AI Governance for Pre-IPO Companies: What S-1 Diligence Will Ask About Your AI

Preparing for an IPO? Build an S-1 AI risk disclosure with clear ownership, materiality, controls, vendor evidence, and a 90-day plan.

As a pre-IPO leader, you face pressure from every direction. Growth is accelerating, AI use is spreading, and the SEC will expect your claims, controls, and reporting to align with these advancements. Investors now scrutinize how companies manage AI risk disclosures—the formal process of documenting AI-related exposures, dependencies, and governance measures—as part of their broader compliance strategy.

AI may sit inside your product, customer service, hiring, forecasting, security, or internal operations. An S-1 process will test whether you know where it matters and what could fail. Download the AI Boardroom Question Pack if you need sharper questions before the next executive or board discussion.

A credible S-1 AI risk disclosure starts with facts, ownership, and proof.

TLDR

Your AI disclosure should reflect the reality of your AI adoption and how the business operates, rather than how the product is marketed.

Start with an AI inventory that tracks systems, data, vendors, owners, and business impact.

Do not treat an AI policy as a substitute for actual governance. Effective AI governance requires documented decisions, defined limits, rigorous testing, clear escalation paths, and tangible evidence.

The board needs visibility into business exposure, emerging trends, and clear decision requests, not just a count of models or training sessions.

Use a 90-day plan to close the gaps that could slow down diligence or weaken investor confidence.

What S-1 Diligence Will Really Ask About Your AI

An S-1 is not only a financial and product document. Your AI use may affect Item 1A Risk Factors, business descriptions, intellectual property, data privacy, cybersecurity, internal controls, customer commitments, and operating continuity.

The question is not whether your company uses AI responsibly. The question is whether you can support that statement with facts.

AI governance is a repeatable way to make decisions. It assigns ownership, sets limits, tests outcomes, records exceptions, and creates evidence that leaders reviewed the risk. It is not a policy in a shared folder, a committee that meets once without producing decisions, or a vague promise that someone will keep an eye on it.

Use four questions to frame your S-1 AI risk disclosure:

What AI do you use?

What could happen if it fails, changes, or is misused?

Who has authority to approve, limit, or stop it?

What proof supports your answer?

The level of work should match the use case. Scrutiny rises when AI is core to your product, supports material revenue, processes sensitive data, or influences important decisions. Your legal and accounting teams should assess disclosure duties with qualified securities and regulatory counsel. Management still has to build the underlying record, as counsel cannot disclose facts the company has not identified. By treating these disclosures with the same rigor required for 10-K filings, you position your firm to maintain consistent transparency in future Form 10-K filings, thereby reducing potential SEC scrutiny.

Your AI Risk Disclosure Must Match the Business Model

Diligence teams will compare your public language with reality. They may ask about customer-facing models, embedded features, predictive systems, generative AI, internal automation, third-party APIs, and decisions supported by AI outputs.

Avoid the trap of AI-washing, where vague claims create hard questions that you cannot support. If you describe a feature as proprietary AI, can you explain what is actually proprietary regarding your intellectual property? If you call it intelligent automation, can you show its limits, data rights, vendor dependence, and human controls?

Build an AI use register before someone else asks for one. For each meaningful system, record:

System name, business purpose, owner, and users

Data used, vendor involved, and where outputs go

Business criticality and known risks

Human review points, approval status, and next review date

This register is not paperwork for its own sake. It gives executives one version of the truth to manage every material AI risk across the enterprise.

Expect Questions About Materiality, Not Only Accuracy

A model can perform well and still create material exposure. Materiality is about what a failure could mean for revenue, customers, operations, legal exposure, reputation, or the ability to run the business.

Consider an AI recommendation that harms a customer, a model trained on disputed data, a vendor outage that disables a core product feature, or a chatbot that exposes confidential information or compromises your cybersecurity posture. Accuracy is part of the answer, but it is not the whole answer.

Use business consequences rather than false precision. You should be able to state which risks you accept, which require action, and what event would force escalation to identify a material AI risk.

