Introduction

Financial institutions have always been attractive targets — but the threat environment entering 2026 is categorically different from what came before. Boards are navigating AI-facilitated wire fraud, a post-FFIEC-CAT regulatory environment, and breach costs that have never been higher. According to IBM's 2024 Cost of a Data Breach report, the average data breach in the financial industry costs $6.08 million — 22% above the global average.

That number isn't just a headline. It reflects real exposure: regulatory penalties, customer remediation, reputational damage, and the operational cost of recovering systems under pressure.

Cybersecurity risk assessments are the mechanism that connects threat awareness to defensible decisions. Done well, they inform where to invest, what to prioritize, and how to demonstrate accountability to regulators and the board. Done poorly — or treated as an annual checkbox — they produce documentation that clears a compliance box while leaving actual exposure unexamined.

This guide covers:

- What a cybersecurity risk assessment is and what it should produce

- Why financial institutions face distinct exposure in 2026

- How to conduct an assessment step by step

- How to convert findings into board-ready governance

Key Takeaways

- A cybersecurity risk assessment maps what could go wrong, how likely it is, and the potential damage — across systems, data, vendors, and operations

- Financial institutions face regulatory scrutiny from multiple agencies, high concentration risk in digital infrastructure, and growing third-party exposure

- The FFIEC CAT was retired in August 2025 — institutions must now use NIST CSF 2.0, CRI Profile, or CISA CPGs

- Repeatable assessments follow a clear sequence: scope definition, asset inventory, threat evaluation, residual risk scoring, ownership assignment, and board reporting

- Findings only drive improvement when translated into clear decisions, stable governance metrics, and named owners — especially at the board level

What Is a Cybersecurity Risk Assessment for Financial Institutions?

A cybersecurity risk assessment is a structured process that answers three questions: What could go wrong? How likely is it? What would the impact be? Applied to a bank, credit union, or other financial entity, that means examining core banking systems, mobile platforms, cloud environments, vendor networks, and the people who access them.

The goal is risk-informed decision-making. Documentation is a byproduct, not the point.

Inherent Risk vs. Residual Risk

Two terms come up constantly, and the distinction matters:

- Inherent risk — the exposure level before any controls are applied

- Residual risk — what remains after controls are in place

Regulators expect both to be measured and documented. An institution that can only show controls exist — but can't demonstrate that those controls are proportionate to the underlying threat — will face findings under examination.

One-Time Audit vs. Ongoing Assessment Cycle

A common mistake is treating risk assessment as an annual event. Regulators don't. NYDFS 23 NYCRR 500, for example, requires assessments to be reviewed whenever business or technology changes materially affect cyber risk — not just once a year.

The distinction between a point-in-time audit and a living, repeatable assessment cycle is the difference between compliance theater and an actual security program.

Modern assessments are also far broader in scope than older IT risk reviews — spanning APIs, cloud configurations, and fourth-party vendor dependencies that add exposure most legacy frameworks weren't built to capture.

Why Financial Institutions Face Elevated Cybersecurity Risk in 2026

The financial sector isn't just frequently targeted — it's structurally exposed in ways that make breaches more consequential than in most industries.

The Verizon 2025 Data Breach Investigations Report recorded 3,336 incidents and 927 confirmed breaches in the Financial and Insurance sector alone — and that's only what gets reported. A compromise at one major institution can ripple through counterparties, correspondent banks, and payment networks.

Three Categories of Elevated Risk

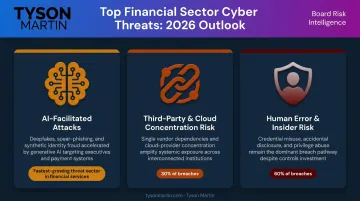

1. AI-Facilitated Attacks

Deepfake audio and video are now being used to impersonate executives in wire transfer authorizations. AI-generated phishing has become difficult to distinguish from legitimate communication at scale. Financial institutions are already logging these in fraud queues.

