A quick clarification before we proceed: "OCC" can refer to two different organizations — the Office of the Comptroller of the Currency (the banking regulator) and the Options Clearing Corporation. This post is exclusively about the Office of the Comptroller of the Currency and its requirements under Appendix D to 12 CFR Part 30.

What follows is a plain-English breakdown of what the OCC requires, who it applies to, and what strong execution actually looks like.

Key Takeaways

- The OCC's Heightened Standards apply to banks with $50B+ in average total consolidated assets, plus certain smaller institutions the OCC determines present heightened risk

- A compliant risk appetite statement requires both qualitative components (risk culture, behavioral guidance) and quantitative limits (earnings, capital, liquidity)

- The RAS must be embedded in six specific governance processes, spanning strategic planning through compensation design

- Boards must actively use the RAS to challenge management, not treat it as an annual sign-off exercise

- Breach protocols must include consequences tied to magnitude and recurrence, with escalation paths that carry real weight

Who the OCC's Heightened Standards Apply To

The OCC's risk appetite statement requirement lives inside the "Heightened Standards" framework — formally, Appendix D to 12 CFR Part 30, which became effective November 10, 2014.

The Coverage Threshold

The standards apply to "covered banks" — defined in Appendix D Section I.A and I.E as:

- Insured national banks

- Insured federal savings associations

- Insured federal branches

...with average total consolidated assets of $50 billion or more.

Note: A December 2025 Federal Register proposal would raise this threshold to $700 billion. As of this writing, the current controlling text still reads $50 billion. Banks in or near the threshold should monitor that rulemaking carefully.

Who Else Gets Pulled In

Being under $50B doesn't automatically mean exemption. Appendix D Section I.E.5 extends coverage to banks below the threshold when:

- The bank's parent company controls at least one covered bank

- The OCC determines the bank's operations are "highly complex or otherwise present a heightened risk"

The OCC also reserves authority under Section I.C to apply or remove these standards based on its own assessment of a bank's risk profile. That reservation matters: no institution should assume it's safely out of scope without confirming with its examiner.

The Regulatory Definition of Risk Appetite

Appendix D Section I.E.10 defines risk appetite precisely:

The aggregate level and types of risk the board of directors and management are willing to assume to achieve a covered bank's strategic objectives and business plan, consistent with applicable capital, liquidity, and other regulatory requirements.

Three things stand out in that language. The board must be explicitly involved — not just management. Appetite ties directly to strategic objectives, not abstract risk tolerance. And the frame is regulatory constraints, not internal preference alone.

What Must Be in an OCC-Compliant Risk Appetite Statement

Appendix D Section II.E requires a comprehensive, written risk appetite statement that serves as the foundation for the entire risk governance framework. Vague, aspirational language won't satisfy that standard.

The Qualitative Component

The qualitative component must describe a safe and sound risk culture and articulate how the bank will assess and accept risk — including risks that resist easy quantification, like reputational or strategic risk.

The key word is "meaningful." The OCC isn't looking for mission-statement prose. Qualitative language must give employees and management actual behavioral guidance — specific enough that someone making a credit decision or approving a new product can use it to orient their judgment.

The Quantitative Component

The quantitative component requires measurable limits addressing:

- Earnings — what levels of earnings volatility are acceptable

- Capital — minimum buffers the bank will maintain

- Liquidity — thresholds below which action is required

These limits must incorporate sound stress testing processes and must be calibrated to prompt action before the bank's financial position is jeopardized — not as a reactive measure after the fact.

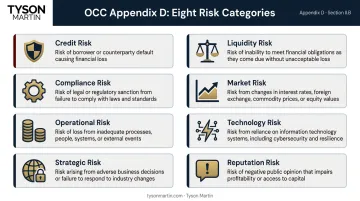

The Eight Risk Categories

The OCC's risk governance framework must cover all eight risk categories defined in Appendix D Section II.B:

| Risk Category | Description |

|---|---|

| Credit risk | Borrower/counterparty default |

| Interest rate risk | Balance sheet sensitivity to rate changes |

| Liquidity risk | Ability to meet obligations |

| Price risk | Market value fluctuations |

| Operational risk | Process, people, systems, and external events |

| Compliance risk | Legal and regulatory adherence |

| Strategic risk | Business model and execution decisions |

| Reputation risk | Public perception and trust |

Covered banks should set appetite levels across each category and, where practical, disaggregate limits to the front-line unit level.

