Ungoverned AI doesn't move faster — it accumulates debt. When a biased credit model surfaces in an examination, when a generative AI tool leaks customer data to a third-party vendor, when regulators ask for documentation that doesn't exist, the institution stops. Not to govern. To firefight.

AI is already reshaping credit decisions, fraud detection, compliance workflows, and customer engagement across financial services. But unlike retail or media, failures here carry systemic weight — for customers denied credit they qualified for, for markets exposed to correlated AI-driven errors, and for the institution's operating license. The floor for acceptable governance in financial services is simply higher than anywhere else.

The institutions pulling ahead aren't choosing between speed and safety. They're building governance structures that make speed possible.

Key Takeaways

- Strong AI governance creates a defined approval path for deployment; without it, every new use case is an unmanaged liability

- Boards must own four primary risks: algorithmic bias in lending, model drift, generative AI data leakage, and third-party liability gaps

- Treasury's FS AI RMF (February 2026) and SR 26-2 establish structured governance as a regulatory expectation, not a recommendation

- Boards don't need model-level fluency — they need inventory, accountability, monitoring, and tested escalation paths in place

- Governance is competitive infrastructure; treating it as compliance overhead is what slows institutions down

Why AI Governance Is Different in Financial Services

Financial services sits at a specific intersection of regulatory density, systemic risk, and public trust that no other sector quite matches. A hallucinating AI chatbot at a streaming service is embarrassing. The same failure at a bank — giving a customer wrong guidance on a loan modification or a regulatory deadline — creates legal exposure, potential UDAP violations, and reputational damage that compounds quickly.

The more structural issue is that AI systems are not static. They learn, drift, and can degrade silently without a single line of code changing. The revised interagency model risk guidance (SR 26-2) is explicit: ongoing monitoring must evaluate whether a model is performing as expected given changes in market conditions, data relevance, consumer behavior, and economic environment.

A credit scoring model trained before the 2022 rate shock may behave unpredictably today. Regulators have flagged exactly this scenario.

Three distinct risk categories make financial services uniquely exposed:

- Model drift — models degrade silently as market conditions shift, with no code change required to produce bad outputs

- GenAI over-reliance — staff and customers lack the domain expertise to catch confident but factually wrong AI-generated guidance

- Systemic amplification — when multiple institutions run similar models, errors don't stay contained to one firm

That last point deserves emphasis. The Financial Stability Board's 2024 analysis identifies how AI in finance may amplify systemic vulnerabilities through third-party dependencies, market concentration, and correlated decision-making across institutions. Confidence and accuracy are not the same thing — and at scale, that gap becomes a sector-wide problem.

In retail or media, AI failure is a customer experience problem. In financial services, it can mean regulatory enforcement, class-action exposure, or loss of charter. That's why "acceptable governance" means something different here.

The AI Risk Landscape Boards Need to Understand

Boards don't need to be model experts. They need to understand the risk categories clearly enough to ask the right questions — and recognize when thresholds have been crossed.

Algorithmic Bias and Fair Lending

AI models trained on historical data can encode and amplify past discrimination — in credit scoring, loan pricing, and account management — without any discriminatory intent. CFPB Circular 2022-03 makes clear that creditors cannot cite algorithmic complexity as a reason for failing to provide specific adverse action explanations. ECOA and Regulation B apply regardless of how sophisticated the model is.

This is both a legal and reputational risk. The board question isn't "did we intend to discriminate?" — it's "can we demonstrate that our model doesn't?"

Data Leakage and Generative AI

Every time a team feeds customer data into a third-party or generative AI tool, the institution needs to know where that data goes, who can access it, and what the vendor's data retention policy actually says. Treasury's 2024 cybersecurity risk report — based on interviews with 42 financial services and technology firms — identifies AI-specific data governance and operational risks as a priority concern.

The board-level question is simple: "Who approves AI tools that touch customer or regulated data, and what happens to that data after it's processed?" If nobody has a clear answer, that's a governance gap.

