Boards make consequential decisions about capital allocation, risk tolerance, and management accountability. When the report they receive is backward-looking, structurally inconsistent, or buried under 80 pages of supporting detail, those decisions suffer — not because directors lack judgment, but because the information pipeline failed them.

McKinsey research covering 857 board directors found that only 58% said their board's decisions had high or very high impact on long-term value creation — down from 62% in 2019. That gap does not close by adding more data. It closes by improving how information reaches the board in the first place.

This guide covers what board-ready reporting actually means, why it is a governance responsibility and not a formatting exercise, and the specific practices that separate reports that enable decisions from ones that merely inform.

Key Takeaways

- Board-ready reporting is a governance discipline — not a data delivery function

- The core structure includes an executive summary, strategic KPIs, forward-looking forecasts, a risk escalation summary, and clean supporting schedules

- Boards govern the future — reports anchored entirely in historical performance leave directors unable to act

- Consistent format, stable KPI definitions, and pre-established escalation thresholds build board confidence

- The close process is the foundation — if it is chaotic, nothing downstream will be credible

What Is Board-Ready Reporting?

Board-ready reporting is the practice of preparing concise, decision-ready financial and risk information that gives the board what it needs to govern — not just to review.

That distinction matters. A report can be accurate, comprehensive, and professionally formatted while still failing to serve the board's actual function.

Governance requires directors to oversee risk, challenge assumptions, allocate capital, and hold management accountable. A report that doesn't support those actions hasn't done its job — no matter how clean the numbers look.

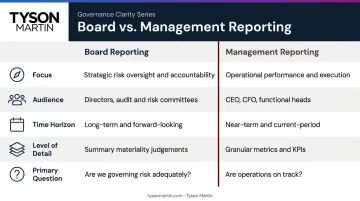

Board Reporting vs. Management Reporting

These are different documents serving different audiences:

| Dimension | Board Reporting | Management Reporting |

|---|---|---|

| Focus | Strategic health, risk posture, forward outlook | Operational detail, departmental performance |

| Audience | Directors exercising oversight | Executives running day-to-day operations |

| Time horizon | Forward-looking with historical context | Current period and recent trends |

| Level of detail | High-level with accessible supporting schedules | Granular, function-specific |

| Primary question | Are we on track strategically? What requires board action? | What happened this week and what needs fixing? |

Board-ready means disciplined. The report must be accurate, auditable, and structured around the board's oversight role — not around the CFO's internal workflow or what was easiest to pull from the close package.

Why Board Reporting Is a Governance Responsibility

The board's fiduciary duty depends entirely on the quality of information it receives. When reporting is unclear, backward-looking, or structured around management convenience, boards cannot fulfill their oversight role. That is not a communications problem — it is a governance failure.

Decision Rights Come First

Board-ready reporting must make explicit which decisions belong to the board and which belong to management. Without that clarity, reporting creates friction rather than resolving it. Research published through the Harvard Law School Forum on Corporate Governance found that board-management role clarity deteriorates during crises, producing excessive deference to the CEO and ineffective oversight — precisely when clear decision rights matter most.

A practical framework for mapping decision authority covers five areas:

- Risk acceptance — what thresholds require board versus executive awareness

- Policy exceptions — who grants them, for how long, and what evidence is required

- Incident escalation — who declares severity, who notifies external parties, who speaks publicly

- Budget tradeoffs — what can be reallocated without formal approval

- Vendor and partnership decisions — who owns the relationship and signs off

Escalation Thresholds Prevent Both Noise and Surprises

Effective board reports embed escalation logic. Without pre-established thresholds, CFOs either over-escalate — flooding boards with operational detail — or under-escalate, which produces the surprises that damage trust most severely.

Escalation thresholds should be expressed in business terms: dollar impact, hours of downtime, customer exposure, and regulatory consequence. Not technical severity scores that only specialists understand.

Deloitte's guidance on board process design recommends that boards work with management to define thresholds for real-time board involvement and to clearly distinguish items requiring a decision from items provided for review. That structure should live inside the report itself, not in a separate governance document no one reads before the meeting.

Transition Environments Stress-Test Everything

Organizations navigating leadership change, M&A activity, regulatory scrutiny, or operational crisis face heightened reporting demands at the exact moment their processes are least stable. The CFO's reporting framework is often the first governance structure tested under pressure — and the first to reveal gaps.

