Introduction

Financial institutions can no longer treat AI as an emerging experiment. According to the U.S. Treasury's December 2024 report, 78% of financial firms are already implementing generative AI — yet a PwC survey found only 12% consider their model risk management function highly robust. That gap is what examiners find first.

The question boards and executives face isn't whether to deploy AI. It's whether their governance can hold up when an examiner walks in, a model drifts, or a consumer harm surfaces. Policy binders don't hold up under that pressure — controls built into the system do.

This article addresses what financial institutions need to own right now: the regulatory expectations that hardened in 2026, the five structural pillars of an effective AI governance framework, and the specific board actions that move an institution from documented policy to a posture it can actually defend.

Key Takeaways

- The FS AI RMF (February 2026) sets operational control expectations across governance, data, model risk, and consumer protection — moving well beyond high-level principles

- Only 12% of financial institutions rate their model risk management as highly robust

- Effective AI governance requires five pillars: governance structure, risk tiering, model lifecycle controls, human oversight, and vendor risk

- Operationalization means controls live in systems and logs, not policy documents

- Boards need answers to three questions on demand: where AI is deployed, who owns each use case, and what evidence confirms controls are working

Why 2026 Is the Inflection Point for AI Governance in Financial Services

The regulatory posture toward AI in financial services shifted this year — not gradually, but with real supervisory teeth.

On April 17, 2026, the OCC, Federal Reserve, and FDIC issued revised interagency model risk guidance (SR 26-2) covering model development, validation, monitoring, governance, and third-party products. This guidance explicitly excludes generative and agentic AI — regulators view these technologies as sufficiently novel to warrant a separate request for information rather than folding them into existing model risk rules.

The message is direct: traditional model risk expectations are now the floor. Generative AI requirements are coming next.

The Governance Debt Problem

Many institutions are running AI-driven decisioning on infrastructure that was never designed to support it. Legacy systems, fragmented model inventories, and inconsistent ownership across business lines create a structural gap between how AI is actually operating and what governance programs claim to cover.

Deloitte's 2025 EMEA Model Risk Management Survey of 136 banks and insurers found that 94% of large banks use generative AI, yet more than half cited transparency and explainability as active hurdles. PwC's parallel survey found that more than 40% rated their MRM function as only halfway adequate, specifically flagging AI governance, staffing, and expertise gaps.

This is the governance debt problem: AI adoption has outpaced oversight capability, and the gap is widening as supervisory expectations tighten.

The Risk of Waiting

Waiting for full regulatory clarity before building a governance program is itself a risk decision — and not a conservative one. Supervisory frameworks are hardening faster than internal programs at most institutions are maturing, and examiners don't grade on a curve for institutions that haven't started.

The 2026 Regulatory Landscape: What Financial Institutions Must Know Now

The FS AI RMF: What It Actually Is

On February 19, 2026, the U.S. Treasury released two new resources for AI governance in financial services: the AI Lexicon and the Financial Services AI Risk Management Framework (FS AI RMF). Both emerged from AIEOG, a public-private initiative established by FSSCC and Treasury in late 2024. The FS AI RMF was built with input from over 100 financial institutions, the Cyber Risk Institute, and U.S. and international agencies including NIST.

The FS AI RMF is an operational architecture standard built to withstand audit and supervisory examination — adapted from the NIST AI RMF with 230 control objectives specific to financial services' regulatory environment.

The Four FS AI RMF Components

| Component | Purpose |

|---|---|

| AI Adoption Stage Questionnaire | Maturity-based self-assessment that maps your adoption stage to relevant control objectives |

| Risk and Control Matrix | 230 control objectives organized by risk area and adoption stage — the central control engine |

| Guidebook | Step-by-step implementation guidance for deploying the framework operationally |

| Control Objective Reference Guide | Example controls and evidence artifacts for audit readiness |

These four components work as an integrated system. The questionnaire establishes your starting point, the matrix maps applicable controls, the guidebook drives implementation, and the reference guide builds your audit trail.

The Six AIEOG Deliverables

Alongside the FS AI RMF, six coordinated deliverables address the full AI risk lifecycle:

- AI Lexicon — standardized terminology across the sector

- Financial Services AI Risk Management Framework — the core governance architecture

- Identity and Authentication — mitigations for AI-related identity risks

- AI and Explainability in Finance — regulatory and operational explainability guidance

- Data Nutrition Labeling — transparency standards for training and inference data

- AI-Enhanced Fraud — detection and response guidance for AI-enabled fraud

What Examiners Will Actually Ask

The shift from prescriptive compliance to outcome-based oversight is real. State regulators are moving in parallel — NY DFS, Colorado, and California have each issued AI-specific requirements for insurance that emphasize governance, bias controls, and audit access.