2. Third-Party and Cloud Concentration Risk

Third-party involvement in breaches doubled from 15% to 30% according to the 2025 DBIR. Cloud misconfigurations remain a top exposure vector — the Cloud Security Alliance identifies misconfiguration and inadequate change control as the number-one cloud threat based on input from over 500 experts.

Financial institutions that consolidate operations around a small number of cloud providers or core banking vendors carry significant concentration risk.

3. Human Error and Insider Risk

The human element was involved in approximately 60% of breaches in the 2025 DBIR. Credential misuse, misconfigured access controls, and accidental data exposure remain common — regardless of how sophisticated the technical controls are.

The Preparedness Gap

Those three risk categories share a common thread: they each exploit gaps that spending alone can't close. The KPMG 2025 Banking Technology Survey found that 91% of senior bank executives believed their additional cybersecurity spending was sufficient and 89% named security a top investment priority. High confidence in investment doesn't automatically translate to actual readiness — and regulators increasingly want institutions to demonstrate the difference.

The 2026 Regulatory Landscape: What Governs Cybersecurity Risk Assessments

Financial institutions don't answer to a single regulator. They operate under a layered framework where multiple agencies have overlapping authority, and assessments must satisfy all of them.

The Governing Framework

| Regulator / Rule | Primary Focus |

|---|---|

| FFIEC | Structural backbone for IT examination |

| GLBA Safeguards Rule | Requires written risk assessment and information security program |

| FDIC | Active threat monitoring and safety/soundness |

| OCC | Operational resilience |

| NCUA | 72-hour incident reporting for credit unions |

| NYDFS 23 NYCRR 500 | Strictest state-level rules; annual certification by April 15 |

| SEC | 4-business-day Form 8-K disclosure for material incidents |

| FINRA | Governance and documentation for broker-dealers |

The GLBA Safeguards Rule is the foundation: it requires a formal written risk assessment, controls designed to address identified risks, and service-provider oversight. Every major framework traces back to this requirement.

The FFIEC CAT Is Gone — Here's What Replaced It

The Cybersecurity Assessment Tool was officially retired on August 31, 2025. Institutions still running CAT-based programs need to transition. FFIEC now points to three primary alternatives:

- NIST CSF 2.0 — Released February 2024. Six core functions: Govern, Identify, Protect, Detect, Respond, Recover. Flexible, risk-based, and widely accepted by financial regulators

- CRI Cyber Profile v2.0 — Built specifically for financial institutions. Contains 318 Diagnostic Statements with verified mappings to FFIEC and NYDFS Part 500

- CISA Cybersecurity Performance Goals (CPG 2.0) — A prioritized minimum-baseline tool for critical infrastructure, including financial services

In practice, the most efficient path: map one assessment across multiple frameworks using crosswalks to reduce duplication. Pick one primary lens — typically NIST CSF 2.0 for executive communication — and cross-reference others only where examiners require specific evidence.

What Regulators Actually Want

Regulators don't just want evidence that controls exist. They want to see how risk assessment informs decisions, investment, and governance. Institutions that treat the process as a documentation exercise consistently face exam findings and enforcement action.

In practice, examiners look for:

- Board minutes that reference risk assessment outputs — not just acknowledgment that a report was received

- Investment decisions tied to identified gaps (budget line items, remediation timelines)

- Risk appetite statements that connect to assessment results and drive escalation thresholds

- Third-party oversight records showing the assessment extended beyond internal systems

How to Conduct a Cybersecurity Risk Assessment: A Step-by-Step Process

The process below follows NIST SP 800-30 — the Guide for Conducting Risk Assessments — which FFIEC has explicitly cited in its authentication and access guidance. Three failure points kill most assessments before they produce value: skipping asset inventory, treating assessment as a once-a-year event, and documenting findings without assigning anyone accountable for fixing them.

Step 1 — Define Scope and Objective

Before collecting any data, clarify the purpose. Is this driven by an upcoming FFIEC exam, GLBA audit, new vendor onboarding, or internal governance?

Scope determines which systems, business units, and third-party relationships are included. Assign assessment leads, subject matter experts, and approvers. Without a defined scope, results shift year-over-year and won't hold up under examination scrutiny.