Each transition type creates a distinct reporting risk:

- New leadership — incoming executives may challenge established thresholds before they understand them

- M&A activity — two governance frameworks collide; escalation paths are unclear on both sides

- Regulatory scrutiny — boards need documented evidence of decisions, not just outcomes

- Operational crisis — speed pressure compresses review cycles and bypasses normal approval chains

The CFO who has mapped these failure modes in advance is the one the board turns to when they occur.

The Essential Components of a Board-Ready Report

A well-constructed board report has five components. Each serves a distinct governance purpose.

1. Executive Summary

One page. Answers three questions before directors ask them:

- How are we performing versus plan?

- What changed since the last meeting?

- What requires board-level action now?

If a director can read only this page and leave adequately informed for the discussion, the executive summary has done its job.

2. Strategic KPIs

Metrics tied directly to board-approved strategic objectives — not departmental performance indicators repackaged for a governance audience. The criteria:

- Linked to a specific strategic objective the board approved

- Defined consistently, with no changes to methodology between periods

- Shown as trends over time, not just point-in-time snapshots

- Limited in number — five to eight is usually sufficient

Rotating what gets reported each quarter, or redefining how a metric is calculated without explanation, destroys the board's ability to track progress. The FRC's review of alternative performance measures found consistent room for improvement in how companies define, explain, and reconcile non-standard metrics — a signal that metric discipline remains a real gap.

3. Forward-Looking Section

Boards govern the future. A report with no forward-looking content leaves directors perpetually reacting rather than guiding. This section should include:

- Rolling forecasts with the assumptions that underpin them

- Scenario analysis covering at least a base and stress case

- Key inflection points — decisions, milestones, or external factors that could change the trajectory

If the assumptions change, that change needs to be disclosed explicitly, not buried in a footnote.

4. Risk and Escalation Summary

Plain language. Covers:

- What changed in the risk environment since the last briefing

- What is currently being monitored at the management level

- What has crossed or is approaching the threshold for board action

Cyber, operational, and financial risks each warrant distinct treatment. Directors do not need technical depth — they need business-impact framing: dollar exposure, operational consequence, and what decision is required of them.

5. Supporting Schedules and Audit Trail

Every headline number must trace back to clean, documented source data. These schedules do not belong in the main report, but they must be organized and immediately accessible when questions arise.

If a board member asks a follow-up question and the CFO cannot produce the underlying support within 24 hours, the report has a credibility problem — regardless of how polished the deck looked.

How to Structure Reports That Enable Decisions

Getting the structure right is what determines whether the report actually functions in the boardroom.

Narrative Before Data

Each section should open with the conclusion, then provide supporting evidence. Directors need the headline first. Not all of them will work through every supporting exhibit, but all of them need the key takeaway immediately.

A common CFO instinct is to build up to the conclusion — to layer context before delivering the finding. That structure works for internal management discussions. It fails in a board report, where time is compressed and directors may be scanning rather than reading linearly.

Consistent Structure, Every Cycle

Changing formats, KPI definitions, or report structures between quarters does more damage than most CFOs realize. It prevents trend analysis, forces directors to reorient every meeting, and signals instability rather than competence.

A stable reporting template, reviewed and approved by the board annually, is a governance asset. Some CFOs resist this because it feels constraining. In practice, it builds the kind of pattern recognition that allows boards to spot anomalies quickly and ask better questions.

Escalation Language Built Into the Report

Every item in the report should carry a clear designation:

- Board vote required

- Board awareness — no action needed

- Delegated to management

When this language is absent, directors spend meeting time trying to figure out what is being asked of them. That is wasted governance capacity.

Balance Builds More Trust Than Polish

Boards that receive only favorable narratives become skeptical. They start asking more questions, not fewer, because they sense gaps. Proactively including identified weaknesses, contrarian views, and worst-case scenarios does the opposite — it signals that management is not managing the optics, and directors can engage with the real picture.

Directors who trust the report read it differently. They stop testing for what's missing and start engaging with what's there.

When External Perspective Helps

CFOs establishing governance frameworks from scratch, or recovering from a period of weak oversight, often benefit from working with an advisor who has sat on both sides of the reporting relationship. Tyson Martin's board advisory work focuses on this directly: clarifying decision rights, building escalation ladders, and establishing a reporting cadence that holds up under scrutiny. The goal is a functional governance structure in place before an incident, a transition, or a board challenge makes the absence visible.

