Introduction

Commercial banks occupy a unique position in the financial system: they absorb risk on behalf of depositors, investors, and the broader economy. Yet many of the most damaging institutional failures in recent history weren't caused by markets turning — they were caused by governance structures that failed to catch problems already visible inside the organization.

Silicon Valley Bank is the clearest recent example. The Federal Reserve's post-mortem identified weak board oversight, ineffective risk management, and an absent CRO for much of 2022 as central contributors to the bank's collapse. The interest rate risk was manageable. The governance failure was not.

That distinction is the core argument: risk governance structure — the formal system of roles, committees, decision rights, and reporting mechanisms that determines how risk is owned and overseen — is what separates institutions that catch problems early from those that discover them in a crisis. This article covers what that structure looks like, how it connects to measurable outcomes, where it most commonly breaks down, and which practices actually strengthen it.

Key Takeaways

- Risk governance structure is the oversight layer connecting board risk appetite to daily management execution — distinct from risk management itself.

- Core structural components: board-level risk committee, three lines of defense, a credible CRO function, and documented decision rights with escalation thresholds.

- Banks with stronger governance — particularly board independence and active audit committees — show higher capital adequacy, lower non-performing loan ratios, and greater shock resilience.

- Common failure modes: unclear role ownership, untested escalation paths, and frameworks that satisfy documentation requirements but fail under real incident pressure.

- Best practices: formalize the risk appetite statement, design board reporting around decisions (not data), and stress-test escalation paths through tabletop exercises.

What Is Risk Governance Structure in Commercial Banks?

Risk governance structure is the formal system of policies, roles, committees, and reporting mechanisms that a bank uses to identify, escalate, and oversee risk across the institution. It is not the same as risk management.

Risk management is the operational practice — identifying specific exposures, measuring them, and mitigating them. Risk governance is the structural oversight layer that sets the terms under which management manages: who is accountable for what, how oversight is exercised, and how the board's risk appetite connects to operational limits.

Why Banks Require Formal Governance Structures

Most industries treat governance quality as optional. For commercial banks, it's a regulatory expectation.

Banks operate with depositor funds, carry systemic importance, and face layered scrutiny from multiple regulators:

- OCC — sets board and senior management expectations via the Comptroller's Handbook on Corporate and Risk Governance

- Federal Reserve — enforces governance standards through supervisory ratings

- FDIC — oversight with direct examination authority over insured institutions

- Basel Committee — international principles that shape domestic regulatory frameworks

Governance gaps in any of these areas translate directly into examination findings and supervisory rating downgrades.

The board sets risk appetite, management executes within it, and the governance structure keeps those two functions aligned and mutually accountable.

Without a clear structural link between board-level appetite and operational limits, banks either over-restrict growth or accumulate unacceptable exposure — often without recognizing it until a crisis surfaces the gap.

Governance Requirements Are Expanding

The Basel Committee's 2021 and 2022 publications expanded governance requirements to include sustainability and climate-related financial risks. The Principles for the effective management and supervision of climate-related financial risks place climate risk explicitly within the board governance framework.

Regulators increasingly treat digital and cyber risk the same way — as board-level governance issues, not just IT concerns.

Key Components of an Effective Risk Governance Structure

Board-Level Risk Oversight and the Risk Appetite Statement

The board's primary governance function is approving the risk appetite statement (RAS), setting institution-wide risk limits, and holding management accountable for operating within those boundaries.

A well-structured RAS is not a qualitative aspiration like "moderate risk tolerance." It should include:

- Specific risk categories covered (credit, market, liquidity, operational, cyber, compliance)

- Quantitative thresholds that cascade to business unit limits

- Direct connection to capital planning and stress test parameters

- Clear definitions of what "in appetite" and "out of appetite" look like at each level

The board risk committee (or combined audit/risk committee) executes this oversight function. Its charter should specify independent director composition, required financial or risk expertise, meeting frequency, and what it reviews at each session: risk dashboards, exceptions to appetite, stress test results, and emerging risk briefings.

Meeting frequency is a governance signal. Examiners notice when a board risk committee meets only once per year.

Critically, the board's role is oversight, not operation. Boards that drift into managing risk directly create their own governance failures, just different ones from boards that disengage entirely.

The CRO Function and Management-Level Risk Committees

The Chief Risk Officer is the structural bridge between board-level governance and operational risk management. The CRO translates the board's risk appetite into enterprise-wide risk limits, oversees the risk framework, and provides the board with credible, independent risk reporting.

CRO reporting lines matter. A CRO who reports to the CFO rather than the CEO or directly to the board loses structural independence and creates a conflict of interest — revenue pressure can distort risk reporting. SVB's CRO vacancy through much of 2022 removed this function entirely during a period of rapidly accumulating interest rate exposure.