The OCC's Own RAS as a Reference

In April 2016, the OCC published its own Enterprise Risk Appetite Statement — OCC News Release 2016-44 — covering nine risk domains including supervision, human capital, strategic, reputation, technology, operational, legal, external, and financial risk. The agency assigned categorical appetite levels across these domains, demonstrating that a well-structured RAS deliberately differentiates tolerance by risk type rather than applying a single posture across the board. The takeaway for covered banks: differentiated appetite levels — not a uniform risk stance — are the baseline expectation.

How the Risk Appetite Statement Anchors the Risk Governance Framework

The RAS isn't a standalone document. Under Appendix D Section II.K, it must be explicitly incorporated into six governance processes:

- Strategic and annual operating plans

- Capital stress testing and planning

- Liquidity stress testing and planning

- Product and service risk management (including new product approvals)

- Acquisition and divestiture decisions

- Compensation and performance management programs

If the RAS doesn't show up in these processes, it isn't functioning as the OCC intends.

The Three Lines of Defense and the RAS

Each line of defense has a distinct relationship to the risk appetite statement:

- Front line units set their own risk limits consistent with the RAS and monitor compliance with those limits, reporting to independent risk management at least quarterly

- Independent risk management designs the RAS, monitors the bank's aggregate risk profile against it quarterly, and escalates material breaches to the CEO and board

- Internal audit independently assesses whether the RAS and the broader governance framework are actually functioning as designed — at least annually

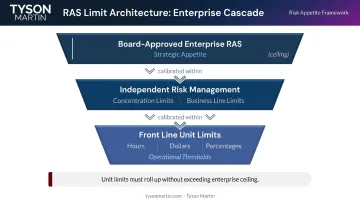

The Cascading Limit Architecture

Appendix D Section II.F requires concentration risk limits and front line unit risk limits to be calibrated so that, when aggregated, they do not exceed the board-approved enterprise RAS. The board-approved RAS sets the ceiling. Every management-level limit operates within it.

This cascading structure is a common examiner focus area. The question they're asking: do the unit-level limits actually roll up coherently to the enterprise appetite? If limits haven't been updated when strategy changed, the answer is often no.

What examiners want to see is a traceable line from board-approved appetite down to specific operational thresholds — hours of downtime, dollars of fraud loss, data loss windows — that management can report against with evidence. Structured workshops that convert board-level appetite into those unit-level metrics, with clear decision rights and escalation thresholds at each level, are how that traceability gets built.

The Board's Specific Obligations Under the OCC Guidelines

The OCC's Heightened Standards assign non-delegable responsibilities to the board with respect to the RAS. These aren't suggestions for good governance — they're regulatory requirements.

Formal Review and Approval

Under Appendix D Section II.G.1, the board or its risk committee must review and approve the RAS at least annually, and more frequently when material changes occur in:

- The bank's business model or strategy

- Its risk profile

- Market conditions

Annual approval is the minimum — examiners expect boards to act sooner when conditions shift.

Active Oversight — Not Just Approval

The OCC's expectation of "active oversight" under Section III means board members must be able to challenge management decisions that would cause the bank's risk profile to exceed its stated appetite. That requires directors to genuinely understand the RAS — not just receive it at year-end.

A board that can confirm it approved the RAS but can't articulate how it informs their judgment on a specific management recommendation hasn't met the standard.

Independent Directors, Training, and Self-Assessment

Section III of the Heightened Standards also requires:

- At least two independent directors (Section III.D)

- A formal, ongoing director training program covering complex products and services, applicable laws and regulations, and the bank's current risk profile (Section III.E)

- An annual board self-assessment of effectiveness in meeting the Section III standards (Section III.F)

These requirements exist precisely because meaningful RAS oversight requires informed directors. Examiners look for evidence that training is substantive and current — not a once-a-year checkbox.

Technology and cyber risk is where many boards find the Section III training requirement hardest to satisfy — the language is technical, the threat landscape shifts quickly, and few directors have direct operating experience. Tyson Martin works with boards on exactly this gap: drafting risk appetite language for technology risk, building escalation ladders, and running tabletop exercises that test both the framework and director decision-making under real pressure.

Monitoring, Quarterly Reporting, and Breach Protocols

Required Monitoring Cadence

Appendix D Section II.G establishes a specific reporting rhythm:

- Independent risk management monitors the bank's risk profile against the RAS and reports to the board or risk committee at least quarterly

- Front line units monitor compliance with their risk limits and report to independent risk management at least quarterly

- More frequent monitoring is expected when risk size and volatility warrant it

Quarterly is the floor — not the target. Volatile risk environments demand a tighter cadence, and examiners will look for evidence that monitoring frequency tracked actual conditions.