Common Board Reporting Mistakes CFOs Make

Reporting Volume Instead of Insight

Sending an 80-page board pack with every available data point is a defensive habit, not a governance one. Deloitte's board effectiveness research frames this as a signal problem: boards need cleaner signal with less noise, and the CFO's job is to filter, not to forward. More data doesn't demonstrate rigor. It demonstrates a failure to prioritize.

Backward-Only Framing

Reports anchored entirely in historical performance leave boards unable to anticipate or guide. If there is no forward-looking section, directors are always reacting. They can review what happened, but they cannot govern what comes next. Without a forward view, the board becomes a historian instead of a governing body.

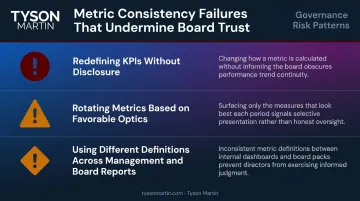

Inconsistent Metrics and Moving Definitions

Changing KPI definitions, restating prior periods without explanation, or rotating which metrics get reported destroys the board's ability to track trends. Consistent reporting discipline matters beyond the boardroom, too.

The PCAOB's auditing standards note that unreasonable accounting estimates, inappropriate principles, or inadequate risk disclosures can trigger departures from a clean audit opinion — an audit risk that originates from the same discipline failures that erode board reporting quality.

The three patterns that most reliably undermine metric consistency:

- Redefining KPIs without disclosing the change or restating prior periods

- Rotating which metrics appear based on what looks favorable that quarter

- Using different definitions across management reports and board packs

Best Practices for Sustainable, Credible Board Reporting

Document the reporting policy in writing — covering frequency, depth, format, and escalation thresholds, reviewed annually with the board. A written policy prevents drift, sets shared expectations, and gives new directors a clear orientation to how governance information flows.

Solicit structured feedback — reporting quality improves through direct input from directors, not assumptions about what they want. PwC's board effectiveness guidance recommends that boards provide direct feedback to management on the quality and timeliness of pre-read materials, with clear follow-up timelines.

Build a short feedback loop into each cycle. Probe for gaps, accuracy concerns, and accessibility issues, then demonstrate responsiveness before the next reporting period.

Treat the close process as the foundation. A tight, documented monthly or quarterly close is the prerequisite for accurate, timely board reporting. Credible reporting cannot be produced on top of a chaotic close process.

As KPMG's internal control guidance states, strong internal control over financial reporting is the bedrock of public and investor confidence. Management cannot satisfy financial reporting responsibilities without it. A disciplined close process is what gives the board something it can actually rely on.

Frequently Asked Questions

What should be included in a board report?

A board report should cover five core components: an executive summary, strategic KPIs tied to board-approved objectives, forward-looking forecasts with stated assumptions, a risk and escalation summary, and supporting schedules that can be accessed when questions arise. Each component serves the board's oversight role, not the CFO's internal workflow.

What are the five qualities of a good report?

Accuracy, relevance, timeliness, clarity, and forward-looking insight. Together, these qualities ensure the board acts on current, trustworthy information — enabling governance rather than pure retrospective review.

What are the three different types of reporting?

Board-level reporting focuses on strategic health, risk posture, and forward-looking decisions. Management reporting provides the operational and departmental detail executives need to run the business. Regulatory or compliance reporting satisfies statutory and disclosure obligations.

What are the four types of audit report?

The four types are unqualified (clean), qualified, adverse, and disclaimer of opinion — defined under PCAOB AS 3101 and IAASB ISA 705. A clean opinion requires fair presentation and sufficient audit evidence; disciplined board reporting and strong internal controls directly support that standard.

How often should board-ready reports be prepared?

Most organizations prepare formal board reports quarterly, aligned with board meetings. In fast-moving or transitional environments — new leadership, M&A activity, or operational disruption — monthly financial snapshots may be appropriate between formal cycles. The cadence should be documented in a written reporting policy and reviewed annually.

What is the difference between board reporting and management reporting?

Board reporting focuses on strategic health, risk posture, and the forward-looking information directors need to govern. Management reporting provides operational depth — departmental performance, execution tracking, and the granular detail executives need to run day-to-day operations. A common mistake is submitting management reports to the board without restructuring them for a governance audience.