Introduction: Why AI Risk Is Now a Board-Level Responsibility

Credit unions are deploying AI across loan decisioning, fraud detection, member-facing chatbots, and back-office automation — and adoption is accelerating. A 2025 Filene Research Institute survey covering 110 participants across 78 organizations found credit union leaders are actively navigating AI strategy and integration, often without formal governance structures.

That gap creates a genuine dilemma. Credit unions that sidestep AI risk governance fall behind competitors and invite regulatory scrutiny. Those that deploy AI without structured oversight expose members to real harm: biased lending decisions, fraudulent account takeovers, privacy violations, and silent operational failures.

NCUA has made clear that boards and management share accountability for AI oversight. This guide covers what that accountability requires:

- The risk categories that demand board attention

- How to build a practical AI risk assessment process

- What NCUA expects from oversight and documentation

- How to structure governance so ownership is unambiguous

Key Takeaways

- AI risk assessment is an ongoing discipline, not a one-time review — it applies to every AI tool, including vendor-supplied systems

- Five risk categories demand board attention: cybersecurity exposure, algorithmic bias, deepfake fraud, data privacy, and model drift

- NCUA applies existing technology-neutral regulations to AI — no AI-specific rule is required to create regulatory exposure

- Effective governance means board accountability plus management ownership across functions — with escalation thresholds defined before an incident occurs

- Vendor-delivered AI carries the same risk as in-house AI — NCUA's third-party oversight expectations apply without exception

What AI Risk Assessment Means for Credit Unions

AI risk assessment is the structured process of identifying, evaluating, and prioritizing potential harms — operational, compliance, reputational, and financial — that can arise from using AI tools, whether built in-house or sourced from a vendor.

For credit unions, this is not a one-time checkbox. It is an ongoing discipline embedded into enterprise risk management, vendor oversight, and internal audit cycles. A model validated at deployment can fail silently six months later. A vendor can update its underlying AI without notifying clients. Governance must keep pace with how those risks evolve.

What the Scope Actually Covers

Most credit union leaders think of AI risk as a technology problem. It's broader than that. A complete AI risk assessment covers:

- Data inputs: where training and transaction data comes from, how it's stored, and who can access it

- Model outputs: the loan approvals, fraud flags, and member service decisions those models produce

- Human behavior: whether staff override, accept, or ignore AI recommendations — and under what conditions

- Member impact: who bears the consequence when a decision is wrong or reflects a bias

Vendor-supplied AI is not exempt. If a fraud detection platform or loan origination system uses AI, the credit union owns the risk that platform creates. NCUA's supervisory expectations make that ownership explicit.

The Key AI Risk Categories Credit Unions Must Address

Cybersecurity and Data Exposure

AI systems concentrate sensitive member data and operate with broad access to core systems — making them high-value targets. Standard perimeter defenses don't fully address AI-specific attack surfaces.

NIST identifies four major adversarial AI attack types: evasion, poisoning, privacy, and abuse attacks — each capable of manipulating AI behavior without triggering traditional security controls. Specific vectors relevant to credit unions include:

- Poisoned training data that corrupts model outputs over time

- API exploitation targeting AI model endpoints

- Prompt injection attacks on member-facing chatbots

- Embedded malicious code in third-party large language models

- Unauthorized model access exposing member records

Algorithmic Bias and Fair Lending

AI models trained on historical data can encode discriminatory patterns, producing disparate outcomes in loan decisioning, credit scoring, and member services. Under ECOA and Regulation B, that creates direct regulatory exposure — regardless of whether a model is proprietary or vendor-supplied.

The CFPB has been explicit: creditors must provide specific, accurate reasons for adverse action even when decisions are made by complex algorithms. "The model decided" is not a compliant adverse-action notice. The opacity of many commercial AI models compounds this risk — credit unions may not be able to explain what a vendor's model actually considered.

Deepfake Fraud and AI-Enabled Social Engineering

Bad actors are using AI to clone member voices, fabricate identity documents, create synthetic identities, and defeat biometric verification. In November 2024, FinCEN issued a formal alert on fraud schemes involving deepfake media specifically targeting financial institutions.

This isn't a theoretical concern. FinCEN's guidance describes specific fraud typologies credit unions should build detection and response protocols around — including synthetic media used to bypass identity verification during account opening and wire transfer requests.

Data Privacy and PII Leakage

When staff use commercially available generative AI tools — including consumer-grade LLMs — and input member information, that data often routes to external servers outside the credit union's control. The U.S. Treasury has identified unauthorized data collection and secondary use of proprietary data through third-party AI providers as a material privacy risk for financial institutions.

This is one of the most immediate operational risks for credit unions evaluating productivity AI tools. Without a written acceptable-use policy and clear guidance on what may and may not be entered into AI systems, PII exposure can occur without any audit trail or control mechanism.

Model Drift and Operational Reliability

AI models degrade over time as real-world conditions diverge from their training data. A fraud detection model built on pre-pandemic transaction patterns performs differently in today's environment. When a credit scoring model trained before a rate cycle misweights risk, it often does so without any signal.

