Introduction

Boards today face a risk environment that has genuinely changed. Cybersecurity threats, regulatory pressure, supply chain disruption, and AI-related exposure don't arrive one at a time — they compound. Yet many organizations still lack a clear answer to a basic question: who owns enterprise risk, and how does that information reach the boardroom?

The Chief Risk Officer exists to answer that question. Not by cataloguing every possible threat, but by giving executive teams and boards a decision-ready picture of the risks that could actually affect business objectives.

This article covers the CRO's core responsibilities, what effective board reporting looks like in practice, why reporting lines matter for governance integrity, and what separates executives who do this work well from those who don't.

Key Takeaways

- The CRO is the executive accountable for enterprise-wide risk — spanning strategic, operational, compliance, and reputational categories.

- The role originated with James Lam at GE Capital in 1993 and has expanded steadily as regulatory pressure and cyber exposure have raised the stakes for boards.

- Effective board risk reports connect risk posture to business objectives and support defensible decisions, not just document what risks exist.

- Where the CRO sits in the reporting structure — CEO, CFO, or directly to the board — determines whether escalation is credible or filtered.

What Is a Chief Risk Officer?

The CRO is the senior executive accountable for enabling effective governance of significant risks — strategic, operational, compliance, and reputational — to protect the organization and its stakeholders. The title first appeared in 1993 when James Lam took the role at GE Capital, a moment documented by Cambridge University Press as the formal origin of the function.

How the CRO Differs from Adjacent Roles

The CRO is often confused with neighboring executives who carry risk-related titles. Here's how they actually differ:

| Role | Primary Focus |

|---|---|

| CRO | Portfolio view across all risk domains; integrated ERM |

| CFO | Financial performance, financial risk |

| CISO | Information security and cyber risk |

| COO | Operational execution |

The CRO doesn't replace any of these roles. The function coordinates across them — closing the gaps that form between silos. That coordination mandate is exactly what external pressures have made non-negotiable.

Why the Role Has Grown

Risk used to be manageable department by department. That's no longer true. Several forces have created direct accountability for enterprise-wide governance:

- Sarbanes-Oxley internal control provisions requiring executive sign-off

- Basel Accord capital and risk management requirements for banks

- OCC heightened standards for large national banks

- Cyber threats that cross every organizational boundary simultaneously

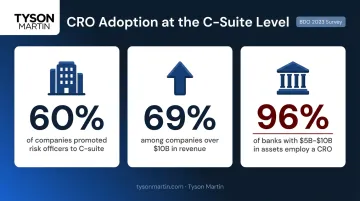

According to BDO's 2023 survey of companies with $100M to over $10B in annual turnover, 60% had promoted risk officers to C-suite status, rising to 69% among companies over $10B. In banking specifically, 96% of banks with $5B–$10B in assets now employ a CRO.

Core CRO Responsibilities

Risk Identification and Assessment

The CRO's starting point is building and maintaining a firm-wide view of risk. This means identifying threats across all categories — strategic, compliance, operational, reputational — then assessing each for likelihood and potential impact on business objectives.

What distinguishes this from department-level risk ownership is the portfolio perspective. Individual functions own their risks; the CRO sees how those risks interact, concentrate, and cascade.

Cybersecurity and Technology Risk

Cyber risk has become one of the most demanding areas on the CRO's agenda. EY's 2023 Global Board Risk Survey — covering 500 board directors at organizations with over $1B in revenue — ranked cyber attacks and data breaches as the third most significant risk for 2023. Only 40% of board members said they were very confident they understood their organization's greatest cyber threats.

The CRO's job is to translate technical security posture into business-level impact that executives and board members can actually use. What does a data breach cost in operational terms? What's the regulatory exposure from a vendor failure? Those are CRO-level questions.

This translation work is what Tyson Martin does with boards: working independently of the in-house CISO and security vendors, converting technical findings into plain-language risk posture updates that directors can govern from.

Risk Appetite, Limits, and Mitigation

The CRO defines and communicates the organization's risk appetite: the level of risk the organization is willing to accept in pursuit of its strategy. The Financial Stability Board defines it as "the aggregate level and types of risk a financial institution is willing to assume within its risk capacity to achieve its strategic objectives."