If you cannot explain when an AI risk becomes a board issue, you have not set a useful threshold.

Build an AI Inventory That Survives Investor Review

You cannot govern what you cannot see. That becomes harder when product teams, sales teams, engineers, and employees adopt machine learning tools independently. To succeed in your S-1 filing, your inventory must capture the full scope of machine learning deployments across the enterprise.

Your inventory should cover more than production models. Include experiments that touch sensitive data, employee tools, AI-enabled vendors, data pipelines, prompts, generative AI workflows, training sources, model outputs, and points where people review or override results.

The goal is not to document every low-risk experiment with the same effort. The goal is to find systems that could create material business, customer, legal, or operational harm.

This is where AI governance for better board decisions becomes practical. The inventory gives the board a usable view of where your technology stack matters and where control is thin.

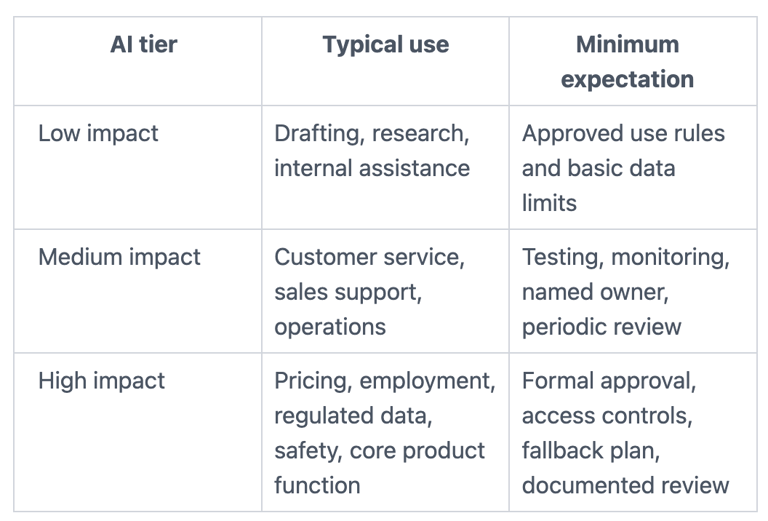

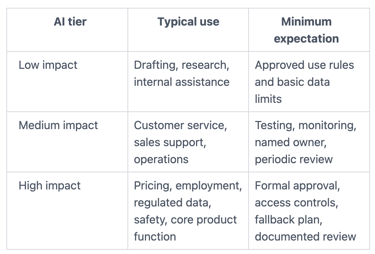

Classify AI by Business Impact and Decision Power

A simple tiering model keeps your effort proportionate.

The more power a system has over people, money, or essential operations, the stronger your evidence should be.

Many companies treat all AI use as equal. That wastes attention on minor tools while high-impact systems move without enough review. A stronger approach puts the most scrutiny where failure would hurt the business.

Trace Data, Vendors, and Intellectual Property

For each important system, you need to know where input data comes from, what happens to it, and who can access the output. That includes customer information, internal records, code, prompts, training data, and generated content. Protecting your intellectual property is essential as you scale these automated systems.

Review vendor contracts for confidentiality, training rights, data retention, deletion, security commitments, incident notice, subcontractors, audit rights, model changes, and exit support. A vendor's AI incident still becomes your customer trust problem.

Keep a short evidence file for each high-impact system. Include contracts, data maps, testing results, approvals, known limits, incidents, and remediation work. Thin evidence should be visible, not hidden.

Create Governance Evidence for S-1 AI Risk Disclosure

Diligence will test whether governance works in practice. A board-approved policy matters less if model changes bypass review, exceptions have no owner, or incidents are handled informally.

Strong governance produces a record of what was decided, why it was decided, who approved it, what evidence supported the decision, and when it will be reviewed again. When preparing your S-1 AI risk disclosure, four evidence areas matter most:

Decision rights: The board provides board oversight for material exposure. Management owns execution. Legal, privacy, security, product, and data teams have defined roles.

Controls: Sensitive data rules, access limits, testing requirements, change approvals, and human oversight fit the system's impact.

