Introduction

Your organization receives a vendor's SOC 2 report. Someone files it. The compliance checkbox gets ticked. And then — nothing.

That pattern is more common than most risk programs would like to admit, and it creates a specific kind of exposure: the kind that looks defensible until a vendor suffers a control failure and regulators ask what oversight actually existed.

A filed-but-unread SOC 2 report is not a defensible answer.

This article gives boards, audit committees, and risk leaders a practical framework for extracting real risk intelligence from SOC 2 reports — one built on analysis, not collection. You'll learn what the report actually tells you and what it doesn't. You'll also see how to read the signals that matter and connect SOC 2 review to a governance program that holds up under scrutiny.

That governance standard matters more now than it did two years ago. The SEC's 2023 cybersecurity disclosure rules require public companies to describe their processes for managing third-party cybersecurity risks and disclose board oversight. Passive report collection doesn't satisfy that requirement.

Key Takeaways

- SOC 2 is an independent auditor examination of vendor controls — not a certification, and not a guarantee of security

- The auditor's opinion type (unqualified vs. modified) is your first and most important signal

- Scope alignment matters: a SOC 2 covering the wrong systems offers you nothing

- Complementary User Entity Controls (CUECs) create obligations on your side that most organizations overlook

- SOC 2 review should produce documented findings, not a filed PDF

What Is a SOC 2 Report and Why It Matters

A SOC 2 (System and Organization Controls 2) report is the result of an independent examination conducted by a licensed CPA firm. Per the AICPA's SOC suite of services, it assesses whether a service organization's controls are designed and operating effectively across one or more of five Trust Services Criteria: Security, Availability, Processing Integrity, Confidentiality, and Privacy.

For organizations outsourcing data handling, cloud infrastructure, payment processing, or other sensitive functions, SOC 2 provides third-party validation that controls have been tested by an independent auditor. Vendors don't self-report; a licensed auditor does.

What SOC 2 Is Not

Three things organizations consistently get wrong:

- It is not a certification. SOC 2 is an attestation examination. There is no AICPA "SOC 2 certified" designation.

- It is not a guarantee. The report reflects a control environment at a point in time (Type I) or over a defined period (Type II). Controls can change after the report closes.

- A report in hand is not due diligence complete. The 2023 interagency guidance from the Federal Reserve, FDIC, and OCC treats SOC reports as one input into documented third-party risk management, not a substitute for it.

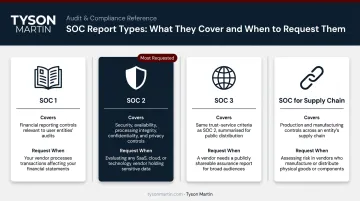

SOC Report Types at a Glance

| Report Type | What It Covers | When You'd Request It |

|---|---|---|

| SOC 1 | Controls relevant to financial reporting | Vendors affecting your financial statements |

| SOC 2 | Security, availability, confidentiality, processing integrity, privacy | Technology and data service vendors |

| SOC 3 | Same criteria as SOC 2, public-facing | General awareness only — less detail |

| SOC for Supply Chain | Production, manufacturing, distribution controls | Supply chain risk exposure |

Once you've confirmed which report type applies, the next question is how to actually read it — and what to do when the findings raise concerns.

SOC 2 Type I vs. Type II: What the Difference Means for Your Assessment

Most vendor questionnaires treat Type I and Type II as equivalent checkboxes. They aren't.

Type I assesses whether controls were suitably designed at a single point in time. It answers: "Did the controls exist and look reasonable on the audit date?" It does not show whether controls worked in practice over any period of time.

Type II assesses whether controls were designed and operated effectively over a defined period. KPMG describes a Type II examination as assessing whether controls operated effectively over a period of time. Enterprise procurement and audit teams should require Type II for any critical vendor — it's the only report that shows controls actually worked, not just that they existed on paper.

When Type I Is Acceptable

Type I isn't worthless — it's appropriate in specific situations:

- A newer vendor that doesn't yet have a 12-month operating history for Type II

- Early-stage due diligence before committing to a deeper relationship

- Non-critical vendors with limited data access

For vendors handling sensitive data, regulated information, or core infrastructure, accept Type I only as a bridge while requiring Type II on the next cycle. Document that expectation in writing — it creates the contract leverage and audit trail you'll need if the vendor stalls on completing a Type II.

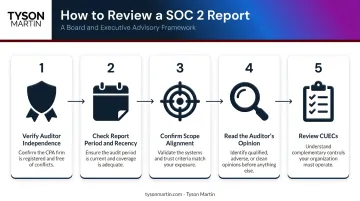

How to Read a Vendor's SOC 2 Report: Five Checks That Matter

Most teams skim SOC 2 reports looking for a green light. The more useful approach is systematic — five specific checks that produce actionable information.

Step 1: Verify Auditor Independence and Qualifications

The report must come from a licensed CPA firm. Credentials like CISA or CISSP on the engagement team signal relevant IT audit expertise. Auditor quality varies — firms with limited SOC 2 experience often rely on small sample sizes and weak evidence standards, which means findings can be incomplete even when the opinion looks clean.

