Reporting frequency is not a scheduling detail. It is a governance design choice that determines whether directors have current enough information to fulfill their oversight duty. Get it wrong in either direction — too infrequent or too voluminous — and you've created a governance failure.

The honest answer to "how often" is: it depends. Risk severity, organizational structure, regulatory environment, and what has materially changed since the last briefing all shape the right answer. This article lays out how to think through those factors and build a reporting rhythm that actually holds.

Key Takeaways

- Most organizations report top strategic risks to the full board at least quarterly; risk or audit committees typically receive updates monthly or more frequently.

- The right cadence depends on risk severity, velocity, regulatory requirements, and whether material conditions have changed.

- Calendar-based reporting is insufficient; KRI thresholds should trigger out-of-cycle briefings when risks cross predefined limits.

- Over-reporting is as harmful as under-reporting; too many updates dilute director attention and bury real escalations.

- The goal is a stable, trend-showing risk picture that enables decisions — not a comprehensive data dump.

Why Reporting Cadence Is a Governance Decision

Most boards treat risk reporting frequency as an administrative question — something handled when the annual meeting calendar gets set. That framing is wrong, and it leads to predictable failures.

Cadence is a governance design choice. It shapes whether the board has current enough information to exercise oversight and whether directors can distinguish a genuine escalation from routine noise. When the rhythm is miscalibrated, the board either acts without enough information or drowns in information it cannot parse.

The Gap Problem

Strategic risks evolve faster than most board meeting cycles. A purely calendar-driven approach leaves material information unreported for weeks — and boards cannot govern what they don't know is changing. According to NC State ERM Initiative's 2024 State of Risk Oversight survey, only 26% of organizations formally discuss risk information when the board reviews the strategic plan. That number reflects a structural disconnect, not individual oversight failures.

Regulatory expectations are tightening this gap further. The SEC's Release No. 33-11216, effective September 2023, requires public companies to disclose material cybersecurity incidents via Form 8-K generally within four business days after determining materiality. That clock doesn't pause for the next scheduled board meeting. Boards need an escalation process that can reach directors and disclosure counsel before the deadline, not after.

Two Failure Modes

That regulatory pressure makes cadence design a liability question, not just a process preference. Bad cadence creates two distinct governance problems:

- Under-reporting leaves the board blindsided by a risk management already knew about. Delaware courts have penalized exactly this scenario — Marchand v. Barnhill (2019) and In re Boeing Co. Derivative Litigation (2021) both allowed oversight claims to proceed where plaintiffs alleged no board-level system or regular process for mission-critical risk reporting.

- Over-reporting overwhelms directors. Real escalations get buried in routine updates, and material signals start to look like background noise.

Both are governance failures. The design challenge is building a cadence tight enough to catch what matters and disciplined enough not to cry wolf.

The Right Reporting Frequency Based on Context

There is no single correct answer, but the data shows clear patterns.

NC State's 2024 survey of 377 organizations found that among those formally reporting top risk exposures to the board: 44% do so annually, 42% quarterly, and 14% at every board meeting. Quarterly is nearly as common as annual — and it's clearly the better choice for organizations with dynamic or material risks.

Based on Risk Severity and Velocity

Not all risks move at the same speed. That distinction should drive reporting rhythm more than the calendar does.

Risk velocity — meaning how quickly a risk can escalate from emerging to material — is a separate governance dimension from likelihood and impact. A slow-moving, high-impact risk and a fast-moving, moderate-impact risk require different reporting rhythms entirely.

| Risk Type | Velocity | Appropriate Cadence |

|---|---|---|

| Active cyber incident | Immediate | Real-time escalation |

| Geopolitical supply chain disruption | Fast | Out-of-cycle briefing |

| Regulatory investigation | Moderate | Monthly committee update |

| Strategic competitive shift | Slow | Quarterly or semi-annual |

| Stable watch-list risk | Low | Annual or semi-annual |

High-severity, fast-moving risks warrant near-immediate escalation. Lower-velocity risks on a watch list are appropriate for quarterly or semi-annual scheduled updates. Applying the same cadence to both is where boards get surprised.

Based on Regulatory and Industry Environment

Velocity and severity set the internal logic for cadence. Regulatory requirements set the floor — and in many industries, that floor is specific and enforceable.

- Public companies: SEC Form 8-K Item 1.05 requires cybersecurity incident disclosure within four business days of materiality determination — boards need to be in the loop before that clock expires, not after.

