The cost of getting this wrong is significant. IBM's 2024 research puts the average breach cost for financial institutions at $6.08 million — 22% above the global average across all industries.

Here's the problem most institutions face: the tools exist. The security teams exist. What's missing is clear board-level oversight — defined decision rights, meaningful escalation thresholds, and reporting that actually informs governance rather than generating paperwork.

This article covers the regulatory landscape boards cannot sidestep, the top cyber risks specific to financial services, a practical five-stage management framework, and what effective board oversight looks like in practice versus performative compliance.

Key Takeaways

- Cyber risk in financial institutions is a governance problem, not just a technical one

- Regulators — OCC, Federal Reserve, and SEC — expect boards to demonstrate active, documented cyber oversight

- Top risks include ransomware, third-party vendor exposure, insider threats, cloud misconfiguration, and payment fraud

- Cyber risk management follows five stages: Identify, Assess, Mitigate, Monitor, and Report

- Boards need trend-based dashboards tied to pre-approved thresholds, not raw technical metrics

Why Cyber Risk Is a Board-Level Issue in Financial Services

The Governance Gap Nobody Talks About

Financial institutions sit at an intersection of concentrated risk: high-value data, high transaction volumes, and deep connections to critical payment infrastructure. When a bank or payment processor goes down, the disruption ripples outward.

Yet the most persistent vulnerability in many institutions isn't technical — it's structural. Security teams operate in technical silos. Boards receive reporting that describes activity rather than business impact. The result is a governance gap where executives can't make informed risk decisions because they're getting patch counts and tool rollouts instead of exposure analysis.

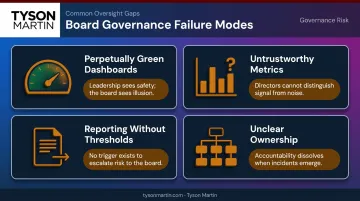

The specific failure modes show up repeatedly in board advisory work:

- Dashboards stay perpetually green even as business risk increases — teams learn to report what gets praise rather than what's true

- Metrics are easy to count but hard to trust — vulnerability counts spike when scanning improves, not necessarily when risk increases

- Reporting lacks decision-readiness — updates arrive without thresholds, making everything look high while nothing feels actionable

- Ownership is unclear — boards can't identify who is accountable for their top three cyber risks by name and role

Decision Rights: The Missing Architecture

When security incidents occur, financial institutions that lack defined decision rights don't slow down — they stop. Who can approve an emergency vendor contract? Who can authorize isolating a network segment? Who escalates to the regulator, and by what trigger?

Without pre-agreed answers, these questions get debated in real time during a crisis. Debating authority during an active incident isn't a security failure — it's a governance failure that security can't fix on its own.

Effective decision rights define three lanes:

- Security owns: policy guardrails, risk register management, and escalation protocols

- Shared approval required: go-live decisions for high-risk systems, major budget tradeoffs

- Security advises, business decides: risk acceptance, external communications

Boards set the thresholds. Management executes under them.

The Regulatory and Reputational Consequences

The SEC imposed a $10 million penalty on Intercontinental Exchange in 2024 for failing to timely report a cyber intrusion — a reporting failure, not a breach-of-operations failure. The agency also settled recordkeeping charges with ICBC Financial Services following a 2023 ransomware attack that disrupted U.S. Treasury market trades.

That regulatory exposure is the direct consequence of governance gaps — unclear escalation paths, undefined disclosure triggers, no pre-approved decision rights. Regulatory fines are only part of the damage. Customer attrition, loss of operating licenses, and downstream systemic risk to payment infrastructure multiply the financial impact of incidents that escalate without structure in place.

The Regulatory Landscape Financial Institutions Cannot Ignore

Boards sometimes treat regulatory compliance as a proxy for security. It isn't — and the distinction matters.

Key Frameworks and Requirements

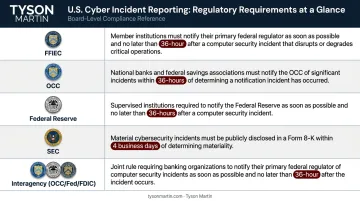

| Regulator / Body | Core Requirement |

|---|---|

| FFIEC | Annual board or committee review and approval of cybersecurity program (CAT sunsetted August 2025; successor frameworks apply) |

| OCC | Risk-based cybersecurity supervision aligned with NIST CSF |

| Federal Reserve | Notification of significant computer-security incidents within 36 hours of determination |

| SEC | Material incident disclosure on Form 8-K within 4 business days; annual disclosure of board cyber oversight under Regulation S-K Item 106 |

| OCC/Fed/FDIC (Interagency) | Documented oversight of third-party relationships including subcontractors and fourth parties |

The SEC's Regulation S-K Item 106 requirement is direct: public financial institutions must now describe the board's oversight of cybersecurity risks and management's expertise — in writing, on an annual basis. Boards that haven't formalized their oversight practices are now creating a disclosure problem alongside a governance one.

