Introduction

Most BFSI boards have approved AI strategies. Far fewer can answer a simple question from an examiner: When was your highest-risk credit model last independently validated?

That gap is no longer a governance footnote. AI models now drive credit underwriting, fraud detection, AML screening, and customer pricing at institutions of every size. When those models produce wrong outputs — or operate outside their approved scope — the consequences extend well beyond operational inconvenience into financial loss, regulatory penalty, and reputational harm.

Regulators responded directly to that risk. On April 17, 2026, the Fed, OCC, and FDIC issued revised model risk guidance, updating the SR 11-7 baseline that has governed MRM for over a decade. They are no longer issuing suggestions — they are issuing frameworks with examination expectations attached.

This post unpacks the current regulatory landscape, the components of a defensible AI model risk management (MRM) framework, and the governance questions boards should be able to answer before approving any new AI deployment.

Key Takeaways

- AI model risk management is a board accountability issue in 2026, not a back-office function

- A sound AI MRM framework rests on four pillars: model inventory and risk classification, lifecycle governance, independent validation, and third-party/vendor risk

- Generative AI and agentic systems carry risks traditional MRM frameworks weren't built for. Boards need updated policies now.

- The most common governance failure isn't having the wrong controls — it's having controls that can't be inspected or reported to the board in plain language

Why AI Model Risk Is Now a Board-Level Problem

The Stakes Have Changed

AI models in BFSI have moved from pilots to core infrastructure. According to PwC's 2024 MRM survey, 70% of financial institutions had already integrated AI-driven models into operations. The FSB projects financial-services AI investment will reach $400 billion by 2027, up from $166 billion in 2023.

That scale matters because model risk — the risk that a model produces wrong outputs, is misused, or is deployed without adequate controls — has always existed in banking. What's changed is the amplification. AI and ML models introduce:

- Opacity: outputs that can't be fully explained even by their developers

- Drift: performance degradation as real-world data diverges from training data

- Autonomous behavior: decisions made at speed and scale without human review

Traditional validation methods weren't designed to catch any of these reliably.

The Misconception That Creates Liability

Governance structure, decision rights, and escalation thresholds are board responsibilities — not something to delegate to the CTO or CRO. Boards that treat AI governance as a technology problem expose themselves the moment a regulator asks who owns it.

OSFI E-23 (effective May 2027) explicitly requires senior management to define roles and accountabilities and ensure appropriate reporting of model risk to the board. US MRM guidance places governance, policies, and controls within the bank's MRM framework expectations — not within the data science team's remit. Boards that cannot demonstrate active oversight of AI model risk are exposed in regulatory examinations, regardless of how sophisticated their models are.

Rapid AI adoption routinely outpaces the controls meant to govern it. Boards should ask for a model inventory and validation status report before approving any AI scale-up.

The Regulatory Wave Reshaping BFSI in 2026

The US Baseline Has Been Updated

SR 11-7 has governed model risk management for US banks for over a decade. In April 2026, the Fed, OCC, and FDIC issued revised model risk guidance that updates that baseline while preserving its core requirements: independent validation, model inventory, and governance proportional to model complexity.

For community banks specifically, OCC Bulletin 2025-26 (October 2025) gives institutions flexibility to scale MRM requirements to their risk profile, size, and model use. It clarifies that validation frequency is not prescriptively annual. What it does not do is eliminate the governance obligation — smaller banks still need a risk-based rationale for their validation scope and cadence.

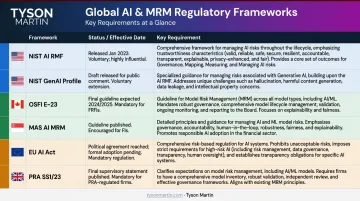

The Global Frameworks US Institutions Can't Ignore

| Framework | Status | Key Requirement |

|---|---|---|

| NIST AI RMF | 2023, voluntary but de facto benchmark | Govern, Map, Measure, Manage functions |

| NIST GenAI Profile (AI 600-1) | 2024 | GenAI-specific controls mapped to AI RMF |

| OSFI E-23 | Effective May 1, 2027 | Enterprise-wide MRM; explicitly includes AI/ML |

| MAS AI MRM | December 2024 | Covers governance, risk processes, GenAI |

| EU AI Act | In force August 2024 | Creditworthiness AI classified as high-risk |

| PRA SS1/23 | May 2023 | Model inventory, tiering, independent validation |

Cross-border institutions and correspondent banking relationships mean these frameworks set expectations for US firms regardless of where they are chartered. The EU AI Act's classification of creditworthiness AI as high-risk, for example, affects any institution with EU-facing credit operations.