Below the CRO, management-level risk committees form the governance layer between board appetite and business unit decisions:

| Committee | Primary Scope |

|---|---|

| ALCO | Asset/liability, interest rate, and liquidity risk |

| Credit Risk Committee | Loan concentration, underwriting standards, NPL management |

| Operational Risk Committee | Process, people, and system failure exposures |

| Cyber/Technology Risk Committee | Digital infrastructure, third-party, and cyber exposures |

Each committee needs a defined scope, clear escalation triggers, and documented decision authority — not just a meeting cadence.

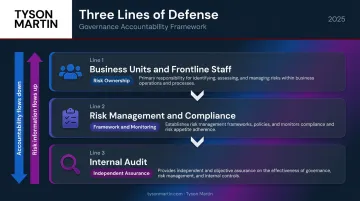

The Three Lines of Defense Model

The three lines distribute risk accountability across the institution without creating gaps or overlapping authority:

- Business units and frontline staff — own risk within their operations and are the first point of accountability

- Risk management and compliance functions — set the framework, monitor adherence, and challenge the first line's risk-taking

- Internal audit — provides independent, objective assurance that both prior lines are functioning as designed

Defining each line is the easy part. The model's most common structural failure is when those three lines operate as silos rather than an integrated system. Effective governance requires defined handoff points, shared risk language, and clear escalation thresholds — so risk information flows upward and accountability flows downward without distortion.

Decision Rights and Escalation Thresholds

Decision rights define who can approve what level of risk exposure, under what conditions, and with what documentation. Without explicit decision rights, risk decisions migrate informally to whoever is most confident or most senior in the room — decoupling accountability from authority.

Escalation thresholds are the mechanism that keeps governance functional under stress: pre-defined conditions that trigger movement from business line to CRO, from CRO to board risk committee, and from the board to regulators. These thresholds must be tested through scenario exercises, not just documented in a policy that sits unread until a crisis provides the first real test.

How Risk Governance Structure Impacts Bank Performance

Strong governance structure isn't just a compliance checkbox : it has measurable effects on capital adequacy, credit quality, and institutional resilience.

Governance and Financial Performance

Research consistently links governance quality to better risk outcomes. Board independence, audit committee activity, and ownership dispersion are significantly correlated with:

- Higher capital adequacy ratios — better-governed banks hold more adequate capital buffers

- Lower non-performing loan levels — governance structures that maintain credit discipline reduce NPL accumulation

- Stronger profitability — cleaner risk decision-making reduces unexpected loss drag

Recent research on audit committee effectiveness and systemic risk reinforces these findings, showing that active audit committees are linked to measurably lower systemic risk exposure in commercial banks.

Resilience During External Shocks

The difference between a disruption and a crisis often comes down to whether decision rights were clear before the event started. During COVID-19, banks with strong governance structures demonstrated greater capacity to sustain lending and maintain capital adequacy — their escalation protocols meant management could act quickly without waiting for governance bottlenecks to clear.

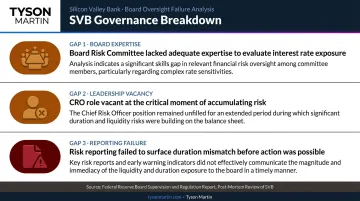

Poorly governed institutions face the opposite: ambiguous authority turns manageable risk events into crises. SVB is the clearest example. The governance failures weren't caused by the interest rate environment. They were caused by three specific gaps:

- A board risk committee without adequate expertise to evaluate the exposure

- A vacant CRO role at the critical moment

- Risk reporting that failed to surface the duration mismatch before it was too late to act

Direct Regulatory Impact

U.S. regulators use governance quality as a supervisory input, not just backdrop. Governance deficiencies translate directly into:

- Examination findings and supervisory rating downgrades

- Consent orders and enforcement actions (both the OCC and Federal Reserve maintain active enforcement records tied to governance failures)

- Remediation requirements that are significantly more expensive than proactive governance investment

The OCC's Heightened Standards framework sets explicit governance expectations for larger institutions, with examiners evaluating whether board risk committees are structurally equipped to oversee the institution's actual risk profile, not just present on the org chart.

Common Governance Failures and Warning Signs

Most governance failures aren't dramatic. They're quiet structural gaps that accumulate invisibly until a stress event makes them visible.

Structural Failures That Create Hidden Exposure

The most common structural problems:

- CRO independence compromised by reporting to a revenue-generating executive (CFO or business line head)

- Board risk committees without clear charters or adequate meeting frequency

- Undocumented or untested decision rights — authority assumed rather than assigned

- Risk ownership diffused so broadly that no single function is actually accountable for key risk categories

- Overly complex governance structures that slow decision-making and crisis response — complexity that looks thorough on paper can create operational risk when speed matters

The Governance-Execution Gap

This is where most invisible risk accumulates: the gap between documented governance and operational governance.

Many banks have frameworks that satisfy regulatory documentation requirements but fail in practice. Escalation paths go untested, decision rights go unchallenged, and risk committees treat their meetings as reporting events rather than decision-making forums. The documentation says one thing; what happens under pressure says another.