That degradation is the real danger — it's usually invisible. A credit union may not know a model has become unreliable until fraud losses spike, loan performance deteriorates, or an examiner asks questions the team can't answer. Treasury's guidance on AI in financial services emphasizes periodic reevaluation precisely because AI models can produce incorrect outputs confidently, with no warning indicator.

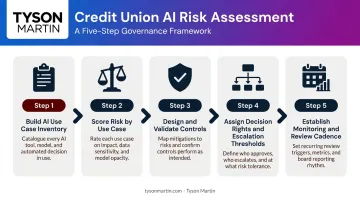

How to Build an AI Risk Assessment Process

Step 1 — Build a Complete AI Use Case Inventory

Start by cataloging every AI application in use or under evaluation. This includes AI embedded in existing vendor platforms — core banking systems, fraud tools, loan origination software, digital banking interfaces. For each application, document:

- What data the application accesses

- What decisions or outputs it produces

- Who owns oversight responsibility

Without this inventory, no governance structure is effective. You can't assess what you haven't named.

Step 2 — Score Risk by Use Case

Prioritize using a simple likelihood-times-impact approach across four dimensions: cybersecurity exposure, compliance risk, reputational risk, and operational reliability. Flag any use case that makes consequential decisions about members — lending, account access, fraud determinations — as requiring heightened scrutiny.

This doesn't need to be a complex scoring matrix. The goal is forcing a conversation about which AI applications carry the most exposure and ensuring those receive documented controls before anything else.

Step 3 — Design and Validate Controls

Once risks are scored, map specific controls to each high-priority application:

- Model validation before deployment (and after significant updates)

- Access controls on AI systems and training data

- Human review thresholds for automated decisions affecting members

- Data governance policies preventing PII from entering unsanctioned AI environments

- Logging and audit trail requirements for AI-influenced decisions

Step 4 — Assign Decision Rights and Escalation Thresholds

This is where most AI governance frameworks break down. The risk assessment is complete on paper, but nobody owns a real decision when something goes wrong.

Governance requires clarity on three questions: who has authority to approve a new AI deployment, who can halt a system showing anomalous behavior, and what triggers escalation from management to the board. Pre-deciding these thresholds — not drafting them during an incident — is what separates functional governance from a policy document.

Credit unions without a dedicated CISO or technology risk leader often find this step exposes a genuine governance gap. An advisor with board-level governance experience can help define decision rights, establish escalation thresholds, and build reporting that directors can actually inspect.

Step 5 — Establish a Monitoring and Review Cadence

AI risk assessments must be revisited at defined intervals and immediately when:

- A vendor updates its underlying AI model

- A new AI use case is being evaluated

- A cybersecurity incident or new fraud pattern emerges

- Regulatory guidance changes

Monitoring dashboards should track measurable outcomes — fraud detection accuracy, model decision rates, bias indicators — not just whether a review meeting occurred.

AI Governance: What Boards and Leadership Need to Own

Board-Level Accountability Starts With the Right Questions

Boards don't need to understand the technical architecture of AI systems. They do need to ask — and receive credible answers to — four questions:

- What AI tools does this credit union currently use?

- What risks do those tools introduce?

- What controls are in place, and how do we know they're working?

- What would trigger escalation to this board?

Vague answers, jargon-heavy responses, or "our vendor handles that" deflections are themselves a governance signal. Credible oversight requires credible reporting.

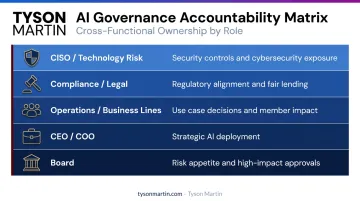

Cross-Functional Ownership

AI governance should not sit solely in IT. An effective structure includes:

| Function | Accountability |

|---|---|

| CISO / Technology Risk | Security controls, cybersecurity exposure |

| Compliance / Legal | Regulatory alignment, fair lending, adverse action |

| Operations / Business Lines | Use case decisions, member impact |

| CEO / COO | Strategic AI deployment decisions |

| Board | Risk appetite, high-impact AI approvals, trend reporting |

A cross-functional AI governance committee with a written charter puts this structure on paper. For boards that need to move quickly, an interim CISO with financial services governance experience can close the gap — standing up the committee structure, drafting the charter, and delivering board-ready risk reporting within the first engagement cycle.

Policy and Reporting Requirements

Every credit union deploying AI needs a written AI use policy. At minimum, it should address:

- Acceptable use — which AI tools are approved and for what purposes

- Prohibited inputs — what staff may not enter into commercial AI tools

- Data handling rules — how member data is classified and protected

- Consequences for non-compliance — enforcement with teeth, not just policy on paper

Board reporting on AI risk should show trend over time, not point-in-time status. A useful AI risk report covers what changed since last review, which risks increased or decreased, and what decisions the board is being asked to make — not a dense technical summary that obscures the actual risk picture.

Navigating NCUA Expectations and Regulatory Alignment

NCUA's Current Supervisory Posture

As of 2026, NCUA has not issued AI-specific rules or regulations. Existing technology-neutral supervisory standards apply — covering information security, internal controls, third-party due diligence, and ongoing risk monitoring. Credit unions are not off the hook because no AI-specific rule exists.