- National banks: OCC Heightened Standards (12 CFR Part 30, Appendix D) require covered banks to have a board risk committee that meets at least quarterly and reviews the risk governance framework annually.

- Insurers: NAIC Corporate Governance Annual Disclosure Model Regulation requires disclosure of the frequency with which risk information is reviewed by the board and committees.

- Healthcare: HHS-OIG guidance calls for full board engagement in compliance oversight with regular reporting, without prescribing a universal cadence.

For organizations without hard mandates, frameworks from NACD and COSO provide the de facto standard — and following them is itself a defensibility argument if governance is ever challenged.

Based on Organizational Structure and Maturity

More mature organizations typically use a bifurcated model: the risk or audit committee receives detailed, frequent updates while the full board receives a synthesized strategic summary. This division of labor protects board time without sacrificing oversight rigor. NC State found 61% of organizations assign formal risk responsibility to a board committee — most often audit (51%) or a dedicated risk committee (30%). In financial services, risk committees dominate at 46%.

Organizations in transition should temporarily increase reporting frequency:

- New leadership — weekly executive checkpoints until risk posture is understood

- Post-incident recovery — daily or near-daily cadence during active response

- M&A integration — monthly at minimum until integration risk is stabilized

- Major platform changes — monthly rather than quarterly

When the business stabilizes, cadence can scale back. The point is to treat frequency as a variable, not a policy — one that adjusts as context changes and resets when it does.

Trigger-Based Reporting: When Risks Demand an Out-of-Cycle Update

Calendar-based reporting is necessary. It's not sufficient.

Organizations should pre-define Key Risk Indicator (KRI) thresholds that, when breached, automatically trigger an out-of-cycle board notification. Waiting for the next scheduled meeting is not an option when a material incident has occurred. A metric without triggers is a history lesson, not a governance tool.

Conditions That Require Immediate or Accelerated Notification

Red triggers — escalate immediately:

- A KRI crossing a predefined threshold

- A material cyber or operational incident

- A sudden regulatory or legal development

- A major acquisition, divestiture, or strategic announcement

- A significant shift in competitive or geopolitical environment

Amber triggers — accelerate the next update:

- A worsening trend for two consecutive reporting cycles

- A near-miss incident or rising exception count

- A threshold approached but not yet breached

The distinction between a full briefing and an executive notification should be decided before an incident — not under pressure when it happens.

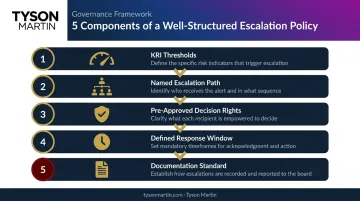

What a Well-Structured Escalation Policy Includes

Tyson Martin's escalation framework builds each of these components before a crisis forces improvisation:

- KRI thresholds tied to each top risk — measurable, tied to business impact not technical severity

- Named escalation path — who gets notified, at what level, and how fast

- Pre-approved decision rights — who can approve containment actions, engage outside counsel, authorize communications

- Defined response window — first update format, cadence during active incident, return-to-normal criteria

- Documentation standard — governance decisions traceable and defensible after the fact

Boeing's derivative litigation illustrates what happens without this architecture. The Delaware Chancery Court found it reasonably conceivable that directors failed to establish board-level monitoring for airplane safety, with no formal process in place for safety issues to reach the board at all. The court identified a governance design failure — not a paperwork problem.

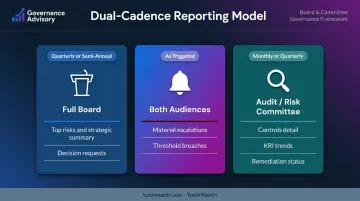

Full Board vs. Risk and Audit Committee: Who Gets What and When

Conflating these two audiences is one of the most common board reporting mistakes. It produces reports that serve neither well.

The full board needs strategic-level summaries with clear decision options framed in business terms. Directors are making oversight and resource allocation decisions, not evaluating control effectiveness.

The risk or audit committee needs depth — control effectiveness, audit exceptions, remediation timelines, regulatory status, and KRI performance against thresholds.

The Practical Dual-Cadence Model

| Audience | Content | Frequency |

|---|---|---|

| Full board | Top risks, strategic summary, decision requests | Quarterly or semi-annually |

| Audit/risk committee | Controls detail, exceptions, remediation status, KRI trends | Monthly or quarterly |

| Both | Material escalations, threshold breaches | As triggered |

This structure keeps the full board out of operational detail while ensuring committees maintain continuous oversight. Committees go deeper on controls, incidents, and compliance posture. The full board focuses on outcomes, material risk, and major tradeoffs.