Step 2: Check the Report Period and Recency

Find the "as of" date (Type I) or the coverage period (Type II). A report more than 12 months old should prompt a direct conversation with the vendor. Request either the current report or a bridge letter confirming no material control changes since the last report period closed.

Step 3: Confirm Scope Alignment With Your Use Case

Read the system description. Confirm that the systems, data environments, and services covered in the report are the same ones your vendor provides to your organization. A SOC 2 covering a different product line or infrastructure segment than what you actually use offers no meaningful assurance for your situation.

Step 4: Read the Auditor's Opinion

This is where the real work happens. Four opinion types matter:

- Unqualified — controls met the stated criteria; the preferred outcome

- Qualified — material issues exist but aren't pervasive; "except for" language signals specific control failures that need documented evaluation before proceeding

- Adverse — failures are both material and pervasive; treat this as a hard stop on vendor engagement until remediation is confirmed

- Disclaimer — the auditor couldn't obtain sufficient evidence to form an opinion; a significant risk signal regardless of the vendor's explanation

"Qualified" does not mean "good." Many recipients misread it as a passing grade. It is not.

Step 5: Review Complementary User Entity Controls (CUECs)

CUECs are the controls your organization must have in place for the vendor's controls to work as intended. Per AICPA guidance on AU-C 9402, these are controls the service organization assumes you will implement — they are your responsibility, not the vendor's.

If your organization hasn't implemented the required CUECs, a control gap exists. It won't appear anywhere in the vendor's report. It will, however, appear in your own audit exposure.

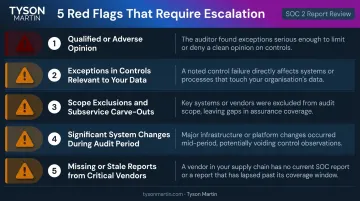

Red Flags That Should Prompt Escalation

Not every issue in a SOC 2 report carries equal weight. These five warrant formal escalation and documented response.

Flag 1: Qualified or Adverse Opinions

A qualified opinion means the auditor found a material deficiency that isn't pervasive — and that's not a minor finding. Your risk team needs to identify which controls were deficient and whether those controls protect the systems or data you actually depend on from that vendor.

An adverse opinion is rare and should be treated as a near-automatic pause on the relationship until remediation is confirmed.

Flag 2: Exceptions in Controls Relevant to Your Data

Not every exception matters equally. A deviation in vendor change-management scheduling procedures is different from exceptions in:

- Access controls and provisioning

- Encryption in transit and at rest

- Incident detection and response

- Backup and recovery procedures

Map exceptions to your specific exposure. If the vendor processes payment data for you and there are exceptions in their access control testing, that requires a documented risk response — not just a note that exceptions were observed.

Flag 3: Scope Exclusions and Subservice Carve-Outs

If the vendor's SOC 2 carves out a major subservice provider — say, the cloud platform actually hosting your data — that subservice organization's controls are not covered in the report. Request separate assurance or verify the subservice provider's compliance independently.

Flag 4: Significant System Changes During the Audit Period

The report should disclose major changes: infrastructure migrations, acquisitions, new platforms. These changes can render portions of the control testing less relevant to your current situation. Treat it as a gap if the report lists significant changes but doesn't explain how controls held up during the transition.

Flag 5: Missing or Stale Reports From Critical Vendors

A critical vendor that cannot produce a current SOC 2 report is itself a risk signal. The 2023 interagency banking guidance states that when desired due-diligence information is unavailable, management must document limitations, assess residual risks, and determine whether those risks are acceptable — not treat them as acceptable by default.

Alternative evidence options when SOC 2 is unavailable:

- ISO 27001 certification

- Completed SIG Lite questionnaire

- Recent penetration test results summary

- CAIQ (Consensus Assessments Initiative Questionnaire)

Whatever alternative you accept, document why it's sufficient for this vendor at this risk tier. Each of these five flags represents a decision point — and how your organization responds, and whether that response is documented, is what distinguishes defensible oversight from checkbox compliance.

Beyond the Report: Integrating SOC 2 Reviews Into Vendor Governance

SOC 2 review shouldn't end when someone saves the PDF. It should feed into an ongoing governance process that produces documented evidence of review, follow-through on findings, and risk decisions that hold up when auditors or regulators ask what you did.

What Documented Review Actually Requires

The 2023 interagency guidance is direct: risk management is expected across the full third-party relationship lifecycle — planning, due diligence, ongoing monitoring, and termination. Receiving a SOC 2 report does not complete due diligence. Reviewing it, evaluating findings, and acting on gaps does.