Monitoring: Management tracks performance decline, complaints, incidents, vendor changes, exceptions, and unresolved issues.

Reporting: Executives and directors receive a short view of what changed, what remains exposed, and what decision is needed.

Use AI governance questions for management to test whether answers are clear before investors, underwriters, or outside counsel ask the same questions.

Set Decision Rights, Approval Gates, and Escalation Triggers

Named owners should exist for approving a high-impact use case, accepting a known model limitation, allowing sensitive data into a system, changing a production model, responding to an incident, and stopping or rolling back a system.

Escalation triggers should be equally clear. Examples include harmful output, privacy exposure, unexplained performance decline, material vendor changes, regulatory inquiries, customer complaint patterns, or any AI failure that affects financial reporting or a core service.

When nobody can answer who decides, you have activity but not AI governance.

Measure Whether AI Risk Is Moving

Your board dashboard should stay small. Effective board oversight requires reporting the number of high-impact systems with current owners, testing coverage, unresolved exceptions, model performance against agreed thresholds, human review rates, vendor evidence gaps, privacy incidents, customer complaints, and remediation status.

Avoid reports built around model counts, policies completed, or training attendance. Those numbers show work. They do not show exposure.

A useful update answers four questions: What changed? What remains exposed? What is management doing? What decision is needed?

Prepare for AI Incidents and Changing Models

AI can fail through bad output, bad data, model drift, vendor changes, misuse, or an exposed prompt. Your response plan should identify the issue, preserve evidence, limit the system, assess affected customers and data, involve legal and communications, correct the problem, and record lessons learned.

Run at least one tabletop exercise with executives, product, security, privacy, legal, operations, and communications. Test the decision path, not only the technical response.

Cyber and AI oversight must move together because the same weak ownership and thin reporting can undermine both your AI strategy and your broader cybersecurity posture. Ensure your cybersecurity protocols align with AI incident response, as robust cybersecurity is essential for protecting model integrity. By integrating these systems, you demonstrate that your cybersecurity framework is capable of managing the unique risks introduced by machine learning.

Use a 90-Day Plan Before S-1 Diligence

You do not need a year-long compliance project to gain control. You need a focused plan with owners, evidence, and follow-through that anticipates the scrutiny of SEC reviewers.

In the first 30 days, identify AI use, crown-jewel data, critical vendors, material use cases, and missing owners. During this phase, consider how your AI risk disclosures will compare to the standards set by S&P 500 companies. In days 31 through 60, tier the risks, review contracts, approve minimum controls, test high-impact systems, and set escalation rules. This is the time to identify your legal and regulatory risk and ensure your machine learning deployments are defensible.

In days 61 through 90, run an executive tabletop, produce a board-ready report, close the most important evidence gaps, and compare disclosure language with the operating facts. Investors will expect your AI risk disclosures to hold up under the same rigor applied to 10-K filings. Ensure your documentation covers competitive risk and potential reputational risk, as these are increasingly scrutinized by the SEC.

Document accepted risks. Each record should name the owner, reason, expiration date, compensating control, and review trigger. Your mitigation strategies must be concrete; avoid falling back on generic boilerplate language that fails to inform shareholders. See Where Your Board Actually Stands if you need a direct view of whether oversight is working or merely symbolic.

Use a Diligence-Ready AI Evidence Checklist

Your evidence should be current, consistent, and easy for directors, counsel, auditors, investors, and underwriters to inspect. This preparation is essential because your Item 1A Risk Factors will be compared against the historical AI risk disclosures of mature S&P 500 companies.

Keep an approved AI inventory, system owners, business purposes, data and intellectual property maps, vendor contracts, security evidence, testing records, human oversight rules, complaint and incident records, risk exceptions, meeting minutes, training records, change logs, and monitoring metrics.

You also need a clear explanation of how AI risk could affect revenue, customers, operations, cybersecurity, compliance, and reputation. Your board must be prepared to defend these positions in a manner consistent with the disclosures found in a standard Form 10-K.