Compliance vs. Security: A Critical Distinction

Meeting regulatory minimums doesn't equal managing real risk. Organizations that optimize for passing audits end up with policies that look complete, controls that look mapped, and exceptions that get politely documented — while real paths to material loss stay open.

A practical example: a bank may have "MFA required" in its policy documents, while admins still use shared accounts in production. The compliance box is checked. The vulnerability is real.

Third-party and vendor oversight has become a specific area of regulatory focus. Interagency guidance now requires financial institutions to:

- Maintain current inventories of vendor relationships

- Conduct due diligence before and during engagements

- Monitor ongoing relationships, not just onboarding

- Review contract controls for security obligations

- Track subcontractor (fourth-party) risk for critical activities

This is a board-level governance responsibility, not a back-office procurement function.

The Top Cyber Security Risks Facing Financial Institutions

Ransomware and Business Disruption

Ransomware was present in 44% of all breaches reviewed in the Verizon 2025 DBIR — up from 32% the prior year. For financial institutions, the consequences extend beyond internal disruption. The 2023 ICBC ransomware attack disrupted U.S. Treasury market trades, illustrating how a single institution's incident can carry systemic consequences.

The median ransom payment was $115,000. The recovery costs, operational disruption, regulatory scrutiny, and reputational damage are harder to price.

Third-Party and Vendor Exposure

Third-party involvement in breaches doubled from 15% to 30% in the 2025 DBIR. For financial institutions, the reliance on fintech partners, cloud platforms, and payment processors creates an attack surface that often isn't fully governed.

The institution remains liable for vendor failures even when the breach originates externally. Effective oversight requires:

- A tiered vendor classification system that reflects actual business criticality

- Contract controls covering breach notification windows and audit rights

- Ongoing monitoring between renewals — not just point-in-time reviews

Insider Threats and Credential Compromise

Internal actors were responsible for 22% of finance sector breaches in the 2025 Verizon Finance Snapshot. Privileged account compromise — through phishing, social engineering, or credential theft — represents an outsized risk given financial institutions' access to high-value systems.

The governance question goes beyond whether MFA is deployed. Boards should be asking:

- Is privileged access reviewed on a defined cycle?

- Are exceptions tracked and documented?

- Does anomalous behavior trigger a defined escalation path?

Cloud Misconfiguration and Rapid Digital Expansion

FFIEC guidance is clear: financial institutions retain overall responsibility for safety and customer information protection, regardless of where their systems run. Accelerated digital transformation has frequently outpaced governance — misconfigured cloud environments, unvetted SaaS tools, and shadow IT create exposure that security teams may not have visibility into. Cloud adoption without a corresponding governance framework is where exposure accumulates quietly and accountability gaps go undetected.

Fraud and Payment System Manipulation

FinCEN reported over 680,000 check-fraud SARs in 2022, with mail-theft-related check fraud tied to more than $688 million in actual or attempted transactions in a six-month period in 2023. ACH manipulation and instant payment fraud add to this exposure.

Fraud controls are managed operationally, below the board's line of sight. Given the direct financial loss and regulatory reporting implications, payment fraud deserves a place in board-level risk reporting — not just operations dashboards.

A Cyber Risk Management Framework Built for Financial Services

The five-stage cycle — Identify → Assess → Mitigate → Monitor → Report — provides the operational backbone of any defensible cyber risk program. Each stage has both a management execution component and a board oversight component. When those roles blur, boards end up approving controls they don't understand — or approving nothing at all.

Identify and Assess

Identification starts with a comprehensive asset and data inventory. Financial institutions must know what they have, who can access it, and what the consequence of its loss would be. That scope includes shadow IT, business-owned SaaS tools, and vendor-managed systems — not just what the security team directly manages.

Assessment maps likelihood and business impact across those assets, producing a prioritized risk register. The board's role at this stage is to define what matters most:

- What's most likely to affect financial impact, uptime, or customer trust?

- What's changed since last quarter?

- What decision is needed from the board?

Management identifies specific threats. The board owns the thresholds against which those threats are evaluated.

Mitigate and Control

Not every risk can be eliminated. But every risk must have a documented owner, a control status, and a residual risk posture.

The board's role in mitigation is to approve risk appetite thresholds — not to design controls. When boards receive two or three options with stated costs, operational impact, and residual risk, they can make genuine tradeoff decisions. When they receive a single recommendation, they're rubber-stamping management's judgment rather than exercising governance.

Clear delegation to management is what makes execution inspectable. The board approves the direction and the boundaries. Management executes within them and escalates when reality conflicts with plan.

Monitor and Report

Point-in-time audits miss drift between reporting cycles. Continuous monitoring closes that gap — and what boards need to see from it is fundamentally different from what security teams track day to day.