When examiners arrive, expect these questions:

- Where are controls implemented, and who owns them?

- What systems enforce them — not what policies describe them?

- What evidence demonstrates they're functioning?

- How is drift monitored and documented?

Narrative policy explanations will not satisfy supervisory review. Controls must live in systems and logs.

The Five Pillars of an Effective Financial Services AI Governance Framework

Pillar 1 — Governance Structure and Decision Rights

Governance starts with separation: policy (what's required) belongs to the second line; delivery (how it's implemented) belongs to the first. The structure follows the three lines of defense:

- First line builds AI systems and performs initial control assessment

- Second line sets policy, governs, and challenges first-line assessments

- Third line provides independent audit assurance across both

What distinguishes functional governance from performative governance is whether decision rights and escalation thresholds hold under real incident conditions. A decision-rights map — defining who can approve AI use cases, who escalates at what threshold, and who owns remediation — is the artifact that makes this concrete rather than conceptual.

Pillar 2 — Risk-Tiered AI Use Case Assessment

Not all AI carries equal risk, and treating it uniformly creates two problems: governance overhead that slows low-risk innovation, and insufficient scrutiny on high-impact deployments.

A proportional intake process classifies AI use cases at the outset:

- Identify the AI type: generative, agentic, or traditional ML — each carries different failure modes

- Classify the risk tier: based on data sensitivity, decision impact, and regulatory exposure

- Apply controls proportionally: high-impact use cases (credit decisioning, suitability assessments, customer-facing interactions) require independent review and additional validation; internal productivity tools follow a lighter, faster path

This approach lets innovation move quickly where risk is low while preserving rigor where consumer or regulatory exposure is real.

Pillar 3 — Model Lifecycle Controls and Testing

Controls must be embedded across the full AI lifecycle — from data design through continuous post-deployment monitoring. Retrofitting governance after deployment is both harder and less defensible.

Key embedded controls include:

- Bias testing and fairness metrics during development

- Independent validation before deployment

- Drift detection and real-time anomaly alerting post-deployment

- Explainability thresholds for consumer-facing decisions

- Prompt testing and red-team exercises for generative models

- Pre-defined incident response playbooks covering toxicity, data leakage, performance drift, and kill-switch protocols

The incident response piece matters more than most institutions recognize. Institutions that manage AI failures well define their failure criteria — and their response thresholds — before a model goes live.

Pillar 4 — Human-in-the-Loop Oversight

In regulated financial services, AI handles analytical processing and pattern recognition — but humans retain accountability over consequential decisions. That division isn't just sound risk management; it's a regulatory requirement.

CFPB Circular 2022-03 is explicit: creditors using AI or ML models for credit decisions must provide adverse action notices with specific, accurate reasons. A creditor's lack of understanding of its own model is not a defense. That means humans must remain in the loop at every decision point where accountability is required.

Pillar 5 — Third-Party and Vendor AI Risk

Internal accountability only goes so far. When a vendor's foundation model fails, the institution still owns the regulatory and reputational consequences — making third-party AI risk a structural governance obligation, not an incidental one.

Governance obligations for third-party AI should include:

- Contractual audit rights and documentation exchange requirements

- Data sovereignty and subprocessor transparency

- Incident trigger protocols with defined notification timelines

- Model cards and validation artifacts as machine-readable compliance inputs

As SR 26-2 states, model risk management principles apply to vendor products — including when code is proprietary and not directly accessible.

Operationalizing AI Governance: From Blueprint to Defensible Execution

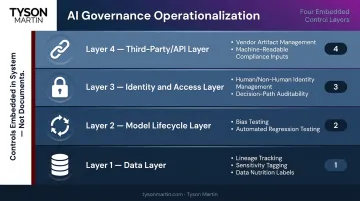

Moving Controls from Documents to Systems

The gap most institutions face is architectural: governance exists at the policy level but hasn't been translated into the technology stack. Operationalization means embedding controls directly into CI/CD and MLOps pipelines across four layers:

- Data layer: lineage tracking, sensitivity tagging at ingestion, data nutrition labels

- Model lifecycle layer: bias testing embedded in development, automated regression testing before deployment

- Identity and access layer: human and non-human identity management, decision-path auditability

- Third-party/API layer: vendor artifact management as machine-readable compliance inputs

What Evidence-Ready Governance Looks Like

The difference between institutions that pass examination and those that struggle comes down to one question: do controls live in systems, or in documents?

Evidence-ready governance means producing on demand:

- Immutable audit trails with timestamps

- Control owner assignments with documented accountability

- Test results from bias checks, validation runs, and red-team exercises

- Explainability artifacts and model cards

- Drift monitoring logs and anomaly alerts

This is exactly what the FS AI RMF's Control Objective Reference Guide is designed to support — example controls and evidence artifacts that survive supervisory scrutiny.