Know the Warning Signs That Slow Diligence

Red flags are usually simple. Employees cannot identify all AI tools in use. Product claims are stronger than test results. No one owns third-party model risk. Contracts ignore data use or deletion. Risk exceptions have no end date. If underwriters find that your AI risk disclosures are inconsistent with your actual machine learning practices, you face significant legal and regulatory risk.

Other warning signs show up in the boardroom. Directors receive technical detail without business impact. Model changes bypass review. Management handles incidents through informal conversations. Nobody can explain what would cause the company to stop using a system. If you fail to account for societal AI risks or specific competitive risk, you may find your Form 10-K preparation significantly delayed by SEC inquiries.

The stronger alternative is equally simple: evidence, ownership, thresholds, and follow-up. By treating these requirements with the same gravity as your eventual 10-K filings, you build a sustainable foundation.

Frequently Asked Questions About S-1 AI Diligence

What is S-1 AI risk disclosure? It is the formal process of documenting AI-related risks and dependencies that matter to investors. This includes operational, privacy, cybersecurity, and legal and regulatory risk. Much like the disclosures in a Form 10-K, these statements must be precise to avoid claims of AI-washing.

Does every pre-IPO company need formal AI governance? The right level depends on your size and risk profile. However, if your AI use is material, you must be ready for the SEC to treat your disclosures with the same skepticism applied to established S&P 500 companies. Proper governance prepares you for the post-IPO reality of annual 10-K filings.

What if you only use vendor AI? Vendor use does not remove your responsibility. You own customer trust and the business impact of vendor failures. When you transition to a public company, your Item 1A Risk Factors must accurately reflect these third-party dependencies, as seen in the 10-K filings of major S&P 500 companies.

How do international standards like the EU AI Act fit in? If you operate globally, the EU AI Act sets a high bar for compliance. SEC expectations often mirror this rigor. Demonstrating compliance with the EU AI Act early can mitigate reputational risk and simplify your transition to reporting via a Form 10-K.

Are there risks related to AI-washing? Yes. The SEC is increasingly focused on ensuring that AI-related claims in S-1 filings are not misleading. AI-washing can lead to SEC enforcement actions, making it vital that your AI risk disclosures are grounded in verifiable technical evidence and machine learning performance metrics.

What should the board ask before filing? Boards should ask how the company addresses legal and regulatory risk, whether cybersecurity protocols are robust, and how the firm handles societal AI risks. They should ensure that the final Item 1A Risk Factors provide a realistic assessment that would satisfy a 10-K filings audit.

How much documentation is enough? You need enough to prove your claims under the scrutiny of an SEC review. Think of your evidence as the supporting documentation for a future Form 10-K. If you cannot provide clear documentation regarding your competitive risk or cybersecurity posture, you are not ready for public markets. Proper documentation mitigates legal and regulatory risk and prevents the pitfalls common to companies relying on boilerplate language. Consistency between your S-1 and your future 10-K filings is the ultimate goal.

Related Reading

Build the Record Before You Need to Defend It

Strong AI governance is not a claim of zero risk. It is a record that you know where AI matters, set reasonable limits, assign decisions, test what can fail, and keep proof that leadership paid attention.

Your S-1 AI risk disclosure should reflect the reality of your business, including its specific limits and technical dependencies. Because the SEC scrutinizes these filings for material accuracy, ensuring your documentation is audit-ready is critical. If scattered AI activity has outpaced your internal oversight, Get Board-Ready on AI and Cyber Risk before formal diligence turns lingering uncertainty into a much harder problem to solve.

Tyson Martin is the executive public and pre-IPO companies in financial services, AI/data, SaaS, and cloud hire to make trust a measurable asset, one accountable answer to Is it secure? Is it resilient? Is the AI governed?

© 2026. All rights reserved.

Navigation

Free Resources

Contact

Stay ahead of your next board agenda

Sign up for Reports & Learnings From the Boardroom. Plain-English AI and cyber governance insights, biweekly. No pitch.

No spam. Unsubscribe anytime. · Or download the Director's AI Question Pack — 25 questions free