NCUA evaluates AI use through the lens of safety and soundness. Boards and management are expected to oversee AI use and mitigate operational, compliance, and security risks — and examiners are already asking about it.

Alignment With Established Frameworks

Because NCUA's standards are technology-neutral, they don't tell you how to manage AI risk — only that you must. Two established frameworks fill that gap:

- NIST AI Risk Management Framework (AI RMF 1.0) — structures risk management around govern, map, measure, and manage functions; applies across the full AI lifecycle

- COSO framework for AI and enterprise risk management — supports board-level risk appetite and governance alignment

Structuring your AI governance program around either framework creates a documented, examiner-recognizable audit trail — which is the practical standard NCUA applies when there's no specific rule to cite.

Heightened Expectations for High-Impact AI

AI applications that make or materially influence consequential decisions (access to credit, account services, fraud determinations) carry heightened supervisory scrutiny. For these applications, examiners will expect evidence of:

- Documented risk assessments completed before deployment

- Model validation evidence

- Human oversight mechanisms for automated decisions

- Adverse-action notice processes that reflect actual model reasoning

Vendor AI Due Diligence: A Practical Approach

Why Vendor AI Is the Biggest Risk Exposure

Most credit union AI risk sits inside third-party platforms. Core banking systems, fraud detection vendors, loan origination tools, and digital banking chatbots often include AI the credit union didn't build and may not fully understand.

NCUA Letters 07-CU-13 and 01-CU-20 apply fully to these relationships. NCUA has stated that failure to monitor and report on third-party program performance is unsafe and unsound.

Credit unions remain accountable for what their vendors do with member data — and for how vendor AI models perform in practice.

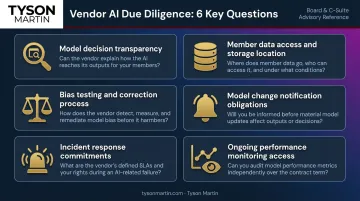

Key Questions for Vendor AI Evaluation

Before signing a contract — and during ongoing oversight — require answers to:

- How does the model make decisions, in plain terms?

- What member data does it access, and where is that data stored?

- How does the vendor test for bias, and how are corrections made?

- What transparency will the vendor provide when the underlying model changes?

- What are the vendor's incident response obligations if the AI system fails or is compromised?

- Can the vendor demonstrate ongoing model performance monitoring with results you can actually inspect?

Contractual and Ongoing Monitoring Requirements

Vendor contracts for AI tools should specify:

- Audit rights — including what evidence the vendor must produce and on what timeline

- Model validation — who is responsible for it and how often it occurs

- Data handling standards covering storage, access, and deletion

- Change notification — required advance notice before the vendor updates the AI system

- Incident response timelines matching your own regulatory obligations

- Right to terminate for cause if the vendor cannot meet transparency requirements

Contracting sets the floor — ongoing monitoring holds vendors to it. Periodically verify that performance claims from the sales cycle still hold once the system is live and processing real member data.

When a vendor cannot or will not provide required transparency, document that refusal as a risk finding, escalate it through your governance structure, and treat it as grounds for contract review.

Frequently Asked Questions

Does NCUA have specific AI regulations credit unions must follow?

No. As of 2026, NCUA has not issued AI-specific rules. However, existing technology-neutral regulations covering information security, third-party vendor management, and safety and soundness apply fully to AI use. Demonstrating responsible risk management is required regardless of the technology involved.

What is an AI risk assessment for a credit union?

An AI risk assessment is the structured process of identifying and evaluating potential harms — cybersecurity exposure, bias in automated decisions, data privacy failures, and operational reliability — for each AI application a credit union uses or is considering. The goal is determining what controls are needed before and during deployment.

What are the biggest AI risks for credit unions specifically?

Five categories demand the most attention:

- Algorithmic bias affecting fair lending compliance

- Deepfake-enabled fraud targeting member identity verification

- Data privacy exposure from generative AI tools used by staff

- Cybersecurity vulnerabilities specific to AI systems

- Silent model drift that degrades performance without obvious warning signs

Who is responsible for AI risk oversight — the board or management?

Both, with distinct roles. Management owns day-to-day risk identification, controls implementation, and monitoring. The board is accountable for approving AI risk appetite, receiving credible trend-based reporting, and making decisions on high-impact AI use cases. Governance fails when either side abandons their portion of that responsibility.

How often should a credit union update its AI risk assessment?

At minimum annually — and sooner if triggered by:

- A vendor updating its AI model

- A new AI use case under evaluation

- A cybersecurity incident or fraud pattern signaling a shifted threat landscape

- New or revised regulatory guidance

What should credit unions look for when evaluating an AI vendor?

Focus on six areas:

- How the model makes decisions, explained in plain terms

- What member data it accesses and where it's stored

- How the vendor tests and corrects for bias

- What audit rights and change notification obligations appear in the contract

- What incident response commitments the vendor makes

- Whether ongoing model performance monitoring produces results the credit union can inspect