One practical note: who presents matters. The presenter's role affects both the credibility of the information and the quality of board engagement.

SEC Regulation S-K Item 106 requires disclosure of the management positions responsible for cybersecurity risk and their relevant expertise — making accountability visible, not implicit. Broader strategic risk reporting typically routes through the CRO, ERM lead, CFO, or committee chair based on the risk domain.

Best Practices for Building a Reporting Rhythm That Holds

Establish Format Discipline First

The most effective board risk reports are short, trend-focused, and tied to decisions. A well-structured risk summary should include:

- Executive snapshot: Top 10–15 risks ranked by strategic impact and velocity

- What changed: Movement since the last briefing, with directional indicators

- Owner and remediation status: Named owners with current progress

- Decision requests: One to three specific asks with options and a recommended path

- Short appendix: Committee-level detail for those who want it

If it doesn't support a governance decision, it doesn't belong in a board risk report. The board view is the decision lens, not the evidence repository.

Address the Over-Reporting Trap Directly

NC State's 2024 data shows only 30% of organizations describe their risk management processes as mature or robust, and only 12% say risk management provides a strategic advantage. When reporting is too frequent or too voluminous, boards become desensitized — real escalations start to look like routine updates, and decision fatigue sets in.

Tyson Martin's approach reduces surface area by focusing committees on 5 to 10 enterprise risks they actively govern, with everything else rolling into operational reporting. The full board presentation uses 1–2 pages or 2–4 slides with a consistent format quarter to quarter. Boards track trend over time rather than re-litigating the same risk list each cycle.

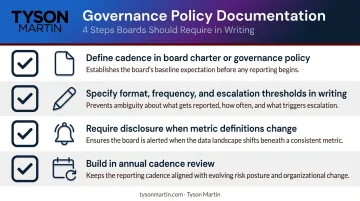

Document the Cadence in Governance Policy

The reporting rhythm should be an institutional expectation, not something dependent on individual initiative. This means:

- Define reporting cadence in the board charter or governance policy

- Specify format, frequency, and escalation thresholds in writing

- Require disclosure when metric definitions or scope change

- Build in an annual review of the cadence itself — does it still match how the business operates?

Consistency is what makes oversight credible. Organizations that lack a clear escalation framework before an incident are forced to improvise under pressure — which is exactly when improvisation fails. Establishing decision rights, reporting thresholds, and escalation protocols in advance is what separates a governance program that holds from one that collapses under stress.

Frequently Asked Questions

How often should a board review the risk register?

Most governance frameworks recommend the full board review the top risk register at least annually, with the risk or audit committee reviewing it quarterly. If material risks are actively shifting or the organization is in a transition period — new leadership, M&A, post-incident — quarterly committee review is the minimum, not the target.

How often should an RCSA be updated?

An RCSA is typically a formal annual exercise, but treat it as a living document. Refresh it whenever significant operational changes, incidents, regulatory shifts, or events like a new platform launch, acquisition, or major vendor change materially alter the control environment.

What triggers an out-of-cycle strategic risk report to the board?

Common triggers include pre-defined KRI threshold breaches, material cyber or operational incidents, sudden regulatory or legal developments, major M&A activity, or any event that materially shifts the organization's risk posture. Document these triggers in the escalation policy before an incident — not under pressure.

What is the difference between full board and audit committee risk reporting frequency?

The full board typically receives a summarized strategic risk update quarterly or semi-annually. The risk or audit committee reviews more detailed risk and control information monthly or quarterly — with the committee acting as the deeper oversight layer and escalating material issues to the full board between scheduled sessions.

How many risks should be presented to the board at one time?

Most effective board presentations focus on 10–15 prioritized risks, with only the top tier reaching the full board. NC State data shows 36% of organizations present fewer than five risks, while 33% present ten to nineteen. Beyond fifteen, director attention dilutes fast in sessions where risk discussion already competes for time.

What should a strategic risk report to the board include?

At minimum: an executive summary tied to strategic objectives, a visual heat map or risk dashboard, a "what changed since last briefing" section, top risks with named owners and remediation status, and explicit decision requests. Leave out anything that doesn't support a governance decision — blocked attack counts and patch totals describe system activity, not business exposure.