, and continuous monitoring—to form an overall risk rating and governance decision.

What are the main risk categories in vendor risk assessments?

Core categories include cybersecurity, operational and availability risk, regulatory compliance, financial continuity, fourth-party supply chain risk, and privacy. SOC 2 addresses the first three through the Trust Services Criteria; the rest require supplementary due diligence.