Step 2 — Inventory Assets and Map the Environment

Identify every asset that carries risk:

- Core banking platforms

- Online and mobile banking applications

- Cloud-hosted systems and APIs

- Endpoints, including branch devices

- Third-party integrations and data-sharing relationships

Common oversights include unmonitored legacy systems still in production, shadow IT, and vendor-managed environments with no internal visibility. If it's not in the inventory, it won't appear in the assessment — and examiners will find it anyway.

Step 3 — Identify Threats and Evaluate Vulnerabilities

Map relevant threats to each asset category:

- Credential phishing targeting online banking portals

- Ransomware exploiting unpatched endpoints

- Misconfigured cloud storage exposing customer data

- Insider misuse of privileged access

- Supply chain compromise via third-party vendors

At this stage, assess inherent risk — before factoring in any existing controls. Use financial-sector threat intelligence, internal audit findings, and vendor security assessments as inputs.

Step 4 — Evaluate Existing Controls and Score Residual Risk

Assess control effectiveness across:

- MFA deployment and coverage

- Endpoint detection and response

- Network segmentation

- Access control policies and privilege reviews

- Patch cadence on critical systems

- Incident response capabilities

Score each risk by likelihood and impact using a consistent model — high/medium/low or a numerical scale. Document residual risk for every finding. Focus prioritization on high-likelihood, high-impact scenarios involving systems with regulatory dependencies or sensitive customer data.

Step 5 — Assign Ownership and Build a Remediation Plan

Every identified risk needs a named owner — a person accountable for resolution, not just a committee.

For each finding, document:

- Remediation steps and current status

- Target completion date

- Blockers and dependencies

- Compensating controls if full remediation isn't immediate

Record everything in a centralized risk register with mapped control references. This is where most programs break down: findings are documented but never assigned, so the same gaps resurface in the next exam.

Step 6 — Report Findings and Maintain the Process

Tailor outputs to the audience:

- Technical teams need specific remediation guidance with verification steps

- Executives need risk summaries tied to business impact and cost

- The board and audit committee need trend visibility, residual risk vs. risk appetite, and clear decisions for their agenda

Establish a reassessment cadence — annually at minimum, but also triggered by system changes, new vendors, incidents, or leadership transitions. The risk register is a living document, not an annual deliverable.

Turning Assessment Findings into Board-Ready Governance

Completing an assessment is only half the job. The harder challenge is translating findings into governance structures that hold under real pressure — during incidents, regulatory exams, or leadership transitions.

According to Deloitte's 2025 Audit Committee Practices Report, 62% of audit committees have primary oversight of cybersecurity risk, and 50% identified cybersecurity as the number-one focus area for the next 12 months. The expectation is clear. The question is whether assessment findings actually reach the board in a form they can use.

What Board Reporting Should Look Like

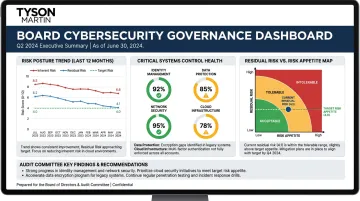

Effective board reporting on cybersecurity risk assessment includes:

- A stable dashboard showing trend over time — not a one-time snapshot

- Plain-English summary of risk posture and what changed since the last briefing

- Residual risk mapped against risk appetite — so the board can see whether exposure falls within the boundaries they've approved

- Decisions needed — not just status updates, but specific asks requiring board or committee action

The most common failure: overwhelming the board with technical detail. When directors can't distinguish between activity and actual risk reduction, they stop asking useful questions. That's not oversight — it's theater.

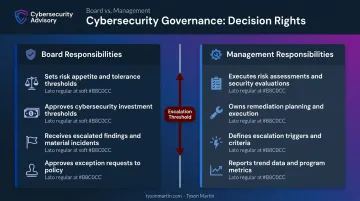

Decision Rights and Escalation Thresholds

Boards set risk appetite and approve investment thresholds. Management executes and reports. When these roles blur — or when escalation thresholds are never formally defined — boards can't provide meaningful oversight and executives can't act with confidence.