Model Drift and Vendor AI Risk

Two risks that compound each other:

- Model drift: Economic conditions and consumer behaviors shift after deployment. SR 11-7 requires ongoing monitoring of performance, outputs, data quality, and thresholds — not a one-time sign-off

- Vendor AI liability: Interagency third-party risk guidance is direct — outsourcing a model to a vendor does not outsource regulatory accountability. The institution owns the liability for what the model does, even when the vendor controls the model

Adversarial AI and Financial Crime

As institutions use AI to detect fraud, bad actors use AI to evade it — and to execute it. Synthetic identities, AI-generated social engineering, and deepfake-assisted account takeover are active attack methods, not theoretical ones.

FinCEN's November 2024 alert specifically directs financial institutions to identify and report fraud schemes involving deepfake media created with generative AI. This isn't just a security operations concern — it carries regulatory reporting obligations that boards should confirm are assigned and tested.

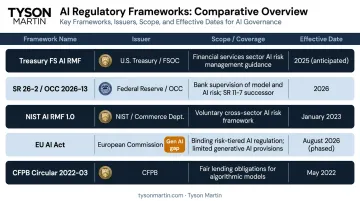

The US Regulatory Landscape Boards Should Know

The regulatory picture has clarified considerably in the last 18 months. Boards should have working familiarity with this stack:

| Framework | Issuer | What It Covers |

|---|---|---|

| FS AI RMF | Treasury (Feb 2026) | Financial services-specific AI risk management across the model lifecycle |

| SR 26-2 / OCC 2026-13 | Fed/FDIC/OCC (Apr 2026) | Revised model risk management for statistical and non-generative AI |

| NIST AI RMF 1.0 | NIST (2023) | Voluntary Govern/Map/Measure/Manage architecture; foundation for FS AI RMF |

| EU AI Act | European Union (2024) | Credit scoring and insurance pricing AI classified as high-risk; applies to US firms serving EU markets |

| CFPB Circular 2022-03 | CFPB | Adverse action explanation requirements for complex algorithm-based credit decisions |

Three things board members should read carefully within this stack:

SR 26-2 covers traditional statistical and non-generative AI only. Generative and agentic AI remain an open governance question under current federal guidance — which makes Treasury's FS AI RMF more relevant, not less.

The examination standard is inspectable process, not perfect prediction. Regulators require evidence of structured process — a model inventory, documented risk classification, validation before deployment, and continuous monitoring with escalation paths. Architecture choices remain yours; the burden of proof is on governance.

Regulators have drawn a clear line on board responsibility. Federal Reserve Vice Chair Bowman has stated that supervision should ensure banks can deploy AI responsibly while preserving a path for innovation. The expectation is board-level oversight of AI risk — not wholesale delegation to technical teams.

A Practical AI Governance Framework for Financial Leaders

The framework that satisfies regulators without killing business momentum has five components — none of which require the board to become model experts.

Step 1: Inventory and Classify

You cannot govern what you cannot see. Map every AI and machine learning system across the enterprise, including embedded third-party tools. Classify each by risk level — customer-facing vs. internal, high-stakes vs. low-stakes, regulatory vs. operational — and assign a named owner. SR 26-2 requires a comprehensive model inventory with enough detail to assess risk at both individual and aggregate levels. Many institutions discover untracked AI deployments during this exercise.

Step 2: Embed Controls Throughout the Model Lifecycle

Governance controls bolted on at deployment don't work. Fairness assessments, data quality standards, explainability requirements, and change management protocols need to be part of model design, validation, deployment, and retirement — not a final review gate. Treasury's FS AI RMF emphasizes lifecycle-integrated risk management on this point.

Step 3: Establish Human-in-the-Loop Requirements

Define which AI-driven decisions require human review before execution. Credit decisions, account closures, and suspicious activity flags are the obvious candidates. Human oversight shouldn't be a fallback for when AI fails — for material decisions, it should be a designed component of normal operations.