In practice, this means:

- Establishing measurable thresholds, not just statements of principle

- Defining who can accept risk at each level (management vs. board)

- Setting mitigation plans for risks that breach acceptable limits

- Using risk transfer tools such as insurance, contracts, and hedging where appropriate

When appetite is vague, it doesn't function. Effective CROs translate abstract tolerance into measurable criteria: acceptable downtime windows, fraud loss thresholds, data exposure limits. Once those thresholds are defined, the board can ask whether the organization is inside or outside appetite rather rather than debating what the statement means.

Risk Framework, Monitoring, and Reporting

Beyond appetite-setting, the CRO maintains the broader risk management infrastructure:

- Policies, procedures, and escalation protocols

- Employee awareness programs

- Due diligence on M&A activity and major strategic decisions

- Third-party and vendor risk governance

The monitoring and reporting function is where much of the board-visible work happens. CROs produce ongoing risk assessments, dashboards, and progress reports — and the quality of those reports has direct consequences for board oversight effectiveness.

The CRO and Board Reporting

Board reporting is one of the most consequential parts of the CRO role, and one of the most poorly executed. EY's 2023 survey found that 61% of board directors are not aligned with other board members on material risks expected over the next 12 months, and 60% agree emerging risks are insufficiently addressed in current frameworks.

That's not a risk identification problem. It's a communication problem.

What Effective Board Risk Reports Include

Boards are not risk managers. They need enough context to ask the right questions and make defensible decisions — not granular operational data. A useful board risk report typically includes:

- Risk posture summary: What changed since the last briefing

- Top risks mapped to strategic objectives: Not an inventory — a connection to business outcomes

- Risk appetite and threshold status: Are we inside or outside agreed limits?

- Escalated items: Issues requiring board-level decision or action

- Forward-looking indicators: Trends, not just snapshots

The difference between a report that enables oversight and one that creates noise comes down to structure: boards need trend visibility and clear choices, not data dumps.

Tyson Martin's board reporting methodology puts this into practice. Reports are structured in three layers: a one-page summary of decisions and changes, a visual snapshot (heat maps or scorecards), and a short appendix for directors who want depth. Every report includes a "Decisions requested" box with one to three items, each with options, cost ranges, and a recommended path.

The briefing format follows the same discipline — 15 minutes on top risks, 10 minutes reviewing the dashboard, 10 minutes on posture changes, 10 minutes on decisions. That structure keeps board time on governance, not technical review.

Reporting Frequency and Format

Most CROs report formally to the board or a risk/audit committee on a quarterly basis, though some organizations require monthly updates. EY's data shows the CRO engages with or reports to the board monthly or quarterly at 59% of surveyed organizations.

Quarterly cadence is not the full picture. Escalation protocols outside the regular cycle are essential — and should be pre-defined before an incident occurs. When a threshold-level risk emerges, the structure for escalating that to the board shouldn't be invented in the moment.

Organizations navigating leadership transitions, M&A activity, regulatory scrutiny, or cyber incidents often need more frequent and more structured risk communication than a quarterly cycle allows.

For organizations without a full-time CRO, a fractional or interim risk advisor can provide this structure quickly. Tyson Martin's fractional and interim engagements, for example, establish a board-ready reporting baseline within the first 30 days — including clarified decision rights and escalation thresholds — with stable trend reporting in place by day 90.

CRO Reporting Lines: CEO vs. Board — and Why It Matters

Most CROs report to the CEO or CFO. That proximity to operational decision-making has a real benefit: the CRO stays close to strategy execution and resource allocation decisions where risk considerations belong.

The risk is equally real. When the CRO and CEO hold conflicting views on risk-reward tradeoffs, the CRO is structurally disadvantaged in escalating concerns. The person they report to is the one whose judgment they may need to challenge.

The alternative — having the CRO report directly to the board or its risk/audit committee — parallels how external auditors report to the audit committee. It strengthens independence and reduces the chance that risk information is filtered before reaching directors.