Governance as an Accelerator

Governance built well reduces time-to-value — it doesn't extend it. Three mechanisms make this work in practice:

- Staged deployments that match review depth to actual risk level

- Pre-approved use case catalogs that eliminate redundant governance cycles

- Feature flags that allow rollback without disrupting the broader pipeline

Innovation moves faster for low-risk use cases and more deliberately for high-impact ones — without rebuilding the process each time.

Integration with Enterprise Risk Management

AI governance built as a parallel system creates duplicate forums, dilutes accountability, and confuses escalation pathways. AI risks should integrate directly into existing ERM taxonomy — model risk, operational risk, compliance, cybersecurity, and third-party risk — sharing reporting structures and escalation paths rather than adding new ones.

For boards and executives who need governance structure immediately but lack internal capacity to build it, a board-level technology risk advisor is often the fastest path from exposure to defensible posture — one who can clarify decision rights, define escalation thresholds, and deliver a 90-day plan with clear owners and measurable outcomes. Tyson Martin's AI Governance Starter Pack does exactly that: an AI risk assessment, decision-rights map, board-level policy, and director briefing completed in a structured 30-day sprint.

What Boards and Executive Teams Must Do Differently

AI governance is not an IT initiative. It is a board governance obligation — and Bank Director's 2026 Risk Survey found that one-third of respondents did not fully comprehend agentic AI, while 84% cited AI-related fraud targeting customers as their top concern.

Three Questions Every Board Must Answer

Boards that cannot answer these questions confidently are carrying governance risk they haven't priced:

- Where are we using AI, and at what risk tier? — A current AI use case inventory with risk classifications

- Who owns governance accountability for each use case? — Named individuals, not functions

- What evidence exists that controls are functioning? — Test results and logs, not policy summaries

The Board's Role in Setting Governance Culture

Naming accountable individuals answers who owns each use case. What determines whether those owners act is the environment boards create around them.

Board engagement is itself a governance control. Boards that signal AI governance as a strategic priority, fund foundational tooling, and hold management accountable through consistent reporting make governance work in practice. Boards that treat it as a compliance checkbox get compliance-checkbox governance.

A practical board AI risk dashboard shows trend over time — not point-in-time snapshots. Each metric should:

- Map to an approved risk threshold

- Include a trend indicator (improving, stable, or worsening)

- Surface what changed since the last briefing and why it matters

When internal teams are managing day-to-day operations simultaneously, they're rarely positioned to build this structure from scratch. An external advisor with both board-level credibility and operational execution experience can close that gap — providing the independent validation and reporting architecture that gives regulators and directors something concrete to inspect.

Frequently Asked Questions

What is the Financial Services AI Risk Management Framework (FS AI RMF)?

Released by the U.S. Treasury in February 2026, the FS AI RMF adapts the NIST AI RMF for financial services — developed with over 100 institutions and the Cyber Risk Institute. Its 230 control objectives span governance, data management, model risk, and consumer protection, built to withstand supervisory examination, not just internal review.

How should financial institution boards oversee AI risk?

Boards should confirm AI risk is embedded in enterprise risk appetite, governance roles are assigned to named individuals, and reporting covers control effectiveness — not just policy summaries. The real test: can the institution demonstrate those controls to an examiner today, with evidence in hand?

What are the biggest AI governance risks for financial services firms in 2026?

The top risks are governance that lives only in policy documents without system-level enforcement, fragmented ownership of AI use cases across business units, inadequate third-party model transparency, and missing bias and explainability controls in high-impact decisioning systems such as credit underwriting or suitability assessments.

What does "operationalizing" AI governance actually mean?

Operationalization means embedding controls directly into the AI development and deployment pipeline — at the data, model lifecycle, identity, and vendor layers — so compliance is enforced by systems, not documented in policies. The proof is whether evidence (audit trails, test results, explainability artifacts) can be produced on demand during a supervisory review.

How do financial institutions balance AI innovation with regulatory compliance?

A risk-tiered approach allows low-risk use cases to move quickly under a lightweight governance track while higher-impact use cases receive proportionally deeper controls. When governance is embedded in workflows from the start rather than bolted on afterward, it reduces time-to-value rather than extending it.

What is the difference between AI governance and traditional model risk management?

Traditional model risk management was built for structured statistical models with defined inputs and outputs. AI governance — especially for generative and agentic systems — must go further, covering hallucination, prompt injection, bias drift, explainability, and continuous monitoring across the full deployment lifecycle. SR 26-2's explicit exclusion of generative AI confirms regulators recognize that gap and are moving to close it.