CFPB's adverse action requirements make this concrete: human-reviewable explanations for complex algorithms are a legal requirement, not just good practice.

Step 4: Implement Continuous Monitoring With Defined Escalation

Deploy monitoring that tracks model performance, fairness metrics, and output drift — with automated alerts and predefined escalation protocols. Boards should receive periodic reporting on AI model health framed in terms they can act on:

- Trend direction (improving, stable, degrading)

- Threshold breaches and their business impact

- Remediation status with owners and timelines

Step 5: Assign Accountability and Maintain Audit Trails

Every AI system affecting customers or material business processes needs a named owner accountable for performance, compliance, and documentation. Shared ownership is not ownership. Audit trails should be maintained so the institution can reconstruct any AI-influenced decision — not as a theoretical capability, but as something demonstrable in examination.

Clarifying Decision Rights: The Governance Layer Most Institutions Are Missing

Many institutions can describe what should be monitored. Far fewer have defined who has authority to act on it.

Who can halt a model? Who escalates a fairness threshold breach? Who approves a material change to a credit scoring algorithm? Without clear answers, governance becomes documentation rather than execution. When a real problem surfaces, accountability disperses into committee discussions rather than decisive action.

The board-management line is worth being precise about:

- Board: Sets risk appetite for AI use, receives meaningful reporting against it, confirms that escalation thresholds exist and have been tested

- Management: Owns operational decisions within that appetite — model selection, deployment, monitoring, and remediation

The failure mode works in both directions. Boards that get too deep into model mechanics lose sight of their actual oversight function. Boards too far removed miss the signals that thresholds have been crossed. Neither serves the institution well in an examination.

Organizations in transition — new leadership, M&A activity, rapid AI adoption, or post-incident environments — often face this gap most acutely. The internal capacity to establish decision rights, reporting structures, and escalation thresholds quickly doesn't always exist.

This is where Tyson Martin's board advisory work in regulated industries fits in: building the oversight structure and reporting cadence that lets institutions move forward without layering in new exposure along the way.

Frequently Asked Questions

What is AI governance in financial services?

AI governance in financial services is the structured set of policies, processes, accountability structures, and monitoring practices that ensure AI systems are deployed safely, fairly, and in compliance with regulatory requirements. Done well, it gives institutions a clear, defensible approval path — so new AI use cases move forward with confidence, not friction.

What are the biggest AI risks financial institutions face?

Five risk categories dominate:

- Algorithmic bias in credit and lending decisions

- Model drift and performance degradation over time

- Data leakage from generative AI tools

- Over-reliance on AI outputs by staff who can't challenge them

- Third-party vendor risk where the institution holds regulatory liability for models it doesn't control

How should a board oversee AI risk without getting into technical detail?

Focus on three things: confirming a governance structure exists (inventory, accountability, monitoring), receiving regular plain-English reporting on AI risk posture and trend direction, and verifying that escalation thresholds and decision rights are defined and tested. Understanding individual models is management's job — not the board's.

What regulatory frameworks apply to AI governance in US financial services?

The core US frameworks are:

- Treasury FS AI RMF (February 2026)

- SR 26-2 / OCC Bulletin 2026-13 (April 2026) — model risk

- CFPB Circular 2022-03 — adverse action requirements

- FinCEN guidance — AI-enabled fraud

Institutions serving European markets must also address the EU AI Act's high-risk classifications for credit scoring and insurance pricing.

How do financial institutions balance AI innovation with compliance?

By building governance into the deployment process from the start — not treating it as a review gate at the end. An institution with a clear AI inventory, risk classification, approval path, and monitoring structure can approve and deploy new AI use cases faster than one that has to stop and reconstruct governance after a problem surfaces.

When should a financial institution bring in outside AI governance expertise?

Outside advisors are most useful during rapid AI adoption, leadership transitions, post-incident remediation, or when board-level oversight capacity is thin. The typical need is establishing decision rights and reporting structures quickly — without slowing operations or creating new exposure while internal capacity catches up.