Banking regulators have been explicit about this: the BIS states that banks should have an independent risk management function under the CRO with "sufficient stature, independence, resources, and access to the board."

Most organizations don't restructure reporting lines easily. What matters most, regardless of formal structure, is that the CRO has direct, unfiltered access to the board — particularly the risk and audit committee — and that escalation paths are pre-defined, documented, and respected across the full executive team.

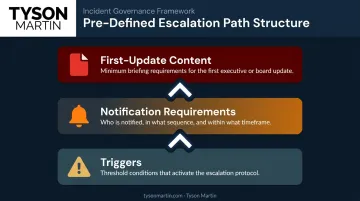

Escalation paths set before pressure arrives are the ones that actually get used. A one-page escalation ladder should specify:

- Triggers — the threshold conditions that move an issue from management to executive to board

- Notification requirements — who gets informed, in what sequence, and within what timeframe

- First-update content — what the initial board briefing must include at minimum

That structure removes the ambiguity that typically slows escalation precisely when speed matters most.

Qualifications and Skills of an Effective CRO

Background and Education

CRO backgrounds vary by sector, but common paths include:

- Auditing, financial analysis, actuarial, legal, or risk management

- Postgraduate education (MBA, master's in finance, economics, or accounting)

- In technology-heavy sectors: backgrounds in IT, cybersecurity, or operational risk

Relevant certifications include the Financial Risk Manager (FRM) from GARP, the Certification in Risk Management Assurance (CRMA) from the IIA, and the Chartered Enterprise Risk Analyst (CERA) from the SOA. In cyber-heavy contexts, CISSP and similar credentials are standard expectations.

What Actually Distinguishes Effective CROs

Most CRO candidates clear the technical bar. According to Spencer Stuart's assessment of senior risk leaders, what separates effective CROs is the ability to:

- Present critical risk insights confidently to non-technical audiences

- Advise boards and engage regulators without losing credibility

- Connect risk management to business strategy, not just compliance

- Apply judgment under pressure and challenge senior leadership when thresholds are breached

That last point is harder than it looks. Challenging a CEO or CFO on a risk call requires both analytical grounding and enough organizational standing to make the challenge stick.

Sector Context Matters

The core ERM framework transfers across industries, but domain knowledge is not optional:

- Financial services: Regulatory compliance, market risk, Basel requirements

- Healthcare: Patient safety, HIPAA, clinical operations risk

- Retail: Supply chain, consumer data, fraud, and physical operations

A CRO moving between sectors needs to rebuild domain fluency, not just apply a generic framework.

Frequently Asked Questions

What is the difference between a Chief Risk Officer and a Chief Information Security Officer?

The CISO focuses specifically on information security and cyber risk. The CRO covers a broader mandate: strategic, operational, compliance, and reputational risk. In many organizations the CISO reports to or coordinates with the CRO, but the roles are distinct and should not be merged.

Who does the Chief Risk Officer report to?

Most CROs report to the CEO or CFO, though some — particularly in financial services — report directly to the board or a board risk committee. The reporting line matters less than ensuring the CRO has direct access to the board when material risk thresholds are breached.

What qualifications does a Chief Risk Officer typically need?

Most CROs hold a postgraduate degree and bring extensive experience in risk management, finance, auditing, or a sector-relevant technical field. Credentials like the FRM, CRMA, or CERA strengthen the profile.

How often should a CRO report to the board?

Formal board or committee reporting is typically quarterly. Escalation protocols should allow the CRO to brief the board outside that cycle whenever a material risk threshold is breached — and those protocols should be defined before an incident, not during one.

What should be included in a CRO board report?

Core elements: current risk posture and what changed since the last briefing, top risks linked to strategic objectives, risk appetite and threshold status, and any items requiring board-level decision or action. The report should show trend, not just point-in-time status.

Do all organizations need a Chief Risk Officer?

Formal CRO roles are most common in regulated, publicly traded, or operationally complex organizations. Smaller organizations can address the function through a fractional or advisory arrangement — especially during leadership transitions, M&A activity, or periods of elevated regulatory scrutiny.