Principles-Based Doesn't Mean Optional

Most of these frameworks prescribe outcomes, not specific tools. Boards must be able to demonstrate governance across the full model risk lifecycle. Principles-based language shifts the burden onto the institution: if your framework can't answer the regulator's questions, the ambiguity works against you, not for you.

Specifically, boards need to show evidence that model risk is:

- Identified and inventoried across the enterprise

- Assessed with documented methodology and proportional scrutiny

- Managed with clear ownership and escalation paths

- Monitored on a defined cadence tied to model complexity

- Reported to the board with enough context to act

What an AI Model Risk Management Framework Must Cover

Model Inventory and Risk Classification

The starting point is a comprehensive, evergreen model inventory covering every AI/ML model in production — including vendor and third-party models. Per OSFI E-23 and MAS guidance, the inventory should capture model purpose, inputs, risk rating, owner, last review date, and approved use. Without it, a board cannot know its actual AI exposure.

Risk tiering is not optional. Not every model needs the same governance intensity. A tiered approach — based on model complexity, autonomy level, customer impact, and financial materiality — lets institutions concentrate governance resources on genuinely high-risk models:

- High risk: Credit decisioning, fraud detection, AML screening, customer pricing

- Medium risk: Internal forecasting, operational models with limited customer impact

- Lower risk: Analytical tools, internal reporting models

Lifecycle Governance: Design Through Decommission

Both OSFI E-23 and MAS identify five stages requiring documented accountability:

- Design — rationale, data sourcing, development methodology, named owner

- Independent review — validation before production deployment

- Deployment — change controls, production testing, approved scope

- Monitoring — drift detection, performance thresholds, automated alerts

- Decommission — formal retirement with fallback procedures

The decommission stage is where most institutions have genuine exposure. Deploying models is a structured process at most banks. Retiring them often isn't. Legacy models still influencing decisions without current validation represent a governance gap that rarely appears on a board's radar until an examination finds it.

Independent Validation and Continuous Monitoring

Model validation must be independent of model development — this is a core expectation across SR 11-7, OSFI E-23, and PRA SS1/23. For AI/ML models, validation must go beyond conceptual soundness and data quality. It needs to include:

- Testing for bias in model outputs across demographic groups

- Drift analysis comparing current performance against development benchmarks

- Robustness testing under adverse or stressed conditions

- Explainability assessment — can the model's decisions be justified to a regulator?

Ongoing monitoring should include automated alerts when model performance degrades past defined thresholds. Examiners under SR 11-7 and OSFI E-23 increasingly expect evidence of continuous monitoring cadence — not just a point-in-time validation report from the prior year's review cycle.

Third-Party and Vendor Model Risk

Many institutions are deploying AI through vendors, cloud platforms, and embedded third-party models. OCC third-party guidance and OSFI B-10 are clear: using a third party does not transfer governance responsibility. Institutions must treat vendor models with the same rigor as internally developed models.

That means:

- Due diligence on vendor model documentation before deployment

- Audit rights negotiated into vendor contracts — not assumed

- Concentration risk assessment — the FSB has flagged that concentrated AI supply chains in cloud infrastructure and pretrained models represent systemic financial-stability vulnerabilities

- Ongoing monitoring of vendor model performance, not just at onboarding

Generative AI and Agentic Systems: The Governance Gap Boards Cannot Ignore

Why GenAI Is Categorically Different

Generative AI — LLMs used for document processing, customer communication, or regulatory reporting drafts — and agentic AI systems carry a different risk profile than traditional predictive models. NIST's GenAI profile (AI 600-1, 2024) and MAS's December 2024 guidance both call out GenAI as requiring additional governance controls beyond standard model risk management.