Assessment findings should directly define these boundaries:

- Which risks require board-level awareness

- Who can accept risk below material thresholds

- Who approves exceptions and for how long

- What triggers escalation during an active incident

Special Circumstances That Elevate Stakes

Three scenarios demand particular attention to the assessment-to-governance connection:

- M&A activity — acquiring unknown cyber debt from a target. Findings from pre-close due diligence should feed directly into integration governance and any contractual protections (holdbacks, escrows, indemnities)

- Leadership transitions — a new or interim CISO needs to establish posture quickly. Assessment findings provide the baseline; board reporting cadence ensures continuity of oversight during the gap

- Post-incident periods — regulators and the board both expect clear evidence of what changed and why. A well-maintained risk register and documented remediation plan is the difference between a credible response and a governance failure

The 90-Day Bridge

A 90-day executable plan — with named owners, measurable outcomes, and defined escalation paths — is what converts an assessment from a document into organizational improvement. Boards that insist on this deliverable get governance they can inspect; those that don't get a report that ages on a shelf.

How Tyson Martin Can Help

Tyson Martin works with boards and executive teams at financial institutions that need more than an assessment — they need the findings to drive defensible decisions at the governance level.

His background spans security and technology transformation at AWS, Home Depot, and Best Buy, with active roles at the World Economic Forum's Centre for Cybersecurity, NACD, and the NRF CISO Executive Committee. That puts him in the room where regulators, boards, and audit committees set expectations — not just reading about them after the fact.

For financial institutions, Tyson delivers:

- A plain-English risk posture boards can use for real oversight — not a technical inventory

- A stable dashboard showing trend direction and control health across critical systems

- Clear decision rights and escalation thresholds that hold during actual incidents

- A 90-day remediation plan with named owners, verification steps, and measurable outcomes

Institutions in transition — new leadership, post-incident, M&A integration, or operating without a full-time CISO — can bring Tyson in as interim CISO to stabilize assessment processes and board reporting quickly.

If your institution is preparing for an FFIEC exam, recovering from a security incident, or building a governance structure that needs to hold under regulatory scrutiny, reach out directly to discuss your situation.

Frequently Asked Questions

How often should financial institutions conduct a cybersecurity risk assessment?

Most regulators expect at minimum an annual assessment, but annual alone is no longer sufficient. Best practice calls for continuous monitoring supplemented by triggered reviews following system changes, new vendor onboarding, incidents, or leadership transitions.

What replaced the FFIEC Cybersecurity Assessment Tool after its August 2025 sunset?

FFIEC now points institutions toward three primary alternatives: NIST CSF 2.0, the CRI Cyber Profile (built specifically for financial institutions with 318 diagnostic statements), and CISA Cybersecurity Performance Goals. These frameworks can be used in combination, and mapping guides let institutions satisfy multiple regulatory obligations from a single assessment.

What is the difference between inherent risk and residual risk in a cybersecurity assessment?

Inherent risk is the level of exposure before any security controls are applied — a measure of the raw threat environment. Residual risk is what remains after controls are in place. Regulators expect both to be measured and documented; controls must be demonstrably proportionate to inherent risk, not just present.

Who is responsible for cybersecurity risk assessment oversight — the CISO, board, or both?

Both are responsible, but for different things. Management — including the CISO — executes the assessment and owns remediation. The board and audit committee provide oversight: approving risk appetite, reviewing findings at a strategic level, and holding management accountable.

What regulatory frameworks should financial institutions align with in 2026?

Most U.S. financial institutions should align with NIST CSF 2.0 and FFIEC IT Examination Handbook expectations as a baseline, layering in GLBA Safeguards Rule requirements, the CRI Profile for financial-sector specificity, and state-level rules such as NYDFS 23 NYCRR 500 where applicable. The specific frameworks depend on charter type and primary regulator.

How should cybersecurity risk assessment findings be communicated to the board?

Board reporting should be in plain English, tied to business impact and risk appetite, and trend-based rather than incident-by-incident. Directors need to see what changed since the last briefing, where the greatest exposure lies, and what management is doing about it — not a technical vulnerability inventory.