Board-ready dashboard components (8–12 metrics maximum):

- Top 5 enterprise cyber risks in business impact terms — what moved, what's stuck

- Time to detect and contain — resilience benchmarks, not just prevention claims

- Critical control coverage on crown jewel systems — with exceptions tracked

- Security debt burn-down — are high-risk gaps closing faster than new ones arrive?

- Third-party exposure — critical vendors with current risk reviews and tested incident communication

What to exclude from board reporting:

- Raw vulnerability counts (punish visibility, ignore business impact)

- Blocked attack volumes (more alerts can mean weaker prevention)

- Audit findings closed (paperwork, not risk reduction)

- Budget size as a success metric

Every metric should include a threshold (what's acceptable), a trend line (are things improving?), and time-to-fix (how long does risk stay open?). Use three-month trends rather than monthly snapshots — a single month can be misleading; three months shows direction.

Organizations without a sitting CISO — or managing a CISO transition — often face an immediate gap in this reporting infrastructure. Engaging a board cyber advisor or interim CISO can establish a functioning board reporting structure within the first 30 days, maintaining oversight continuity without waiting months for a permanent hire.

That's the kind of transition support Tyson Martin provides in interim CISO and board advisory engagements.

What Effective Board Cyber Oversight Looks Like in Practice

Behaviors That Distinguish Governance from Theater

The audit and risk committee is the primary board-level governance body for cyber risk. Effective committees don't just receive briefings — they ask questions that force clarity about ownership, readiness, and evidence:

- "Who is the single accountable executive for cyber risk, and what's their authority?"

- "What are our top three cyber risks stated as business impact — not as vulnerabilities?"

- "Which risks are we actively accepting, and who approved them?"

- "How quickly can we restore critical services — and when did we last prove it?"

- "How do you prove controls work, not just that they exist?"

The standard cadence is quarterly formal board-level cyber briefings, with the audit and risk committee receiving a monthly one-page risk pulse between meetings. After a major incident or significant business change — acquisition, cloud migration, leadership transition — more frequent reporting is appropriate.

Connecting Cyber Risk to Business Outcomes

A common failure mode is boards that focus on compliance checklists and treat "we are compliant" as proof of readiness. It isn't. Compliance proves you met a minimum standard at a specific point in time. It doesn't prove you can detect, contain, and recover when something goes wrong under real pressure.

Effective oversight connects cyber risk to the outcomes boards already govern:

- A ransomware event isn't a malware problem — it's five days of billing disruption, contract penalties, and a missed quarter

- Weak vendor controls aren't just an IT problem — they represent potential customer attrition, regulatory review, and slowed integration after an acquisition

- Misconfigured cloud access isn't a technical finding — it's a compromised admin account that could expose customer data and disrupt operations

Translated into revenue impact, operational continuity, legal exposure, and customer trust, cyber risk becomes something boards can actually rank. It sits alongside credit risk and market risk — evaluated with the same rigor, funded with the same discipline.

That ranking only holds under pressure if escalation is pre-wired. Boards should agree in advance on amber and red triggers — conditions that automatically escalate to the CEO and board chair — rather than making real-time crisis decisions without one. When escalation is predictable, boards move faster and avoid both silence and overreaction.

Frequently Asked Questions

What is cyber risk management?

Cyber risk management is the process of identifying, assessing, and addressing risks posed by digital threats to an organization's systems, data, and operations. In financial institutions, it extends beyond technical controls to include governance structures, board-level accountability, and documented oversight practices that regulators now actively scrutinize.

What are the 5 stages of risk management?

The five stages are Identify, Assess, Mitigate, Monitor, and Report. Each stage requires management execution (doing the work) and board-level oversight (setting thresholds, approving risk appetite, reviewing trend-based reporting). Programs that separate these roles clearly perform better when incidents actually occur.

What are the top 5 cyber security risks for financial institutions?

Ransomware and business disruption, third-party and vendor exposure, insider threats and credential compromise, cloud misconfiguration and shadow IT, and fraud targeting payment rails (ACH manipulation, check fraud, instant payment fraud). All five require board visibility, not just operational management.

What is the board's role in cybersecurity oversight?

The board's role is governance: setting risk appetite, reviewing trend-based reporting, approving escalation thresholds, and ensuring management has the resources and accountability to execute. Boards don't design controls or manage incidents — they set the boundaries within which management operates and hold leadership accountable for outcomes.

How often should a financial institution's board review its cyber risk posture?

Most governance frameworks support at minimum quarterly board-level cyber briefings, with the audit and risk committee receiving a monthly risk pulse between sessions. Briefings should show trend data against pre-approved thresholds — not point-in-time status updates that can't inform decisions.

What regulations govern cybersecurity requirements for financial institutions?

Key frameworks include FFIEC cybersecurity guidance, the OCC's Cybersecurity Supervision Work Program, Federal Reserve 36-hour incident notification rules, SEC Form 8-K disclosure requirements (4 business days), and interagency third-party risk management guidance. All require documented board engagement, not passive receipt of management reports.