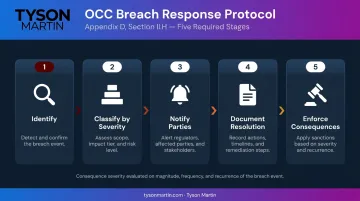

Breach Protocols Under Section II.H

When a limit in the RAS is breached, covered banks must have documented processes that:

- Identify breaches of the RAS, concentration limits, and front line unit limits

- Classify breaches by severity

- Notify appropriate parties — the board, front line management, independent risk management, internal audit, and the OCC — based on the magnitude of the breach

- Document how the breach will be, or has been, resolved in writing

- Establish accountability with consequences that consider magnitude, frequency, and recurrence

Compensation and performance structures must reflect risk limit adherence — not just financial outcomes. A pattern of repeated, low-severity breaches with no consequences is itself a governance failure under the OCC's framework.

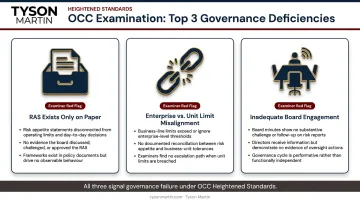

Common Weaknesses That Draw Examiner Scrutiny

Three governance failures surface repeatedly in OCC examinations of covered banks.

The RAS That Exists Only on Paper

The most common deficiency: a risk appetite statement that isn't embedded in operational decisions. Examiners look for evidence the RAS is actually used — not just filed. They check for its influence in:

- New product approvals

- Capital planning discussions

- Compensation program design

If the RAS sits in a document repository but doesn't visibly shape management behavior, that's a governance red flag.

Vague appetite language makes this problem worse. Words like "low," "moderate," or "conservative" without attached thresholds create a statement that sounds compliant but provides no real decision guidance. Thresholds need to be measurable — hours, dollars, coverage percentages — so the question "are we in appetite or out of appetite?" has a clear answer.

Misalignment Between Enterprise and Unit-Level Limits

Appendix D Section II.F requires unit-level limits to roll up to the enterprise RAS. When front line unit limits, in aggregate, would exceed the board-approved appetite — or when limits haven't been updated after a strategic change — examiners will flag the disconnect.

The problem tends to emerge gradually. The enterprise RAS gets updated annually, but unit-level limits lag behind. Or a new business line launches without aligning its limits against the aggregate ceiling. Either way, the gap is visible to an examiner even when it isn't visible internally.

Inadequate Board Engagement

The OCC's expectation of active oversight doesn't mean receiving and signing off on the RAS once a year. Directors must be prepared to explain how the RAS informs their judgment on specific management decisions — not just confirm they received the document.

Boards that can't demonstrate they've challenged a management recommendation on risk grounds — or that treat the RAS as an annual sign-off rather than a live governance tool — draw examiner criticism. A well-drafted document doesn't offset weak director engagement.

Frequently Asked Questions

What is the OCC's risk appetite framework?

The OCC's risk appetite framework, required under Appendix D to 12 CFR Part 30, is the structured system through which a covered bank defines, monitors, and governs its aggregate risk. It spans the written RAS, concentration and front line unit risk limits, quarterly monitoring, and formal breach protocols — all under board oversight.

What is an example of a risk appetite statement?

The OCC's own Enterprise Risk Appetite Statement released in April 2016 is a useful reference. The agency assigned categorical appetite levels across nine risk domains — including technology, operational, strategic, and reputational risk — demonstrating how a well-structured statement differentiates tolerance by domain rather than applying a single blanket posture across all risk types.

Who does the OCC risk appetite statement requirement apply to?

The requirement applies to "covered banks" — insured national banks, federal savings associations, and federal branches with $50B or more in average total consolidated assets. Banks below that threshold also qualify if their parent controls a covered bank, or if the OCC determines they present heightened complexity or risk.

What is the difference between risk appetite and risk tolerance under the OCC guidelines?

Risk appetite is the board-level declaration of how much and what types of risk the institution will assume. Risk tolerance refers to the specific quantitative limits that define acceptable deviation from that appetite. Appendix D requires both: qualitative appetite language and quantitative limits.

How often must the risk appetite statement be reviewed and approved?

The board or its risk committee must review and approve the RAS at least annually, and more frequently when material changes occur in the bank's strategy, business model, risk profile, or market conditions. Independent risk management must also review and update the broader risk governance framework at least annually.

What happens when a risk limit in the risk appetite statement is breached?

Covered banks must follow documented breach protocols: identify the violation, classify it by severity, notify appropriate parties (including potentially the OCC), document a resolution plan, and enforce consequences. Under Appendix D Section II.H, consequences must reflect the magnitude, frequency, and recurrence of violations — not be treated as routine administrative events.