Closing this gap requires stress-testing governance before a crisis does it for you — tabletop exercises, escalation drills, and decision-rights reviews conducted while conditions are controlled.

Board Reporting as the Last-Mile Breakdown

When the board receives risk reporting that is too granular, too metric-heavy, or too jargon-dense to generate a decision or an escalation, the governance structure has failed at its most critical function.

Boards need to see three things:

- What changed since the last review

- What is outside appetite

- What decision or escalation is required from the board

The board isn't a passive audience for management reporting — it's the governance decision-maker, and reporting should be built to drive that function.

Best Practices for Building a Stronger Risk Governance Structure

Establish a Specific, Actionable Risk Appetite Statement

The RAS is the governance anchor. It should be specific enough to generate real quantitative limits at every operational level. A qualitative statement like "we maintain moderate credit risk" is governance theater: it cannot cascade to a business unit limit, cannot generate an exception flag, and cannot tell a loan officer where the line is.

An effective RAS includes three interconnected components:

- Quantitative thresholds defined by risk category

- Explicit connection to capital planning and stress scenarios

- A clear cascade from board-approved limits to divisional and product-level constraints

When the RAS is specific, the governance structure has something real to enforce.

Design Board Reporting for Decision-Making, Not Documentation

Board-level dashboards should answer three questions before anything else: What changed? What's outside appetite? What does the board need to decide or escalate?

This requires a deliberate reporting design process that starts with what the board needs to decide, not what management wants to report. The difference matters: management reporting optimizes for completeness; board reporting optimizes for decision quality.

Tyson Martin builds board risk reporting structures around this principle. The format is direct: 8 to 12 decision-grade metrics mapped to approved risk appetite thresholds, trend data over three to four quarters rather than single-point snapshots, and a "Decisions Requested" section with options, cost ranges, and a recommended path.

The entire board pack fits in one to two pages, with supporting evidence in appendices. If a metric can't answer "in appetite or out of appetite," it belongs in management reporting, not board reporting.

Boards without internal reporting design expertise often benefit from an outside advisor who can build a reporting structure calibrated to board-level decision rights — one that shows trend rather than trivia and keeps board attention on governance rather than operational detail.

Stress-Test Governance Structures Through Scenario Exercises

Escalation paths, decision rights thresholds, and committee charters need to be exercised against realistic stress scenarios — not just reviewed in annual audits. A documentation review cannot surface the governance gaps that a tabletop exercise will find in 90 minutes.

Effective scenarios test the governance structure, not just the technical response:

- A sudden credit concentration in a single sector

- A cyber incident that requires real-time decisions about system availability

- A liquidity shortfall requiring rapid escalation to the board risk committee

- A vendor failure that becomes the bank's operational failure

The exercises should involve the board risk committee, CRO, and business leadership together — and should specifically rehearse who declares an incident, who can authorize system changes, who communicates with regulators, and who calls the board chair. These are governance decisions. Making them for the first time during an actual crisis is how manageable events become catastrophic ones.

Conduct an Annual Governance Gap Assessment Against Regulatory Standards

Governance requirements from the OCC, Basel Committee, and Federal Reserve have grown more prescriptive. Annual alignment reviews ensure the governance structure reflects current expectations rather than the standards that were current when the framework was last designed.

Banks that embed regulatory standards into governance design from the start avoid the disruption of reactive upgrades under supervisory pressure. The practical difference: fewer examination findings, lower remediation costs, and examiners who see a governance structure built to current standards rather than one being patched to meet them.

Frequently Asked Questions

What is the risk governance framework of a bank?

A bank's risk governance framework is the formal structure of policies, committees, roles, and reporting mechanisms that define how risk is identified, escalated, and overseen. It is anchored by the board's risk appetite statement and executed through structures like the three lines of defense and board risk committee oversight.

What are the 4 P's of governance?

The 4 P's are People, Purpose, Process, and Performance. In banking risk governance, this means independent directors with relevant expertise, a clearly defined risk appetite, documented decision rights and escalation thresholds, and risk performance metrics that confirm the structure is functioning as intended.

What is the difference between risk management and risk governance in banking?

Risk management is the operational practice of identifying, measuring, and mitigating specific risks. Risk governance is the structural oversight layer that determines who is accountable, sets the risk appetite boundaries, and ensures management stays within them. Governance gives management the framework to operate — without it, accountability has no structure.

What role does the board play in bank risk governance?

The board sets the institution's risk appetite, approves major risk limits, oversees the CRO and board risk committee, and holds management accountable for operating within approved boundaries. Day-to-day risk management belongs to the CRO — boards that blur this line create their own governance failure.

What are the three lines of defense in bank risk governance?

The three lines are: (1) business units that own risk within their operations, (2) risk management and compliance functions that set frameworks and monitor adherence, and (3) internal audit that independently verifies both prior lines are functioning as designed. When accountability handoffs between the three lines break down, risk information distorts and gaps go undetected.