The core challenge is non-determinism. The same prompt can produce different outputs. That makes traditional validation approaches — backtesting, performance benchmarking against historical data — insufficient on their own. Key risks that traditional MRM frameworks weren't designed to catch include:

- Hallucinations: confident but incorrect outputs that are difficult to detect, per FSB's 2024 findings

- Prompt injection: adversarial inputs that manipulate model behavior, flagged by BIS

- Privacy leakage: training data exposed through model outputs

- Scope creep: models operating beyond their validated and approved purpose

The Agentic AI Question Boards Need to Ask Now

The risks above are compounded when AI moves from generating outputs to taking action. Agentic systems can chain decisions and commit institutional resources without moment-to-moment human oversight. OCC Bulletin 2026-13 notes that generative AI and agentic AI models are novel and rapidly evolving — and that they fall outside the scope of the revised model risk guidance. That gap is a board-level governance problem, not a technical footnote.

Boards should require, at minimum:

- Clear decision boundaries — what actions can an agentic system take without human approval?

- Kill-switch protocols — how is the system halted if it behaves unexpectedly?

- Escalation triggers — what performance or behavioral threshold triggers human review?

These should be board-approved policies, not technical configurations managed below the risk committee level.

What Boards Should Be Asking — and Can Actually Inspect

The Six Questions Every Board Should Be Able to Answer

If these questions require extensive preparation to answer, that's the governance signal:

- How many AI models are currently in production?

- Which are the highest-risk models, and when were they last independently validated?

- Are any models operating outside their approved scope?

- What would trigger a board-level escalation from model failure?

- How are vendor and third-party models governed — do contracts include audit rights?

- Has the MRM framework been explicitly reviewed for GenAI applicability?

What Inspectable Execution Looks Like

Board oversight of AI model risk requires more than an annual briefing. Meaningful oversight means receiving a model risk posture report — not a data dump — that shows:

- Model inventory status — total models in production, risk tier distribution

- Validation currency — how many models have overdue validations

- Monitoring alerts — open performance threshold breaches

- Open findings — unresolved model limitations and remediation status

- Trend data — what changed since the last board briefing, not just a point-in-time snapshot

The distinction between a posture report and a data dump is whether the board can make decisions from it. If the report requires a 30-minute briefing to interpret, it isn't board-ready.

Accountability Design Is a Board Responsibility

Readable reporting only works when accountability is equally clear. Every material AI model should have a named individual owner — not a team — with defined responsibilities and a predetermined escalation path if the model fails. Diffuse ownership is not accountability.

When regulators examine governance documents and board minutes, they look for three things: evidence that someone was responsible, that the board was informed, and that the escalation path existed before the failure occurred.

Tyson Martin works with BFSI boards to establish the reporting architecture, decision rights, and escalation thresholds that make these six questions answerable without preparation — so the board is positioned to govern, not just respond.

Frequently Asked Questions

What is AI model risk management in the context of banking and financial services?

AI model risk management is the set of processes, governance structures, and controls designed to identify, assess, and mitigate the risk that AI/ML models produce incorrect outputs, are misused, or fail in ways that cause financial loss, regulatory penalty, or reputational harm — covering every model that influences a business decision, from credit underwriting to fraud detection.

How is AI model risk different from traditional model risk?

AI models introduce risks traditional MRM frameworks weren't designed to catch: opacity ("black box" behavior), non-deterministic outputs in generative systems, autonomous decision-making, and data drift over time. Addressing these requires updated governance policies, expanded validation, and continuous monitoring.

What regulations govern AI model risk management for US financial institutions in 2026?

The foundational standard is SR 11-7, updated by the April 2026 revised interagency model risk guidance. OCC Bulletin 2025-26 provides flexibility for community banks. The NIST AI RMF (including the 2024 GenAI profile) functions as the de facto benchmark for examiners. Cross-border institutions also face OSFI E-23 (effective May 2027) and MAS AI MRM guidance.

What is the board's specific role in AI model risk governance?

Boards are expected to approve AI governance frameworks and risk appetite, receive regular model risk reporting, and ensure escalation thresholds and accountability structures are in place. They don't manage models directly — but they must demonstrate meaningful oversight, not passive ratification of what management presents.

Does our existing model risk management framework cover generative AI?

Most existing MRM frameworks were built for deterministic predictive models and need explicit updating to address generative AI risks: hallucinations, non-deterministic outputs, and prompt-based vulnerabilities. Boards should benchmark their frameworks against the NIST GenAI profile (AI 600-1) and MAS's December 2024 AI MRM guidance.

What are the most common AI model governance failures regulators find?

The most frequent gaps regulators cite: incomplete or stale model inventories, validation that isn't independent from development, no formal decommission process for legacy models, inadequate vendor model due diligence, and board reporting too thin to support independent judgment.