A defensible review process includes:

- Documented confirmation that scope aligns with your use case

- Recorded evaluation of any exceptions and their relevance to your data

- Implementation status of required CUECs

- Dated evidence of who reviewed the report and what decisions followed

A Tiered Review Frequency Model

Not every vendor needs the same depth of review. A workable tier structure:

| Vendor Tier | Criteria | Review Approach |

|---|---|---|

| Critical | Sensitive data, core infrastructure, high business impact | Review upon receipt, track annual renewal, escalate exceptions immediately |

| Medium-risk | Operational dependencies, moderate data exposure | Periodic review aligned to reporting period |

| Low-risk | Limited access, non-sensitive functions | Documented rationale for reduced scrutiny |

Your organization should be able to produce this tiered inventory and evidence of review during an audit. EY's 2023 Global Third-Party Risk Management Survey of 500+ institutions found 90% directly invested in TPRM programs — the governance infrastructure to make SOC 2 review meaningful is the gap many programs still need to close.

Feeding Findings to the Board

SOC 2 exceptions and scope gaps need to reach boards and risk committees in plain English — not as technical details buried in a GRC platform. The relevant questions for a board dashboard:

- Which critical vendors have current SOC 2 reports on file?

- Are there open exceptions in controls relevant to high-risk data?

- Which vendors have missing or overdue reports?

- What CUECs are required, and have we implemented them?

This is where independent advisory support bridges raw findings and board-ready reporting. Tyson Martin's Third-Party & Vendor Risk Reporting service translates a sprawling vendor inventory into a board-level view of concentration, criticality, and exposure. Deliverables include a vendor criticality ranking, a concentration risk report, and a quarterly board update template — giving directors clear, documented answers when regulators or acquirers examine how third-party risk is governed.

When a SOC 2 Report Isn't Enough

SOC 2 is a strong starting point — but it's rarely sufficient on its own.

Regulated Industries Require More

| Sector | What SOC 2 Doesn't Cover |

|---|---|

| Healthcare (HIPAA) | Written Business Associate Agreements defining permitted PHI uses and required safeguards |

| Financial Services (NY DFS) | Written third-party security policies requiring vendors to maintain cybersecurity protections |

| Financial Services (GLBA) | Written information security program, service-provider safeguards by contract, board reporting |

| Government Contracting (CMMC Level 2) | 110 NIST SP 800-171 requirements and formal CMMC assessment/status |

| Federal Cloud (FedRAMP) | Agency-specific FedRAMP authorization for in-scope cloud services |

| Healthcare (HITRUST) | Separate assessment handbook and certification with its own validity period |

Contractual Controls Are Non-Negotiable

The SOC 2 report documents what a vendor does. Contracts define what they're obligated to do. These are not the same thing, and one doesn't substitute for the other.

At minimum, contracts with critical vendors should include:

- Audit rights, or at minimum evidence rights and cooperation language

- Breach notification timelines aligned to your regulatory obligations — OCC rules, for example, require bank service providers to notify a designated contact as soon as possible after incidents degrading covered services for four or more hours

- Data ownership and deletion provisions effective on contract termination

- Subcontractor flow-down requirements and prior-approval rights

These terms function as security governance controls. Treating them as legal boilerplate is one of the more common gaps Tyson Martin surfaces in vendor risk advisory engagements.

High-Risk Vendors May Warrant Direct Assessment

For vendors with access to your most sensitive systems or data, a SOC 2 review alone isn't enough. Supplement it with:

- Targeted security questionnaires focused on your specific risk exposure

- Penetration test executive summaries covering in-scope systems

- Direct attestation on subservice providers carved out of the SOC 2 scope

Frequently Asked Questions

What does a qualified SOC 2 report mean?

A qualified opinion means the auditor found a material deficiency in control design or operation — limited in scope, but real. "Qualified" does not mean high-quality; it means something failed. Identify which controls were deficient and whether they cover the systems or data relevant to your vendor relationship.

What is a vendor SOC 2 report and who provides it?

A vendor SOC 2 report is an independent examination report issued by a licensed CPA firm, documenting whether the vendor's controls meet the AICPA's Trust Services Criteria. The vendor commissions the audit and shares the resulting report (typically under NDA) with customers and prospects who request it as evidence of security and operational controls.

Is a SOC 2 Type I or Type II report better for vendor risk assessment?

Type II is the appropriate standard for meaningful vendor due diligence. It shows controls operated effectively over a defined period, whereas Type I only confirms controls were designed appropriately at a single point in time. For critical vendors handling sensitive data, Type II should be the baseline expectation ; Type I is acceptable only as a temporary bridge.

What should you do if a vendor cannot provide a current SOC 2 report?

Treat it as a meaningful risk indicator. Request alternative evidence such as ISO 27001 certification, a completed SIG Lite, or penetration test results, and document your assessment methodology. Formally accept or escalate the residual risk with a named owner and expiry date.

How often should your organization review a vendor's SOC 2 report?

SOC 2 reports are typically issued annually. For critical vendors, review updated reports upon receipt. At minimum, your review cycle should have no gap in assurance coverage relative to the vendor's reporting period. Significant system changes disclosed in the report (migrations, acquisitions, new infrastructure) should trigger immediate evaluation regardless of the normal review schedule.

Do vendors have to get a SOC 2 report?

No legal mandate requires vendors to obtain a SOC 2 report. Customer demand makes it a commercial expectation for technology and data service providers. If a critical vendor cannot or will not provide one, your organization must conduct alternative due diligence and document why the relationship is acceptable. Formal risk acceptance needs to be on record.